You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Code of Ethics Test BankDocument20 pagesCode of Ethics Test BankJedidiah SmithNo ratings yet

- Simple Nonprofit Accounting TemplateDocument1,940 pagesSimple Nonprofit Accounting Templateluve silvia100% (1)

- GL PPT Basic For Oracle AppsDocument81 pagesGL PPT Basic For Oracle AppsPhanendra KumarNo ratings yet

- Job Order Costing: Illustrative ProblemsDocument30 pagesJob Order Costing: Illustrative ProblemsPatrick LanceNo ratings yet

- 3 - Answer Key Exercise Set #3 - Accounting For Partnership Part IDocument11 pages3 - Answer Key Exercise Set #3 - Accounting For Partnership Part INikko Bowie PascualNo ratings yet

- Module 2 - Financial Statements - Organized PDFDocument14 pagesModule 2 - Financial Statements - Organized PDFSandyNo ratings yet

- User Manual Asset AccountingDocument47 pagesUser Manual Asset AccountinginasapNo ratings yet

- Chapter 07Document5 pagesChapter 07Angel TumamaoNo ratings yet

- Arens Auditing and Assurance Services 13eDocument9 pagesArens Auditing and Assurance Services 13eintanfidztiraNo ratings yet

- Chapter 05Document12 pagesChapter 05Angel TumamaoNo ratings yet

- Auditing - RF-12 Quiz BowlDocument12 pagesAuditing - RF-12 Quiz BowlAngel TumamaoNo ratings yet

- Review of The Accounting ProcessDocument4 pagesReview of The Accounting ProcessAngel TumamaoNo ratings yet

- C. Sale of Professional Instruments and Implements Wearing Apparel, Domestic Animals and Personal Household Effects Under Certain ConditionsDocument150 pagesC. Sale of Professional Instruments and Implements Wearing Apparel, Domestic Animals and Personal Household Effects Under Certain ConditionsAngel TumamaoNo ratings yet

- Working Capital and Financing Decision SolutionDocument31 pagesWorking Capital and Financing Decision SolutionAngel TumamaoNo ratings yet

- AP QuizzerDocument9 pagesAP QuizzerAngel TumamaoNo ratings yet

- Capital ManagementDocument32 pagesCapital ManagementAngel TumamaoNo ratings yet

- Our Products Offering: Photocopy Shop Business Plan - SWOT AnalysisDocument20 pagesOur Products Offering: Photocopy Shop Business Plan - SWOT AnalysisAngel TumamaoNo ratings yet

- 4.02D Calculating A Reorder Point KEYDocument2 pages4.02D Calculating A Reorder Point KEYAngel TumamaoNo ratings yet

- Bus PoDocument5 pagesBus PoAngel TumamaoNo ratings yet

- Chapter I-The Nature of Auditing: Information CriteriaDocument10 pagesChapter I-The Nature of Auditing: Information CriteriaAngel TumamaoNo ratings yet

- Nbaa PloDocument212 pagesNbaa PlosmlingwaNo ratings yet

- Advanced Financial Accounting - Paper 8 CPA PDFDocument10 pagesAdvanced Financial Accounting - Paper 8 CPA PDFAhmed Suleyman100% (1)

- PETRONAS PIR2021 Financial Report 2021Document174 pagesPETRONAS PIR2021 Financial Report 2021Ez BzNo ratings yet

- Foundations of Entrepreneurship: Basic Accounting and Financial StatementsDocument89 pagesFoundations of Entrepreneurship: Basic Accounting and Financial StatementsTejaswi BandlamudiNo ratings yet

- SoM UIA Forensic Review 11.25.2020 708891 7Document34 pagesSoM UIA Forensic Review 11.25.2020 708891 7Tiffany RobertsonNo ratings yet

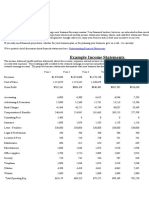

- Example Income Statements: Business Plan Financial ProjectionsDocument3 pagesExample Income Statements: Business Plan Financial ProjectionsSUMANTO SHARANNo ratings yet

- Job Opportunities World Bank IUCEA African Centers of Excellence (ACE II) ProjectDocument1 pageJob Opportunities World Bank IUCEA African Centers of Excellence (ACE II) ProjectRashid BumarwaNo ratings yet

- UAS ALK Dinda Azzahra Salsabilla Contoh Forecasting and Valuation AnalysisDocument9 pagesUAS ALK Dinda Azzahra Salsabilla Contoh Forecasting and Valuation AnalysisDinda AzzahraNo ratings yet

- International Accounting 3Rd Edition Doupnik Test Bank Full Chapter PDFDocument40 pagesInternational Accounting 3Rd Edition Doupnik Test Bank Full Chapter PDFJulieHaasyjzp100% (9)

- TEST BANK For Advanced Financial Accounting 13th Edition by Theodore Christensen Verified Chapter's 1 - 20 CompleteDocument70 pagesTEST BANK For Advanced Financial Accounting 13th Edition by Theodore Christensen Verified Chapter's 1 - 20 Completemarcuskenyatta275No ratings yet

- Accounting For Receivables: Summary of Questions by Study Objectives and Bloom'S TaxonomyDocument51 pagesAccounting For Receivables: Summary of Questions by Study Objectives and Bloom'S TaxonomyRabie HarounNo ratings yet

- CA Welcome Pack 2020 Reduced VersionDocument16 pagesCA Welcome Pack 2020 Reduced VersionHenry Sicelo NabelaNo ratings yet

- EA and ReportingDocument17 pagesEA and ReportingsengottuvelNo ratings yet

- Auditing Standards and Auditors Performance1Document7 pagesAuditing Standards and Auditors Performance1alfikooNo ratings yet

- Analisis Laporan Keuangan Untuk Menilai Kinerja Keuangan Perusahaan PT. Ultrajaya Milk Industry, TBKDocument6 pagesAnalisis Laporan Keuangan Untuk Menilai Kinerja Keuangan Perusahaan PT. Ultrajaya Milk Industry, TBKMeirza FazriyahNo ratings yet

- Full Download:: Suggested Answers To Discussion QuestionsDocument8 pagesFull Download:: Suggested Answers To Discussion QuestionsIrawatiNo ratings yet

- Civil SocietDocument4 pagesCivil SocietAbdi Mucee TubeNo ratings yet

- Chapter 6:part Two Cost-Volume-ProfitDocument44 pagesChapter 6:part Two Cost-Volume-ProfitFidelina CastroNo ratings yet

- Introduction To Accounting: Fundamentals of Accountancy, Business and Management 2Document4 pagesIntroduction To Accounting: Fundamentals of Accountancy, Business and Management 2Emariel CuarioNo ratings yet

- FNSACC501 Assessment 2Document6 pagesFNSACC501 Assessment 2Daranee TrakanchanNo ratings yet

- FCB Records Summarized 20-22Document8 pagesFCB Records Summarized 20-22Eric HopkinsNo ratings yet

- MT1 Ch20Document7 pagesMT1 Ch20api-3725162100% (1)

- CEO Turnover, Corporate Tax Avoidance and Big Bath AccountingDocument50 pagesCEO Turnover, Corporate Tax Avoidance and Big Bath AccountingSaadBourouisNo ratings yet

- The The The Which Procedures? And: (! Te. of The Following Is ToDocument1 pageThe The The Which Procedures? And: (! Te. of The Following Is ToLove Sunshine BancaleNo ratings yet