You might also like

- NHA V AlmeidaDocument3 pagesNHA V AlmeidaShanicaNo ratings yet

- Williams V SunerDocument2 pagesWilliams V SunerShanicaNo ratings yet

- Carpio Morales V CADocument4 pagesCarpio Morales V CAShanicaNo ratings yet

- Marquez V COMELECDocument2 pagesMarquez V COMELECShanicaNo ratings yet

- de Leon V DuterteDocument6 pagesde Leon V DuterteShanicaNo ratings yet

- 023 Zabal V Duterte - Main Opinion + DissentDocument10 pages023 Zabal V Duterte - Main Opinion + DissentShanicaNo ratings yet

- Biraogo V Philippine Truth CommissionDocument3 pagesBiraogo V Philippine Truth CommissionShanicaNo ratings yet

- Blaquera V CSCDocument3 pagesBlaquera V CSCShanicaNo ratings yet

- Mesina v. SonzaDocument1 pageMesina v. SonzaShanicaNo ratings yet

- People V MacerenDocument3 pagesPeople V MacerenShanicaNo ratings yet

- Benny Hung v. BPI Finance PDFDocument2 pagesBenny Hung v. BPI Finance PDFShanicaNo ratings yet

- Philippines Pryce Assurance V CADocument2 pagesPhilippines Pryce Assurance V CAShanicaNo ratings yet

- Guillermo v. Uson PDFDocument3 pagesGuillermo v. Uson PDFShanicaNo ratings yet

- People V ArrojadoDocument4 pagesPeople V ArrojadoShanicaNo ratings yet

- Keppel Cebu Shipyard, Inc Vs Pioneer Insurance and Surety Corporation v2Document6 pagesKeppel Cebu Shipyard, Inc Vs Pioneer Insurance and Surety Corporation v2ShanicaNo ratings yet

- LRTA V Quezon CityDocument4 pagesLRTA V Quezon CityShanica100% (1)

- Pioneer V YapDocument3 pagesPioneer V YapShanicaNo ratings yet

- Nacar V Gallery FramesDocument4 pagesNacar V Gallery FramesShanicaNo ratings yet

- 10 BPI Family Bank V Franco, SollegueDocument5 pages10 BPI Family Bank V Franco, SollegueShanicaNo ratings yet

- Estrada V Office of The OmbudsmanDocument12 pagesEstrada V Office of The OmbudsmanShanicaNo ratings yet

- Air France V Court of AppealsDocument3 pagesAir France V Court of AppealsShanicaNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Bank StatementDocument3 pagesBank Statementbigman walthoNo ratings yet

- Your Adv Plus Banking: Account SummaryDocument4 pagesYour Adv Plus Banking: Account SummaryANo ratings yet

- By:-Rajat Singla Karan Singh Jaideep Singh Nikhil SinghDocument4 pagesBy:-Rajat Singla Karan Singh Jaideep Singh Nikhil Singhrajat_singlaNo ratings yet

- 24010700098136CNRB ChallanReceiptDocument1 page24010700098136CNRB ChallanReceiptBasavarajNo ratings yet

- Certification: Cupido Gerry D. AsuncionDocument26 pagesCertification: Cupido Gerry D. AsuncionMark Anthony De GuzmanNo ratings yet

- Taxation in South Africa 2010/11Document99 pagesTaxation in South Africa 2010/11vikramaditya_n84No ratings yet

- Saadiq SOCDocument31 pagesSaadiq SOCjoshmalikNo ratings yet

- NAB Statement X0256 10-Sep-2021Document6 pagesNAB Statement X0256 10-Sep-2021mkilfoyle11No ratings yet

- Section 80 C of Income Tax ActDocument3 pagesSection 80 C of Income Tax ActJatin BansalNo ratings yet

- Mark Up Versus MarginDocument18 pagesMark Up Versus MarginCaryl GalocgocNo ratings yet

- Invoice Apartmentsglenisla 14874Document1 pageInvoice Apartmentsglenisla 14874Ronnie HatiNo ratings yet

- ListDocument4 pagesListNgeleka kalalaNo ratings yet

- Online Challan For Admission BZU MultanDocument1 pageOnline Challan For Admission BZU MultanAbdul WahidNo ratings yet

- Itr 22-23 PDFDocument1 pageItr 22-23 PDFPixel computerNo ratings yet

- Assessment of Income From House PropertyDocument15 pagesAssessment of Income From House PropertyManish SinghNo ratings yet

- Oct 23Document2 pagesOct 23VIKAS TIWARINo ratings yet

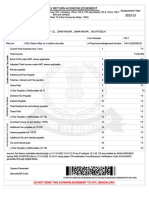

- PFMS Generated Print Payment Advice: To, The Branch HeadDocument2 pagesPFMS Generated Print Payment Advice: To, The Branch HeadPunjabi JindNo ratings yet

- Gmail - Guest Reservations - Reservation Confirmation #R4448147806Document4 pagesGmail - Guest Reservations - Reservation Confirmation #R4448147806amarenterpries01No ratings yet

- SERVICE DETAILS Padmini 06 118 007 470 (9965591961)Document3 pagesSERVICE DETAILS Padmini 06 118 007 470 (9965591961)mk gandhiNo ratings yet

- Wired Broadband Current Address Proof 12024 03 19 07 31 02 3798Document3 pagesWired Broadband Current Address Proof 12024 03 19 07 31 02 3798mohit19980628No ratings yet

- Lecture - 17: Computation of Income Under The Head Capital GainsDocument26 pagesLecture - 17: Computation of Income Under The Head Capital GainsHarjot SinghNo ratings yet

- BIR RegistrationDocument3 pagesBIR Registrationcara sophiaNo ratings yet

- Service Quotation For APC SRT3000RMXLI With Network Card-Prosperity Knitwear LTDDocument1 pageService Quotation For APC SRT3000RMXLI With Network Card-Prosperity Knitwear LTDYe Yan NaingNo ratings yet

- Fundamentals of Accountancy Business and Management 2Document20 pagesFundamentals of Accountancy Business and Management 2MOST SUBSCRIBER WITHOUT A VIDEO43% (7)

- Asu 2019-12Document49 pagesAsu 2019-12janineNo ratings yet

- Hostel Fee ReceiptDocument1 pageHostel Fee Receiptanoucha JordanNo ratings yet

- E0012 Payslip Template With CalculatorDocument2 pagesE0012 Payslip Template With CalculatorPTO Zamboanga del SurNo ratings yet

- Chapter-1: Principles of Income-Tax Law Self Assessment QuestionsDocument46 pagesChapter-1: Principles of Income-Tax Law Self Assessment QuestionsJasmeet SinghNo ratings yet

- Microsoft Word - Chapter 06 Negotiable InstrumentsDocument9 pagesMicrosoft Word - Chapter 06 Negotiable InstrumentsDuy Trần TấnNo ratings yet

- Report On E-Money and Its Usage (Business Communication)Document10 pagesReport On E-Money and Its Usage (Business Communication)Piyush PorwalNo ratings yet