You might also like

- Types of Negotiable InstrumentDocument3 pagesTypes of Negotiable Instrumentanon_919197283No ratings yet

- DRAWEEDocument4 pagesDRAWEEranticccNo ratings yet

- Types of banking instruments and cheques explainedDocument15 pagesTypes of banking instruments and cheques explainedtriratnacomNo ratings yet

- U.S. Bank Online Banking Terms and Conditions: Effective July 6, 2012Document28 pagesU.S. Bank Online Banking Terms and Conditions: Effective July 6, 2012Monkees LabsNo ratings yet

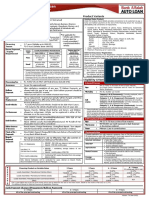

- Alfalah Auto Loan: Policy One PagerDocument1 pageAlfalah Auto Loan: Policy One PagerbilalasifNo ratings yet

- Moving To E-PaymentsDocument8 pagesMoving To E-PaymentsJulieth Alejandra Vargas OchoaNo ratings yet

- What Is A Coupon BondDocument3 pagesWhat Is A Coupon BondNazrul IslamNo ratings yet

- (15-00293 258-7) - Ex. D Promissory Note Gary MillerDocument9 pages(15-00293 258-7) - Ex. D Promissory Note Gary Millerlarry-612445No ratings yet

- Naked Guide to Bonds: What You Need to Know -- Stripped Down to the Bare EssentialsFrom EverandNaked Guide to Bonds: What You Need to Know -- Stripped Down to the Bare EssentialsNo ratings yet

- Discharge of ContractDocument20 pagesDischarge of ContractUtkarsh SethiNo ratings yet

- Bond (Finance) : IssuanceDocument66 pagesBond (Finance) : IssuanceAnonymous 83chWz2voNo ratings yet

- Bank Instruments & Accounts Management: Detecting & Preventing Fraud: With Case Law, Tutorial Notes, Questions & AnswersFrom EverandBank Instruments & Accounts Management: Detecting & Preventing Fraud: With Case Law, Tutorial Notes, Questions & AnswersNo ratings yet

- First Premier-Notice of AcceptanceDocument1 pageFirst Premier-Notice of AcceptanceLaKeishaNo ratings yet

- Webinar on Law Relating to Stamp Duty and PenaltyDocument13 pagesWebinar on Law Relating to Stamp Duty and PenaltySayidNo ratings yet

- Foreign Remittance PRESENTATIONDocument4 pagesForeign Remittance PRESENTATIONprince185No ratings yet

- 2018 Bond Official StatementDocument192 pages2018 Bond Official Statementthe kingfishNo ratings yet

- Bank of America QWR Response 3.7.2014 by Law Firm Blank RomeDocument37 pagesBank of America QWR Response 3.7.2014 by Law Firm Blank RomeIsabel SantamariaNo ratings yet

- MKDocument4 pagesMKRaju RajuNo ratings yet

- HSBC Black Credit Card Terms and Conditions: BenefitsDocument6 pagesHSBC Black Credit Card Terms and Conditions: BenefitsMax Evra7No ratings yet

- BANKING Terms-1Document17 pagesBANKING Terms-1Monika Choudhary100% (1)

- Letter of Credit InstructionsDocument2 pagesLetter of Credit InstructionsHenry Franks100% (2)

- Admiralty Jurisdiction and Amphibious TortsDocument13 pagesAdmiralty Jurisdiction and Amphibious TortsShubhrajit SahaNo ratings yet

- Elements of Banking & InsuranceDocument77 pagesElements of Banking & InsuranceMADHULIKAANo ratings yet

- Law of Banking Notes For Unit WiseDocument59 pagesLaw of Banking Notes For Unit WiseSuyog ChaudhariNo ratings yet

- Banking Law B.com - Docx LatestDocument69 pagesBanking Law B.com - Docx LatestViraja GuruNo ratings yet

- Promissory Note: Borrower: LenderDocument1 pagePromissory Note: Borrower: LenderAmis SteigerNo ratings yet

- AmexDocument12 pagesAmexMohammad BilalNo ratings yet

- 10000001667Document79 pages10000001667Chapter 11 DocketsNo ratings yet

- Instructions for Default Divorce FormsDocument6 pagesInstructions for Default Divorce FormsJNo ratings yet

- Banker and CustomerrelationshipDocument27 pagesBanker and CustomerrelationshipVasu DevanNo ratings yet

- Payments Screens: This Document Describes How The Payments Screens in The Financials Application WorkDocument3 pagesPayments Screens: This Document Describes How The Payments Screens in The Financials Application WorkKui MangusNo ratings yet

- Revised PRA Remittance Instruction Form 1Document1 pageRevised PRA Remittance Instruction Form 1Menchie Ann Sabandal SalinasNo ratings yet

- Tamil Nadu Stamp BillDocument37 pagesTamil Nadu Stamp BillSaravana KumarNo ratings yet

- BMW Financial Services: Consumer Credit ApplicationDocument2 pagesBMW Financial Services: Consumer Credit ApplicationMuhammad Ben Mahfouz Al-ZubairiNo ratings yet

- BLO Unit 1-1Document24 pagesBLO Unit 1-1Mohammad MAAZNo ratings yet

- Fcca DarleneDocument15 pagesFcca DarleneAdele JeterNo ratings yet

- Negotiable Instrument: Sesbreno Vs CADocument19 pagesNegotiable Instrument: Sesbreno Vs CAChris InocencioNo ratings yet

- Deposit Account EssentialsDocument30 pagesDeposit Account EssentialsmattloyaltyNo ratings yet

- Negotiable Instruments Notes: Form and Interpretation (Sec. 1 - 8)Document14 pagesNegotiable Instruments Notes: Form and Interpretation (Sec. 1 - 8)Gennelyn Grace PenaredondoNo ratings yet

- CARDHOLDER DISPUTE FORM-Gift 060910Document2 pagesCARDHOLDER DISPUTE FORM-Gift 060910Joseph StricklerNo ratings yet

- Lettr of CRDocument13 pagesLettr of CRMayank BhatiaNo ratings yet

- BANKING TERMS DEFINITIONSDocument6 pagesBANKING TERMS DEFINITIONShoney30389100% (1)

- Assignments: Banking and FinanceDocument19 pagesAssignments: Banking and FinanceAamir Hussian100% (1)

- Commerci Al L Aw Memory Aid Negotiable Instruments LawDocument11 pagesCommerci Al L Aw Memory Aid Negotiable Instruments LawGold Leonardo100% (1)

- Credit Uniuon Terms and ConditionsDocument1 pageCredit Uniuon Terms and ConditionsTyler cruzNo ratings yet

- Payment Finality and Discharge in Funds TransfersDocument45 pagesPayment Finality and Discharge in Funds Transferssebastian agudeloNo ratings yet

- Letter of Credit (Terms& Conditions& Exhibits)Document3 pagesLetter of Credit (Terms& Conditions& Exhibits)Rnaidoo1972No ratings yet

- How To Read Your RCN BillDocument1 pageHow To Read Your RCN BillMiguel ÁngelNo ratings yet

- Commercial Remittance - State Bank of PakistanDocument13 pagesCommercial Remittance - State Bank of Pakistanmoinahmed99No ratings yet

- Nego TerminologiesDocument15 pagesNego TerminologiesLee SomarNo ratings yet

- Test Question (General Banking)Document43 pagesTest Question (General Banking)siddiqur rahmanNo ratings yet

- Bank Error in Your FavorDocument2 pagesBank Error in Your FavorgargramNo ratings yet

- After Judgement Guide To Getting Results ENDocument25 pagesAfter Judgement Guide To Getting Results ENTim GordashNo ratings yet

- Ch.6 Bills of Exchange Principles of Accounting NotesDocument7 pagesCh.6 Bills of Exchange Principles of Accounting NotesMUHAMMAD AMIRNo ratings yet

- International Project AppraisalDocument4 pagesInternational Project AppraisalMs. Anitharaj M. SNo ratings yet

- Project CrashingDocument6 pagesProject CrashingMs. Anitharaj M. SNo ratings yet

- Credit ServicesDocument4 pagesCredit ServicesMs. Anitharaj M. SNo ratings yet

- Sample LettersDocument15 pagesSample LettersRamya100% (1)

- Other ServicesDocument11 pagesOther ServicesMs. Anitharaj M. SNo ratings yet

- Banking - Other ServicesDocument11 pagesBanking - Other ServicesMs. Anitharaj M. S100% (1)

- Simulation TechniqueDocument2 pagesSimulation TechniqueMs. Anitharaj M. SNo ratings yet

- Risk AnalysisDocument4 pagesRisk AnalysisMs. Anitharaj M. SNo ratings yet

- Stock Exchanges in India: A Guide to Primary and Secondary MarketsDocument16 pagesStock Exchanges in India: A Guide to Primary and Secondary MarketsMs. Anitharaj M. SNo ratings yet

- ACCCOB2 Chapter 2 CASH AND CASH EQUIVALENT EXERCISESDocument15 pagesACCCOB2 Chapter 2 CASH AND CASH EQUIVALENT EXERCISESAyanna CameroNo ratings yet

- FINAL Second Quarter Final Report 2024Document76 pagesFINAL Second Quarter Final Report 2024selamalex737No ratings yet

- CSWDocument49 pagesCSWnickbyfleetNo ratings yet

- Kina Bank Fees Charges ScheduleDocument15 pagesKina Bank Fees Charges SchedulemarcialitovivaresNo ratings yet

- View DocumentDocument3 pagesView DocumentAlex PattersonNo ratings yet

- Dal Mill Project ReportDocument8 pagesDal Mill Project ReportMohan Rao Paturi80% (5)

- UntitledDocument14 pagesUntitledNUR FAZLINA BINTI MAKHTAR KPM-GuruNo ratings yet

- Financial Inclusion NL No 6Document9 pagesFinancial Inclusion NL No 6No MentionNo ratings yet

- ECGCDocument24 pagesECGCShilpa KhannaNo ratings yet

- Financial Ratio Analysis of Sbi (2009 - 2016) : S. Subalakshmi, S. Grahalakshmi and M. ManikandanDocument7 pagesFinancial Ratio Analysis of Sbi (2009 - 2016) : S. Subalakshmi, S. Grahalakshmi and M. ManikandanArchana Mohite100% (1)

- ForfaitingDocument14 pagesForfaitingArun SharmaNo ratings yet

- Idbi Bank Project ReportDocument49 pagesIdbi Bank Project ReportVinay Chawla0% (1)

- Land Bank vs Poblete: Ruling on petition for nullification of land titleDocument7 pagesLand Bank vs Poblete: Ruling on petition for nullification of land titlep95No ratings yet

- Leung Ben vs. P. J. O'BrienDocument3 pagesLeung Ben vs. P. J. O'BrienAnonymous gHx4tm9qm100% (1)

- Fill capital letters form for home loanDocument6 pagesFill capital letters form for home loanvijaycuteNo ratings yet

- Archesh Tiwari (Updated)Document4 pagesArchesh Tiwari (Updated)Archman comethNo ratings yet

- Consequences of Registration of Sale Deed - Burden of Proof When It Is Alleged ShamDocument30 pagesConsequences of Registration of Sale Deed - Burden of Proof When It Is Alleged ShamSridhara babu. N - ಶ್ರೀಧರ ಬಾಬು. ಎನ್No ratings yet

- Project On Credit WorthinessDocument6 pagesProject On Credit Worthinessjuily9No ratings yet

- Impact On Customer Perception Towards ATM Services Provided by The Banks Today: A Conceptual StudyDocument4 pagesImpact On Customer Perception Towards ATM Services Provided by The Banks Today: A Conceptual StudyRizwan Shaikh 44No ratings yet

- Matara HS, Libon, Albay - ATAP PDFDocument1 pageMatara HS, Libon, Albay - ATAP PDFMark Florence SerranoNo ratings yet

- Problem 1Document14 pagesProblem 1SyedNo ratings yet

- Metalurgica Aco-Lar Ltda: Contas Pagas Por Centro de Custo Valores em Reais (R$)Document7 pagesMetalurgica Aco-Lar Ltda: Contas Pagas Por Centro de Custo Valores em Reais (R$)Compras Aço LarNo ratings yet

- Agricultural Credit in BangladeshDocument40 pagesAgricultural Credit in Bangladeshaluka porota80% (5)

- TenderDocument165 pagesTenderAnkur AnilNo ratings yet

- Solution Chapter 6Document10 pagesSolution Chapter 6Clarize R. MabiogNo ratings yet

- ESSEC Brochure - Master - in - Finance PDFDocument20 pagesESSEC Brochure - Master - in - Finance PDFJai KamdarNo ratings yet

- Loan Recovery Literature ReviewDocument6 pagesLoan Recovery Literature Reviewc5jwy8nr100% (1)

- World Bank, IMF, and It's ImpactsDocument24 pagesWorld Bank, IMF, and It's ImpactsAli JumaniNo ratings yet

- A Report On Merchant Banking and Portfolio Management Rules: A Comparison of Bangladesh and IndiaDocument49 pagesA Report On Merchant Banking and Portfolio Management Rules: A Comparison of Bangladesh and IndiaYeasir ArafatNo ratings yet

- Mediobanca Securities Report - 17 Giugno 2013 - "Italy Seizing Up - Caution Required" - Di Antonio GuglielmiDocument88 pagesMediobanca Securities Report - 17 Giugno 2013 - "Italy Seizing Up - Caution Required" - Di Antonio GuglielmiEmanuele Sabetta100% (1)