You might also like

- Bankers Code, Debt Millionaire, Wealthy CodeDocument91 pagesBankers Code, Debt Millionaire, Wealthy CodeJohn Turner100% (2)

- Business Loans Are Easy. . .If You Know the Secrets: If You Know the SecretsFrom EverandBusiness Loans Are Easy. . .If You Know the Secrets: If You Know the SecretsNo ratings yet

- How to Get Started Improving Your Credit: The Inside Information You Need to Avoid Costly Mistakes and Do Things Right the First TimeFrom EverandHow to Get Started Improving Your Credit: The Inside Information You Need to Avoid Costly Mistakes and Do Things Right the First TimeRating: 4 out of 5 stars4/5 (3)

- 10 Reasons Your Loan Is RejectedDocument11 pages10 Reasons Your Loan Is RejectedSyahmie Ramley100% (1)

- How To Use Your Credit Rating To Put You On The Path To Debt FreedomFrom EverandHow To Use Your Credit Rating To Put You On The Path To Debt FreedomNo ratings yet

- The Credit Info/Repair Kit: Your Key To Financial FreedomDocument16 pagesThe Credit Info/Repair Kit: Your Key To Financial FreedomBrittany ElkindNo ratings yet

- Analyzing and Investing in Community Bank StocksDocument234 pagesAnalyzing and Investing in Community Bank StocksRalphVandenAbbeele100% (1)

- Ally-Bank-Statement - Helen ZhaoDocument4 pagesAlly-Bank-Statement - Helen ZhaoJonathan Seagull Livingston100% (1)

- How To Get Great CreditDocument16 pagesHow To Get Great Creditduckey08No ratings yet

- Meaning and Types of Loans ExplainedDocument10 pagesMeaning and Types of Loans ExplainedbondhonbondNo ratings yet

- Credit Analysis What Credit Analyst Look For 5 Cs RatiosDocument6 pagesCredit Analysis What Credit Analyst Look For 5 Cs RatioscuribenNo ratings yet

- Consumer Goes To Mortgage Broker (ABC Mortgages), Usually A Private Corporation WithDocument41 pagesConsumer Goes To Mortgage Broker (ABC Mortgages), Usually A Private Corporation WithStinkiePhish100% (1)

- Transunion NewDocument8 pagesTransunion NewCaleb HolleyNo ratings yet

- Principles of Problem Loan ManagementDocument22 pagesPrinciples of Problem Loan ManagementAsadul Hoque100% (1)

- 06 MoneyDocument4 pages06 Moneywhwei91No ratings yet

- 5 C'sof CreditDocument2 pages5 C'sof CreditarshhussainNo ratings yet

- 4 Problem of Credit Card Debt and How To Solve Them TodayDocument8 pages4 Problem of Credit Card Debt and How To Solve Them Todayfaithworks financialNo ratings yet

- Driving Factors For Banking IndustryDocument10 pagesDriving Factors For Banking Industryavi4studyingNo ratings yet

- Credit Analyst Q&ADocument6 pagesCredit Analyst Q&ASudhir PowerNo ratings yet

- JulDocument7 pagesJulmogambo khushhuaNo ratings yet

- Banks' Lending Functions and Loan ProductsDocument26 pagesBanks' Lending Functions and Loan ProductsAshish Gupta100% (1)

- Bank StatementDocument5 pagesBank Statementshahbaz alamNo ratings yet

- Robo Signer SCRBD VersionDocument112 pagesRobo Signer SCRBD VersionForeclosure Self Defense0% (1)

- FMI - Benefits of Financial IntermediariesDocument11 pagesFMI - Benefits of Financial IntermediariesGaurav Pote100% (2)

- Key BankDocument4 pagesKey BankKelley33% (3)

- Barclays Introduction To Inverse IODocument20 pagesBarclays Introduction To Inverse IOsriramkannaNo ratings yet

- Banking RegulationDocument29 pagesBanking RegulationAngela CerquaNo ratings yet

- Liquidity Management of Citi BankDocument8 pagesLiquidity Management of Citi BankGanesh AppNo ratings yet

- Loan SyndicationDocument11 pagesLoan SyndicationArun DasNo ratings yet

- CH 9 Part 2 Notes EC 113Document6 pagesCH 9 Part 2 Notes EC 113RoselleFayeGarciaTupaNo ratings yet

- Ten Commandments of Commercial LendingDocument4 pagesTen Commandments of Commercial LendingcapitalfinNo ratings yet

- Business Finance and International Economy3 - 2Document4 pagesBusiness Finance and International Economy3 - 2Ayan MitraNo ratings yet

- Chap 012Document15 pagesChap 012van tinh khuc100% (2)

- Silicon Valley Bank AssignmentDocument2 pagesSilicon Valley Bank AssignmentMaazNo ratings yet

- Credit Admin and Support FinalDocument9 pagesCredit Admin and Support FinalJohn Mark CabrejasNo ratings yet

- 5 Cs of CreditDocument5 pages5 Cs of CreditAB AgostoNo ratings yet

- The Industry Handbook: The Banking Industry: Home Dictionary Articles Tutorials Exam Prep Forex Markets SimulaDocument5 pagesThe Industry Handbook: The Banking Industry: Home Dictionary Articles Tutorials Exam Prep Forex Markets SimulaMaverick MeiuNo ratings yet

- Bank Loan DefaultDocument7 pagesBank Loan DefaultGolam Samdanee TaneemNo ratings yet

- Advantages and Disadvantages of Borrowing Money From Lending InstitutionDocument7 pagesAdvantages and Disadvantages of Borrowing Money From Lending InstitutionFEVY BOOTNo ratings yet

- Guard Your Money: Become Financially Literate, Save Money, Protect Your Investments and Even Make More MoneyFrom EverandGuard Your Money: Become Financially Literate, Save Money, Protect Your Investments and Even Make More MoneyNo ratings yet

- 3 - Financial InstitutionsDocument7 pages3 - Financial InstitutionsArmeen KhanNo ratings yet

- FinanceDocument6 pagesFinanceVirajRautNo ratings yet

- Loan CollateralDocument3 pagesLoan CollateralAhmed AlhaddadNo ratings yet

- Valenzuela - Workshop 4Document3 pagesValenzuela - Workshop 4Weiyee ValenzuelaNo ratings yet

- Volcker's Rule: UNION BUDGET 2015 - Banking SectorDocument6 pagesVolcker's Rule: UNION BUDGET 2015 - Banking SectorManu RameshNo ratings yet

- 19th Lecture of Credit AnalysisDocument21 pages19th Lecture of Credit AnalysisM IshtiaqNo ratings yet

- Dr. OgagaDocument108 pagesDr. Ogagamichaelaye64No ratings yet

- Lecture 2 - Business Application of FintechDocument19 pagesLecture 2 - Business Application of Fintechanon_888020909No ratings yet

- FTHB Six Steps Bonus EbookDocument31 pagesFTHB Six Steps Bonus EbookDani's VoicesNo ratings yet

- How Banks Create Money Through Fractional-Reserve BankingDocument14 pagesHow Banks Create Money Through Fractional-Reserve BankingminichelNo ratings yet

- Finance Pytania 3Document6 pagesFinance Pytania 3Marta SzczerskaNo ratings yet

- C PPP PPPPPPPPPPPPP P PP PPDocument7 pagesC PPP PPPPPPPPPPPPP P PP PPWahid MuradNo ratings yet

- Edward Fernandes: 1) California Consumer BankingDocument10 pagesEdward Fernandes: 1) California Consumer Bankingsaghirahmad44No ratings yet

- Assig2 Solutions 112 PgradDocument18 pagesAssig2 Solutions 112 PgradYolanda WuNo ratings yet

- Presentation in Engineering Management: Engr. Eleonor F. DilidiliDocument17 pagesPresentation in Engineering Management: Engr. Eleonor F. DilidiliLenidee San JoseNo ratings yet

- Unit 4Document3 pagesUnit 4Rossi Ana100% (1)

- Incorporate NowDocument32 pagesIncorporate Nowjoseph borketeyNo ratings yet

- Commercial Banking Structure and PrinciplesDocument17 pagesCommercial Banking Structure and PrinciplesshanujssNo ratings yet

- Occasionalpaper: Measuring Microcredit Delinquency: Ratios Can Be Harmful To Your HealthDocument20 pagesOccasionalpaper: Measuring Microcredit Delinquency: Ratios Can Be Harmful To Your HealthdddibalNo ratings yet

- Disadvantages of Conventional BankDocument2 pagesDisadvantages of Conventional Banksyakirah-mustaphaNo ratings yet

- BCOM Financial LiteracyDocument11 pagesBCOM Financial LiteracyVivek GabbuerNo ratings yet

- How Regulators Monitor BanksDocument4 pagesHow Regulators Monitor BanksEhsanul HamidNo ratings yet

- Banking Theory and Practice Chapter FiveDocument23 pagesBanking Theory and Practice Chapter Fivemubarek oumerNo ratings yet

- PDF For Banking Material-04Document8 pagesPDF For Banking Material-04mairaj zafarNo ratings yet

- Corporate Banking Interview Questions: Finance InterviewsDocument8 pagesCorporate Banking Interview Questions: Finance InterviewsbazielNo ratings yet

- 6 things to know before taking a home loanDocument3 pages6 things to know before taking a home loanDrSivasundaram Anushan SvpnsscNo ratings yet

- Bank Definition: What Is A Bank?Document5 pagesBank Definition: What Is A Bank?Aliha FatimaNo ratings yet

- Advanced Accounting QuestionsDocument1 pageAdvanced Accounting Questionsclarisav154No ratings yet

- Assignment 5Document1 pageAssignment 5clarisav154No ratings yet

- Chapter 15 Tax AssessmentDocument2 pagesChapter 15 Tax Assessmentclarisav154No ratings yet

- Chapter 17 LeasesDocument2 pagesChapter 17 Leasesclarisav154No ratings yet

- Auditing Procedures - CashDocument1 pageAuditing Procedures - Cashclarisav154No ratings yet

- Libor Transition A Practical Guide PDFDocument31 pagesLibor Transition A Practical Guide PDFmartaNo ratings yet

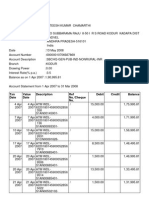

- TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument10 pagesTXN Date Value Date Description Ref No./Cheque No. Debit Credit BalancesatishapexNo ratings yet

- Micro Finance and Micro Credit SHGsDocument33 pagesMicro Finance and Micro Credit SHGsGanesh SamalNo ratings yet

- Functions of Central Bank in An EconomyDocument4 pagesFunctions of Central Bank in An EconomyShafiq MirdhaNo ratings yet

- Research Project On ATM SystemDocument8 pagesResearch Project On ATM Systemgenuinespot100% (1)

- Shahrukh Broadband BillDocument3 pagesShahrukh Broadband BillShah Rukh SNo ratings yet

- Forex Market EquilibriumDocument11 pagesForex Market EquilibriumVishnu VenugopalNo ratings yet

- TOA Loans ReceivablesDocument9 pagesTOA Loans ReceivablesPachiNo ratings yet

- Brockman Guitar Company Is in The Business of Manufacturing Top PDFDocument1 pageBrockman Guitar Company Is in The Business of Manufacturing Top PDFAnbu jaromiaNo ratings yet

- Ack TanDocument1 pageAck TanHIMA HOSPITALNo ratings yet

- General Terms & Conditions For LoansDocument14 pagesGeneral Terms & Conditions For Loansvignesh sNo ratings yet

- Accounts of Blind PersonsDocument8 pagesAccounts of Blind PersonshvenkiNo ratings yet

- Implementation of Islamic Banking in Pakistan By-M.hashaamDocument27 pagesImplementation of Islamic Banking in Pakistan By-M.hashaamSyedMohammadHashaamPirzadaNo ratings yet

- ACC 106 ANSWER - ACCOUNTING EQUATION AND JOURNAL ENTRIESDocument2 pagesACC 106 ANSWER - ACCOUNTING EQUATION AND JOURNAL ENTRIESsiti fatimahNo ratings yet

- Cash and Cash EquivalentsDocument408 pagesCash and Cash EquivalentsJanea ArinyaNo ratings yet

- (TEST BANK and SOL) Bonds PayableDocument6 pages(TEST BANK and SOL) Bonds PayableJhazz DoNo ratings yet

- HANDOUT01 - Cash and Cash EquivalentDocument4 pagesHANDOUT01 - Cash and Cash EquivalentDymphna Ann CalumpianoNo ratings yet

- Official Receipt: Global Indian International SchoolDocument1 pageOfficial Receipt: Global Indian International SchoolBadal BhattacharyaNo ratings yet

- Chapter 12 (Saunders)Document13 pagesChapter 12 (Saunders)sdgdfs sdfsfNo ratings yet

- Bantayan in ActionDocument8 pagesBantayan in ActionSeph TorresNo ratings yet

- Syllabus of Banking & Insurance LawDocument4 pagesSyllabus of Banking & Insurance LawAkshay DhawanNo ratings yet

- MDL ChallanDocument1 pageMDL ChallanPratik V PaliwalNo ratings yet