You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5807)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Start-Up Legal PackDocument24 pagesStart-Up Legal Packzoya100% (1)

- Amazon FbaDocument9 pagesAmazon Fbadata baseNo ratings yet

- Taxation - Final ExamDocument4 pagesTaxation - Final ExamKenneth Bryan Tegerero Tegio100% (1)

- Special Resolution FormatDocument4 pagesSpecial Resolution FormatSanjeev TiwariNo ratings yet

- Playconomics 4 - MacroeconomicsDocument302 pagesPlayconomics 4 - MacroeconomicsMinhNo ratings yet

- Provident Fund Full DetailsDocument5 pagesProvident Fund Full DetailsGaurav VijayNo ratings yet

- SWOT Analysis CandP HomesDocument5 pagesSWOT Analysis CandP HomesRowena CahintongNo ratings yet

- Barangay Agenda For Governance and Development Year 2018-2019Document7 pagesBarangay Agenda For Governance and Development Year 2018-2019Lgu Buenavista100% (3)

- IS3223 Zara Case Study: Zara: IT For Fast FashionDocument27 pagesIS3223 Zara Case Study: Zara: IT For Fast FashionAlex NguyenNo ratings yet

- Tutorial 2 SolutionDocument7 pagesTutorial 2 SolutionMinhNo ratings yet

- Tutorial 3 SolutionDocument5 pagesTutorial 3 SolutionMinhNo ratings yet

- Tutorial 1 SolutionDocument4 pagesTutorial 1 SolutionMinhNo ratings yet

- Financial Accounting: Tools For Business Decision Making: Reporting and Analyzing ReceivablesDocument60 pagesFinancial Accounting: Tools For Business Decision Making: Reporting and Analyzing ReceivablesmikeNo ratings yet

- BIR Form No. 1709 Dec 2020 EncsDocument3 pagesBIR Form No. 1709 Dec 2020 EncsLaurence ElazeguiNo ratings yet

- Cross e of DemandDocument19 pagesCross e of Demandapi-53255207No ratings yet

- DNV Annual Report 2021Document83 pagesDNV Annual Report 2021AlekoNo ratings yet

- Konsep Global Strategi Bisnis R2Document41 pagesKonsep Global Strategi Bisnis R2Ricky NovertoNo ratings yet

- Cost and Management AccountingDocument52 pagesCost and Management Accountings.lakshmi narasimhamNo ratings yet

- Namma Kalvi 12th Business Maths Slow Learners Study Material em 216934 PDFDocument92 pagesNamma Kalvi 12th Business Maths Slow Learners Study Material em 216934 PDFElijah ChandruNo ratings yet

- Game Theory and The Prisoner's Dilemma: An AnalysisDocument5 pagesGame Theory and The Prisoner's Dilemma: An AnalysisPUPT-JMA VP for AuditNo ratings yet

- 1.business Organisation and StakeholdersDocument27 pages1.business Organisation and StakeholdersAli Khan AhmadiNo ratings yet

- Five Year Plan Class PresentationDocument12 pagesFive Year Plan Class PresentationVaishali SinghNo ratings yet

- Components of Industrial EconomyDocument2 pagesComponents of Industrial EconomyEllis ElliseusNo ratings yet

- Linmarr Deed of Absolute Sale PDFDocument2 pagesLinmarr Deed of Absolute Sale PDFMae De GuzmanNo ratings yet

- Tom enDocument29 pagesTom enAbhiraj dNo ratings yet

- Slide 1: Home Affordable Modification ProgramDocument27 pagesSlide 1: Home Affordable Modification ProgramglenhfordNo ratings yet

- EU Understanding Social InnovationDocument8 pagesEU Understanding Social InnovationEva KrokidiNo ratings yet

- The Benefits of Corporate Social ResponsibilityDocument2 pagesThe Benefits of Corporate Social ResponsibilityDavid Stivens CastroNo ratings yet

- Clo Rex Case Study Teaching NoteDocument5 pagesClo Rex Case Study Teaching Noteismun nadhifahNo ratings yet

- FXMD Circular NRB Foreign Investment and Loan MGT Bylaw 2078Document35 pagesFXMD Circular NRB Foreign Investment and Loan MGT Bylaw 2078Anil JayswalNo ratings yet

- Trade UnionismDocument16 pagesTrade UnionismBhavika BaliNo ratings yet

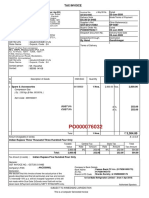

- Tax Invoice: Ice Make Refrigeration Limited - (From 1-Apr-2019)Document1 pageTax Invoice: Ice Make Refrigeration Limited - (From 1-Apr-2019)Sunil PatelNo ratings yet

- Value Added Tax 9.6.18Document3 pagesValue Added Tax 9.6.18Monica Carmona RicafrancaNo ratings yet

- Nbmba Lot Business Oportunity and Market ResearchDocument16 pagesNbmba Lot Business Oportunity and Market Researchapi-299852343No ratings yet