You might also like

- Institutes of Biblical Law R. J. RushdoonyDocument1,064 pagesInstitutes of Biblical Law R. J. RushdoonyChalcedon Foundation98% (46)

- CORPORATE INCOME TAX (Answer Key)Document5 pagesCORPORATE INCOME TAX (Answer Key)Rujean Salar AltejarNo ratings yet

- Rothbard On RevisionismDocument126 pagesRothbard On RevisionismLiberty AustraliaNo ratings yet

- DONATIONDocument13 pagesDONATIONJusty LouNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Tutorial 9 - PIT1-Summer 2023-Sample AnswerDocument4 pagesTutorial 9 - PIT1-Summer 2023-Sample Answerkien tran100% (1)

- TAX 1201 Answers Deductions From Gross IncomeDocument6 pagesTAX 1201 Answers Deductions From Gross IncomeCarlo Agravante100% (1)

- My German Tax Return: A step-by-step guide to file your taxes in GermanyFrom EverandMy German Tax Return: A step-by-step guide to file your taxes in GermanyAkademische ArbeitsgemeinschaftNo ratings yet

- SCS FamiliarisationDocument26 pagesSCS FamiliarisationKAH MENG KAMNo ratings yet

- Income Taxes Problem SolvingDocument3 pagesIncome Taxes Problem SolvingLara FloresNo ratings yet

- Tax: TRAIN Illustrative Problems: Long Problem With FormsDocument23 pagesTax: TRAIN Illustrative Problems: Long Problem With FormsNooroddenNo ratings yet

- Accounting For Income Tax QuizDocument5 pagesAccounting For Income Tax QuizTorico BryanNo ratings yet

- TX - Mock Test - Đáp ÁnDocument12 pagesTX - Mock Test - Đáp ÁnPhán Tiêu Tiền100% (1)

- Discontinued OperationsDocument2 pagesDiscontinued OperationsBwwwiiiiiNo ratings yet

- Academic Misconduct PolicyDocument29 pagesAcademic Misconduct PolicySahil BatraNo ratings yet

- S20 TX ROM Sample AnswersDocument8 pagesS20 TX ROM Sample AnswersKAH MENG KAMNo ratings yet

- TX-CYP Dec 21 AnswersDocument8 pagesTX-CYP Dec 21 AnswersKAM JIA LINGNo ratings yet

- Miscellaneous TopicsDocument93 pagesMiscellaneous Topicsgean eszekeilNo ratings yet

- CBE June 2021 - ADocument7 pagesCBE June 2021 - ANguyễn Hồng NgọcNo ratings yet

- Accounting For Taxes 6Document7 pagesAccounting For Taxes 6charlene kate bunaoNo ratings yet

- 20th Regional Mid Year Convention Cup 6 Easy RoundDocument18 pages20th Regional Mid Year Convention Cup 6 Easy RoundSophia De GuzmanNo ratings yet

- Accounting For Income TaxationDocument8 pagesAccounting For Income Taxationangelian bagadiongNo ratings yet

- Problems Accouting For Deferred Taxes Webinar ReoDocument7 pagesProblems Accouting For Deferred Taxes Webinar ReocrookshanksNo ratings yet

- ACC 3013 - FWA - Revision - 202110Document14 pagesACC 3013 - FWA - Revision - 202110falnuaimi001No ratings yet

- Taxable Income: 20% 10000 200000/2 200000000 PIT 200000000 5% 10mDocument32 pagesTaxable Income: 20% 10000 200000/2 200000000 PIT 200000000 5% 10mnga vuNo ratings yet

- Tax System L3A 2021 SMDocument2 pagesTax System L3A 2021 SMAmrani LisaNo ratings yet

- Section TWO 2024Document5 pagesSection TWO 2024basuonyshowNo ratings yet

- Atxuk Sample Marjun 2019 ADocument10 pagesAtxuk Sample Marjun 2019 AAdam KhanNo ratings yet

- S20 TX POL Sample AnswersDocument6 pagesS20 TX POL Sample AnswersKAH MENG KAMNo ratings yet

- F6 AnsDocument9 pagesF6 AnsRaza AliNo ratings yet

- IFRS Week 6Document4 pagesIFRS Week 6AleksandraNo ratings yet

- Income Tax - Corporations Sample Problems: SolutionsDocument12 pagesIncome Tax - Corporations Sample Problems: SolutionsYellow BelleNo ratings yet

- F6 - IPRO - 2021 - Mock 1 - AnswersDocument16 pagesF6 - IPRO - 2021 - Mock 1 - AnswersHussein SeetalNo ratings yet

- Identify The Letter of The Choice That Best Completes The Statement or Answers The QuestionDocument171 pagesIdentify The Letter of The Choice That Best Completes The Statement or Answers The QuestionRengeline LucasNo ratings yet

- F6 Mock - Exm - Answers - Dec2012Document17 pagesF6 Mock - Exm - Answers - Dec2012Inga ȚîgaiNo ratings yet

- VOL 2 16. Accounting For Income TaxationDocument15 pagesVOL 2 16. Accounting For Income TaxationdmangiginNo ratings yet

- IAS12 - Examples - SolutionDocument9 pagesIAS12 - Examples - SolutionTrần Nguyễn Tuệ MinhNo ratings yet

- 06 Actvity 1 1Document4 pages06 Actvity 1 14mpspxd5msNo ratings yet

- Week 3 - Extension Questions (Solutions)Document4 pagesWeek 3 - Extension Questions (Solutions)ichika20010201No ratings yet

- Finalchapter-16 2Document22 pagesFinalchapter-16 2Jud Rossette ArcebesNo ratings yet

- Income TaxesDocument3 pagesIncome TaxesCENTENO, JOAN R.No ratings yet

- DEFERRED TAX - TUTORIAL SOLUTION - Part 2Document4 pagesDEFERRED TAX - TUTORIAL SOLUTION - Part 2SARASVATHYDEVI SUBRAMANIAMNo ratings yet

- Book 3Document1 pageBook 3Quincy Lawrence DimaanoNo ratings yet

- Topic 1: Accounting For Income TaxesDocument13 pagesTopic 1: Accounting For Income TaxesPillos Jr., ElimarNo ratings yet

- Submit in Schoology Using " " 1.: Shirwin - Sandoval@olivarezcollege - Edu.phDocument2 pagesSubmit in Schoology Using " " 1.: Shirwin - Sandoval@olivarezcollege - Edu.phCherry MirabuenoNo ratings yet

- Quiz Chapter+9 Income+Taxes+-+Document5 pagesQuiz Chapter+9 Income+Taxes+-+Rena Jocelle NalzaroNo ratings yet

- Class Activities (Millan, 2019) : Requirements: A. How Much Is The Income Tax Expense For 2003? SolutionDocument6 pagesClass Activities (Millan, 2019) : Requirements: A. How Much Is The Income Tax Expense For 2003? SolutionPrincess TaizeNo ratings yet

- Cae05-Chapter 10 Income Tax Problem DiscussionDocument37 pagesCae05-Chapter 10 Income Tax Problem Discussioncris tellaNo ratings yet

- Accounting For Income Tax Comprehensive Problem 1: Additional InformationDocument1 pageAccounting For Income Tax Comprehensive Problem 1: Additional InformationAngel Keith MercadoNo ratings yet

- DocxDocument5 pagesDocxJohn Vincent CruzNo ratings yet

- Identify The Choice That Best Completes The Statement or Answers The QuestionDocument9 pagesIdentify The Choice That Best Completes The Statement or Answers The QuestionJay-L TanNo ratings yet

- Double TaxationDocument10 pagesDouble TaxationMintuNo ratings yet

- Module-Accounting For Income TaxDocument13 pagesModule-Accounting For Income TaxJohn Mark FernandoNo ratings yet

- Classroom Exercise - Unit 1-1Document2 pagesClassroom Exercise - Unit 1-1Hannah Jane ToribioNo ratings yet

- Tutorial 9 PIT1 Summer 2023 Sample AnswerDocument6 pagesTutorial 9 PIT1 Summer 2023 Sample Answernewgen2173No ratings yet

- Deductions From Gross IncomeDocument10 pagesDeductions From Gross IncomewezaNo ratings yet

- Fundamentals of Finance: Ignacio Lezaun English Edition 2021Document20 pagesFundamentals of Finance: Ignacio Lezaun English Edition 2021Elias Macher CarpenaNo ratings yet

- Acc 3013 - Fwa Revision AnswersDocument15 pagesAcc 3013 - Fwa Revision Answersfalnuaimi001No ratings yet

- Acc501 GDB 1 Sol Fall 2022Document1 pageAcc501 GDB 1 Sol Fall 2022Sth. Bilal BashirNo ratings yet

- Exam - Taxation MSA 206Document4 pagesExam - Taxation MSA 206Juan FrivaldoNo ratings yet

- Fundamentals of Finance: Ignacio Lezaun English Edition 2021Document13 pagesFundamentals of Finance: Ignacio Lezaun English Edition 2021Elias Macher CarpenaNo ratings yet

- TaxationDocument8 pagesTaxationPeligrino MacNo ratings yet

- FUNDALES BTAX MidtermsDocument4 pagesFUNDALES BTAX MidtermsE. RobertNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- TXPOL 2019 Dec QDocument14 pagesTXPOL 2019 Dec QKAH MENG KAMNo ratings yet

- TXROM 2019 Dec QDocument17 pagesTXROM 2019 Dec QKAH MENG KAMNo ratings yet

- TXROM 2018 Dec QDocument16 pagesTXROM 2018 Dec QKAH MENG KAMNo ratings yet

- S20 TX POL Sample AnswersDocument6 pagesS20 TX POL Sample AnswersKAH MENG KAMNo ratings yet

- TXPOL 2019 Dec ADocument8 pagesTXPOL 2019 Dec AKAH MENG KAMNo ratings yet

- TXROM 2019 Jun QDocument17 pagesTXROM 2019 Jun QKAH MENG KAMNo ratings yet

- Txrus 2019 Dec QDocument15 pagesTxrus 2019 Dec QKAH MENG KAMNo ratings yet

- TX (SGP) Sept 20 Sample CBE QuestionsDocument28 pagesTX (SGP) Sept 20 Sample CBE QuestionsKAH MENG KAMNo ratings yet

- S20 TX RUS Sample AnswersDocument8 pagesS20 TX RUS Sample AnswersKAH MENG KAMNo ratings yet

- S20 TX SGP Sample AnswersDocument7 pagesS20 TX SGP Sample AnswersKAH MENG KAMNo ratings yet

- TXZAF 2018 Dec QDocument16 pagesTXZAF 2018 Dec QKAH MENG KAMNo ratings yet

- TXSGP 2018 SepDec ADocument8 pagesTXSGP 2018 SepDec AKAH MENG KAMNo ratings yet

- TXZWE 2018 Dec QDocument15 pagesTXZWE 2018 Dec QKAH MENG KAMNo ratings yet

- TXZAF 2019 Dec ADocument8 pagesTXZAF 2019 Dec AKAH MENG KAMNo ratings yet

- Taxation VNM - ACCA F6Document8 pagesTaxation VNM - ACCA F6Nguyễn Hải TrânNo ratings yet

- TXZAF 2019 Dec QDocument17 pagesTXZAF 2019 Dec QKAH MENG KAMNo ratings yet

- S20 TX ZWE Sample AnswersDocument9 pagesS20 TX ZWE Sample AnswersKAH MENG KAMNo ratings yet

- S20 TX ZAF Sample AnswersDocument8 pagesS20 TX ZAF Sample AnswersKAH MENG KAMNo ratings yet

- AA SD21 QsDocument23 pagesAA SD21 QsKAH MENG KAMNo ratings yet

- TXZWE 2018 Dec ADocument9 pagesTXZWE 2018 Dec AKAH MENG KAMNo ratings yet

- Strategic Exam Blueprints 2022 2023 Version3Document56 pagesStrategic Exam Blueprints 2022 2023 Version3KAH MENG KAMNo ratings yet

- SCS May 22 Game PlannerDocument31 pagesSCS May 22 Game PlannerKAH MENG KAMNo ratings yet

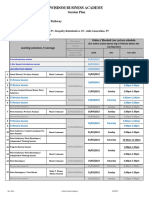

- SCS-Pathway Session Plans 2022Document2 pagesSCS-Pathway Session Plans 2022KAH MENG KAMNo ratings yet

- United States v. Marvin Jerome Horsley, 56 F.3d 50, 11th Cir. (1995)Document4 pagesUnited States v. Marvin Jerome Horsley, 56 F.3d 50, 11th Cir. (1995)Scribd Government DocsNo ratings yet

- March13.2012 - B House Body Urges TRB To Collect PNCC's P4 Billion Unpaid Concession FeesDocument1 pageMarch13.2012 - B House Body Urges TRB To Collect PNCC's P4 Billion Unpaid Concession Feespribhor2No ratings yet

- Full Download Operations and Supply Chain Management The Core 3rd Edition Jacobs Test BankDocument25 pagesFull Download Operations and Supply Chain Management The Core 3rd Edition Jacobs Test Bankbenjaminlaw0o100% (39)

- LAW Exam RevisionDocument3 pagesLAW Exam RevisionjasmineNo ratings yet

- Lyondel Basel NMPDocument3 pagesLyondel Basel NMPshikhajainNo ratings yet

- Irrigation Project ManualDocument66 pagesIrrigation Project ManualHorace Prophetic DavisNo ratings yet

- Omni Innovations LLC Et Al v. Impulse Marketing Group Inc Et Al - Document No. 14Document2 pagesOmni Innovations LLC Et Al v. Impulse Marketing Group Inc Et Al - Document No. 14Justia.comNo ratings yet

- KSEF Strucutred Electronic Invoice Dec2022 enDocument158 pagesKSEF Strucutred Electronic Invoice Dec2022 enfebeb26145No ratings yet

- Bahan Nafkah IdahDocument20 pagesBahan Nafkah IdahAli Alamsyah JosNo ratings yet

- Ayelala DeityDocument20 pagesAyelala DeityJose SegoviaNo ratings yet

- St. Vincent College of CabuyaoDocument6 pagesSt. Vincent College of CabuyaoDan RyanNo ratings yet

- Procurement - Oracle R12 AP-PO Changes OverviewDocument49 pagesProcurement - Oracle R12 AP-PO Changes OverviewKiran KumarNo ratings yet

- Circular 3Document4 pagesCircular 3MushtaqElahiShaikNo ratings yet

- Balbheemloan Sanction LetterDocument6 pagesBalbheemloan Sanction LetterVenkatesh DoodamNo ratings yet

- BHT p01 Cmyk 0914Document2 pagesBHT p01 Cmyk 0914Debbie BlankNo ratings yet

- Apollo Contacts ExportDocument30 pagesApollo Contacts Exportanasakram701No ratings yet

- Risk and Fraud Analytics For Telecom White PaperDocument11 pagesRisk and Fraud Analytics For Telecom White PaperhatipejaNo ratings yet

- Shils, Edward. Tradicion and Liberty. Article.Document13 pagesShils, Edward. Tradicion and Liberty. Article.David LuqueNo ratings yet

- Judgement Stay Can Be Granted For Six MonthsDocument36 pagesJudgement Stay Can Be Granted For Six MonthsAkram KhanNo ratings yet

- George Brann PDFDocument6 pagesGeorge Brann PDFmisanthropoNo ratings yet

- Status of Women in Indian Society: Harapriya MohapatraDocument4 pagesStatus of Women in Indian Society: Harapriya MohapatraDhanvanthNo ratings yet

- Bharat Petroleum Corporation Limited: Sv/Tv/Ta-FormDocument1 pageBharat Petroleum Corporation Limited: Sv/Tv/Ta-FormSan100% (1)

- Boyles Law Powerpoint Presentation MELCS 1 QUARTER 4 Prosperity and IndustryDocument15 pagesBoyles Law Powerpoint Presentation MELCS 1 QUARTER 4 Prosperity and IndustryJeo ShinNo ratings yet

- Spraytec RulingsDocument10 pagesSpraytec RulingsPuneet PagariaNo ratings yet

- Akt Lanjutan PDFDocument255 pagesAkt Lanjutan PDFIndra Ramadhan ChaniagoNo ratings yet

- This Study Resource Was: Study Guide For POLI 2057: Intro To International Politics Chapter 2: Realist TheoriesDocument4 pagesThis Study Resource Was: Study Guide For POLI 2057: Intro To International Politics Chapter 2: Realist TheoriesAadhityaNo ratings yet