You might also like

- Activity Based Costing - APO 9Document13 pagesActivity Based Costing - APO 9manan guptaNo ratings yet

- Denison Mines PPT Vamshi-1Document10 pagesDenison Mines PPT Vamshi-1Thinkers ProNo ratings yet

- Lecture 2 Activity Based CostingDocument6 pagesLecture 2 Activity Based Costingmaharajabby81No ratings yet

- Cost and Management Accounting - II Activity Based Costing: CU SyllabusDocument5 pagesCost and Management Accounting - II Activity Based Costing: CU SyllabusTaa AngieNo ratings yet

- Cost Allocation and Activity Based CostingDocument5 pagesCost Allocation and Activity Based CostingRonalyn delos SantosNo ratings yet

- Activity Based CostingDocument13 pagesActivity Based CostingSudeep D'SouzaNo ratings yet

- Cost SheetDocument20 pagesCost SheetKeshviNo ratings yet

- Cost and Management Accounting 01 _ Class Notes (1)Document114 pagesCost and Management Accounting 01 _ Class Notes (1)saurabhNo ratings yet

- Design1 Lesson 9 - Cost EvaluationDocument96 pagesDesign1 Lesson 9 - Cost EvaluationIzzat IkramNo ratings yet

- Cost CH 3Document40 pagesCost CH 3tewodrosbayisaNo ratings yet

- ABCDocument3 pagesABCATUL KUMARNo ratings yet

- Acc116 G7Document6 pagesAcc116 G7ABDUL HAFIZ ABDULLAHNo ratings yet

- Acct602 Managerial AccountingDocument8 pagesAcct602 Managerial AccountingHaroon KhurshidNo ratings yet

- Unit & Batch CostingDocument25 pagesUnit & Batch CostingragefolioNo ratings yet

- Ch06 Equivalent UnitsDocument51 pagesCh06 Equivalent Unitsvenkataramanan_thiruNo ratings yet

- Activity-Based Costing Chapter04NPPTsDocument49 pagesActivity-Based Costing Chapter04NPPTsDibakar DasNo ratings yet

- 1.3 Activity Based Costing 1.3 Activity Based CostingDocument10 pages1.3 Activity Based Costing 1.3 Activity Based CostingSUHRIT BISWASNo ratings yet

- ABC Slides Final (SP 23)Document11 pagesABC Slides Final (SP 23)Syed Shayan Haider RizviNo ratings yet

- Activity-Based Costing: Questions For Writing and DiscussionDocument28 pagesActivity-Based Costing: Questions For Writing and DiscussionSaratull SafriNo ratings yet

- Activity Based CostingDocument6 pagesActivity Based CostingmisgiegirmaNo ratings yet

- Activity-Based Costing vs Traditional CostingDocument21 pagesActivity-Based Costing vs Traditional CostingKrishna RaiNo ratings yet

- Chapter 3 - Cost AssignmentDocument28 pagesChapter 3 - Cost Assignmentviony catelinaNo ratings yet

- Unit 2 Cost Concepts and Classifications (BBA)Document25 pagesUnit 2 Cost Concepts and Classifications (BBA)Aayushi KothariNo ratings yet

- Chapter 2.4 ABC StudentDocument7 pagesChapter 2.4 ABC StudentnafhahxNo ratings yet

- 4thsem CMA II ActivityBasedCosting by SunitaSaha 19apr2020Document9 pages4thsem CMA II ActivityBasedCosting by SunitaSaha 19apr2020bhupNo ratings yet

- ABC Costing Questions and ExercisesDocument6 pagesABC Costing Questions and ExerciseslinhttisvnuNo ratings yet

- Group 3 Case STUDY 1Document7 pagesGroup 3 Case STUDY 1Rhoel YadaoNo ratings yet

- Management Accounting - Hansen Mowen CH04Document49 pagesManagement Accounting - Hansen Mowen CH04Gito Novhandra100% (5)

- ABC Analysis Reveals Costing Issues$100,00060,000$160,00080,000$30,00015,00010,0008,0006,0005,0004,0003,000$81,000Total budgeted costs.................................................. $321,000Document12 pagesABC Analysis Reveals Costing Issues$100,00060,000$160,00080,000$30,00015,00010,0008,0006,0005,0004,0003,000$81,000Total budgeted costs.................................................. $321,000Parul AbrolNo ratings yet

- MAS-Chapter 7Document3 pagesMAS-Chapter 7Mae CruzNo ratings yet

- CH.08.Unit&Batch CostDocument22 pagesCH.08.Unit&Batch CostRohit AgarwalNo ratings yet

- Learning Unit 4Document70 pagesLearning Unit 4Ndivho MavhethaNo ratings yet

- ch04 Activity Based Costing NewDocument49 pagesch04 Activity Based Costing NewDexxasdNo ratings yet

- KT UnderstandingDocument20 pagesKT UnderstandingJit GhoshNo ratings yet

- CH 4Document16 pagesCH 4Euis Muliawaty NNo ratings yet

- Latest UnitDocument22 pagesLatest UnitNaga ChandraNo ratings yet

- Traditional To ABC CostingDocument37 pagesTraditional To ABC Costingdadali.enterprise6123No ratings yet

- Activity Based CostingDocument25 pagesActivity Based Costingttongoona3No ratings yet

- B01 AbcDocument21 pagesB01 AbcAcca BooksNo ratings yet

- F2 Management Accounting Overheads & Absorption CostingDocument10 pagesF2 Management Accounting Overheads & Absorption CostingCourage KanyonganiseNo ratings yet

- Activity-Based-CostingDocument37 pagesActivity-Based-Costingrehanc20No ratings yet

- Activity-Based CostingDocument46 pagesActivity-Based CostingRiska A. ThamrinNo ratings yet

- Front PageDocument7 pagesFront PageogundaretimmyNo ratings yet

- ABC Costing Optimizes Product CostingDocument3 pagesABC Costing Optimizes Product Costingsajid newaz khanNo ratings yet

- Behavioral Classification of CostDocument22 pagesBehavioral Classification of CostLabib ShahNo ratings yet

- ABC and ABM: Activity-Based Costing and Management ExplainedDocument8 pagesABC and ABM: Activity-Based Costing and Management ExplainedJemNo ratings yet

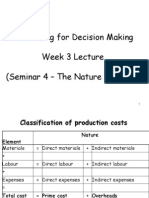

- Accounting For Decision Making Week 3 Lecture (Seminar 4 - The Nature of Costs)Document51 pagesAccounting For Decision Making Week 3 Lecture (Seminar 4 - The Nature of Costs)nwcbenny337No ratings yet

- Seminar 3 - QDocument3 pagesSeminar 3 - QanalsluttyNo ratings yet

- Activity Based CostingDocument27 pagesActivity Based CostingsurendarNo ratings yet

- Activity Based Costing: DR Meena BhatiaDocument23 pagesActivity Based Costing: DR Meena BhatiaAkashbaldwinNo ratings yet

- Topic 5 - Job Costing & Batch CostingDocument5 pagesTopic 5 - Job Costing & Batch CostingMuhammad Alif100% (1)

- How Value Stream Costing WorksDocument4 pagesHow Value Stream Costing Workstanpreet_makkadNo ratings yet

- Activity Based Costing Notes and ExerciseDocument6 pagesActivity Based Costing Notes and Exercisefrancis MagobaNo ratings yet

- Acca F5Document133 pagesAcca F5Andin Lee67% (3)

- Colegio de San Gabriel Arcangel: Learning Module in Strategic Cost Management Unit Title: DurationDocument7 pagesColegio de San Gabriel Arcangel: Learning Module in Strategic Cost Management Unit Title: DurationC XNo ratings yet

- 19728ipcc CA Vol1 Cp9Document22 pages19728ipcc CA Vol1 Cp9manoNo ratings yet

- CMA Part 1 Sec CDocument131 pagesCMA Part 1 Sec CMusthaqMohammedMadathilNo ratings yet

- Accm507: Academic Task I: (Master of Business Administration)Document9 pagesAccm507: Academic Task I: (Master of Business Administration)kunarapu gopi krishnaNo ratings yet

- General Public Schemes2022Document45 pagesGeneral Public Schemes2022tanushree singhNo ratings yet

- Retail Marketing Project at De-Lemon, A Unit of Banaras Beads LTDDocument12 pagesRetail Marketing Project at De-Lemon, A Unit of Banaras Beads LTDtanushree singhNo ratings yet

- DataDocument6 pagesDatatanushree singhNo ratings yet

- Assignment2 1000015918Document8 pagesAssignment2 1000015918tanushree singhNo ratings yet

- Inventory Quiz ProblemsDocument9 pagesInventory Quiz Problemspenny coronado100% (1)

- ASCA301 Module 1 DiscussionDocument22 pagesASCA301 Module 1 DiscussionKaleu MellaNo ratings yet

- Advance Financial Accounting and Reporting: Installment SalesDocument15 pagesAdvance Financial Accounting and Reporting: Installment SalesJason PitosNo ratings yet

- Errors Not Affecting The Trial BalanceDocument4 pagesErrors Not Affecting The Trial BalanceKleeNo ratings yet

- Time Table CS Exams December 2023Document1 pageTime Table CS Exams December 2023Himanshu UpadhyayNo ratings yet

- FAC 1502 Tut Letter 201 With Q&A 2013-1 PDFDocument32 pagesFAC 1502 Tut Letter 201 With Q&A 2013-1 PDFVinny HungweNo ratings yet

- Ais Chapter 5Document37 pagesAis Chapter 5Charlize XabienNo ratings yet

- Accounting Cycle For Service Business - Part 1Document35 pagesAccounting Cycle For Service Business - Part 1Michael MagdaogNo ratings yet

- Answer KeyDocument10 pagesAnswer KeyEvelina Del RosarioNo ratings yet

- Final Examination Chapters 5 & 6Document8 pagesFinal Examination Chapters 5 & 6Marco RegunayanNo ratings yet

- Kaplanlearn - Quiz ContaDocument4 pagesKaplanlearn - Quiz ContaRussell LeyvaNo ratings yet

- CB Chap 3Document39 pagesCB Chap 3Christianne Joyse MerreraNo ratings yet

- 369-Article Text-822-1-10-20200805Document10 pages369-Article Text-822-1-10-20200805Alifia GaneshiNo ratings yet

- Investment in AssociateDocument11 pagesInvestment in AssociateElla MontefalcoNo ratings yet

- Agp Financial AnalysisDocument15 pagesAgp Financial AnalysisDanish KhanNo ratings yet

- 2009-12-08 065812 LaramieDocument2 pages2009-12-08 065812 LaramieRezha Setyo100% (1)

- Accounting contingency theory achievement and future directionsDocument16 pagesAccounting contingency theory achievement and future directionsMarthyn Maturbongs100% (1)

- Week 6 Financial Accoutning Homework HWDocument7 pagesWeek 6 Financial Accoutning Homework HWDoyouknow MENo ratings yet

- Management AccountingDocument304 pagesManagement AccountingRomi Anton100% (2)

- Advanced Management AccountingDocument204 pagesAdvanced Management Accountingmohamad ali osman100% (1)

- Q12013 Consolidated Balance Sheet - Assets UKDocument1 pageQ12013 Consolidated Balance Sheet - Assets UKwellawalalasithNo ratings yet

- Accounting For ManagersDocument286 pagesAccounting For Managersritesh_aladdinNo ratings yet

- INVOICEDocument1 pageINVOICEErwin F. JJ Darwin'sNo ratings yet

- Preweek Auditing Theory 2014Document86 pagesPreweek Auditing Theory 2014Angelica AllanicNo ratings yet

- Break-Even Analysis/Cvp AnalysisDocument41 pagesBreak-Even Analysis/Cvp AnalysisMehwish ziadNo ratings yet

- Ofag Fam 2019 FinalDocument161 pagesOfag Fam 2019 FinalHamse MahirNo ratings yet

- Form 20FDocument398 pagesForm 20FNguyen KyNo ratings yet

- Auditing-Unit 3-VouchingDocument12 pagesAuditing-Unit 3-VouchingAnitha RNo ratings yet

- Hotel Audit Work ProgramDocument60 pagesHotel Audit Work ProgramJean-Paul Hazoume100% (4)

- Army Local Audit Manual (Part I & II)Document561 pagesArmy Local Audit Manual (Part I & II)Varma Mks83% (6)