You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Central Park Apartment Owners Association - Memorandum of AssociationDocument7 pagesThe Central Park Apartment Owners Association - Memorandum of Associationkjacobgeorge124288% (8)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

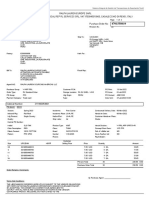

- Transactions: The Barclays Bank A/C 20-77-85 43223280Document2 pagesTransactions: The Barclays Bank A/C 20-77-85 43223280Doris Zhao100% (2)

- Food Quality FactorsDocument19 pagesFood Quality FactorsBubacarr Fatty100% (9)

- TaxReturn2022 1040Document10 pagesTaxReturn2022 1040Trish Hit100% (3)

- Calculating Marginal Revenue From A Linear Dema... - Chegg - Com97Document4 pagesCalculating Marginal Revenue From A Linear Dema... - Chegg - Com97BLESSEDNo ratings yet

- A.M. No. 02-11-10-SCDocument9 pagesA.M. No. 02-11-10-SCRio SanchezNo ratings yet

- ANNEX 1 - Revised People's FOI Manual of The BIRDocument34 pagesANNEX 1 - Revised People's FOI Manual of The BIRRio SanchezNo ratings yet

- ANNEXES 2,3,4-FRO, Process Flow Chart, List of ExceptionsDocument19 pagesANNEXES 2,3,4-FRO, Process Flow Chart, List of ExceptionsRio SanchezNo ratings yet

- RMC No. 128-2019Document1 pageRMC No. 128-2019Rio SanchezNo ratings yet

- 3A, SORIANO and SANCHEZ-Comment - OppositionDocument4 pages3A, SORIANO and SANCHEZ-Comment - OppositionRio SanchezNo ratings yet

- 68-SANCHEZ - Pineda vs. de JesusDocument11 pages68-SANCHEZ - Pineda vs. de JesusRio SanchezNo ratings yet

- Labor Bar Syllabus 2020Document13 pagesLabor Bar Syllabus 2020Ronaldo ValladoresNo ratings yet

- Bar Bulletin 10Document8 pagesBar Bulletin 10xdesczaNo ratings yet

- RMO No. 4-2020Document3 pagesRMO No. 4-2020Rio SanchezNo ratings yet

- 30 - SANCHEZ - Pobre Vs DefensorDocument12 pages30 - SANCHEZ - Pobre Vs DefensorRio SanchezNo ratings yet

- Bar Bulletin 8 PDFDocument7 pagesBar Bulletin 8 PDFFaye Jennifer Pascua PerezNo ratings yet

- PALE Syllabus SUMMERDocument4 pagesPALE Syllabus SUMMERRio SanchezNo ratings yet

- Liability of parents, employers and others under the doctrine of vicarious liabilityDocument14 pagesLiability of parents, employers and others under the doctrine of vicarious liabilityFlorence RoseteNo ratings yet

- Bar Bulletin 7Document20 pagesBar Bulletin 7Alimozaman DiamlaNo ratings yet

- Suggested Answers PUBCORP PDFDocument3 pagesSuggested Answers PUBCORP PDFRio SanchezNo ratings yet

- Midterm Reviewer For TORTS AND DAMAGES 3A 3E PDFDocument20 pagesMidterm Reviewer For TORTS AND DAMAGES 3A 3E PDFRio SanchezNo ratings yet

- Political Party System and Automated Election LawsDocument7 pagesPolitical Party System and Automated Election LawsFlorence RoseteNo ratings yet

- Civil Syllabus PDFDocument14 pagesCivil Syllabus PDFHabib SimbanNo ratings yet

- Case Doctrines PDFDocument3 pagesCase Doctrines PDFRio SanchezNo ratings yet

- Illegal Dismissal Cases in Transport CompaniesDocument42 pagesIllegal Dismissal Cases in Transport CompaniesRio SanchezNo ratings yet

- Midterm Reviewer For TORTS AND DAMAGES 3A 3E PDFDocument20 pagesMidterm Reviewer For TORTS AND DAMAGES 3A 3E PDFRio SanchezNo ratings yet

- ELECTION LAW Case Doctrines PDFDocument24 pagesELECTION LAW Case Doctrines PDFRio SanchezNo ratings yet

- Labrel QuizDocument3 pagesLabrel QuizRio SanchezNo ratings yet

- Pascasio 2017 2018 Samplex Suggested AnswerDocument5 pagesPascasio 2017 2018 Samplex Suggested AnswerRio SanchezNo ratings yet

- Banking Laws and Jurisprudence ReviewerDocument81 pagesBanking Laws and Jurisprudence Reviewermitsudayo_No ratings yet

- ELEC Suggested AnswersDocument3 pagesELEC Suggested AnswersRio SanchezNo ratings yet

- Case Doctrines PDFDocument3 pagesCase Doctrines PDFRio SanchezNo ratings yet

- Elec Law Case Digests - Batch 1Document56 pagesElec Law Case Digests - Batch 1SabritoNo ratings yet

- Pascasio 2017 2018 Samplex Suggested AnswerDocument5 pagesPascasio 2017 2018 Samplex Suggested AnswerRio SanchezNo ratings yet

- 7 1 15Document103 pages7 1 15Gaurish ChoudhuryNo ratings yet

- Module 1 - Administrative Office ProcedureDocument17 pagesModule 1 - Administrative Office ProcedureShayne Candace QuizonNo ratings yet

- IGEM 2016 Key in Enquiry 10 Oct 2016Document38 pagesIGEM 2016 Key in Enquiry 10 Oct 2016rexNo ratings yet

- Do Multiple Large Shareholders Affect Tax Av - 2020 - International Review of EcDocument18 pagesDo Multiple Large Shareholders Affect Tax Av - 2020 - International Review of Ecputri karimahNo ratings yet

- CIR v. NEGROS CONSOLIDATED FARMERS MULTI-PURPOSE COOPERATIVEDocument23 pagesCIR v. NEGROS CONSOLIDATED FARMERS MULTI-PURPOSE COOPERATIVEFaustina del RosarioNo ratings yet

- Cadbury Schweppes Edition 9 WorksheetDocument3 pagesCadbury Schweppes Edition 9 WorksheetLong Dong Mido0% (1)

- Amit Mahajan MindBodyDocument3 pagesAmit Mahajan MindBodychampuyaNo ratings yet

- TECHNOLOGY1 Answer-1Document6 pagesTECHNOLOGY1 Answer-1JlkKumarNo ratings yet

- Posting HFEP Chem & Hema Analyzer June 25, 2020 Ai FinalDocument93 pagesPosting HFEP Chem & Hema Analyzer June 25, 2020 Ai FinalDustin Padilla FormalejoNo ratings yet

- SITRAIN Training Course FeesDocument2 pagesSITRAIN Training Course FeesSead ArifagićNo ratings yet

- Chapter 10 Test BankDocument48 pagesChapter 10 Test BankRujean Salar AltejarNo ratings yet

- Erp Dissertation TopicsDocument8 pagesErp Dissertation TopicsPaySomeoneToWriteAPaperCanada100% (1)

- Go AwayDocument3 pagesGo AwaySharath AlugandulaNo ratings yet

- ANA A. CHUA and MARCELINA HSIA, Complainants, vs. ATTY. SIMEON M. MESINA, JR., RespondentDocument7 pagesANA A. CHUA and MARCELINA HSIA, Complainants, vs. ATTY. SIMEON M. MESINA, JR., Respondentroyel arabejoNo ratings yet

- Resolution Amendingthe Applicable SOLRRateDocument3 pagesResolution Amendingthe Applicable SOLRRateAbbi PerezNo ratings yet

- BST 12 KVS Study Material 2024Document77 pagesBST 12 KVS Study Material 2024Parth AgrawalNo ratings yet

- Audit IT Governance Controls & Structure (39Document132 pagesAudit IT Governance Controls & Structure (39Quendrick Surban100% (1)

- Industrie4.0 Smart Manufacturing For The Future enDocument40 pagesIndustrie4.0 Smart Manufacturing For The Future engorfneshNo ratings yet

- The 4 Types of InnovationDocument8 pagesThe 4 Types of InnovationMoncheNo ratings yet

- Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument8 pagesDate Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceProficient CyberNo ratings yet

- ASG - Amanat Shah Group NextrDocument7 pagesASG - Amanat Shah Group NextrshakibNo ratings yet

- Po 4701558619Document2 pagesPo 4701558619Roger Sebastian Rosas AlzamoraNo ratings yet

- LMC Global Sugar Strategic View 2020 Brochure 1Document17 pagesLMC Global Sugar Strategic View 2020 Brochure 1Ahmed OuhniniNo ratings yet

- Onshore Maintenance Fiber Optic Cable InstallationDocument15 pagesOnshore Maintenance Fiber Optic Cable InstallationAdil IjazNo ratings yet

- Edexcel Business Full Notes-Unit 1Document35 pagesEdexcel Business Full Notes-Unit 1muhamed.ali.2905No ratings yet