You might also like

- The Great Recession: The burst of the property bubble and the excesses of speculationFrom EverandThe Great Recession: The burst of the property bubble and the excesses of speculationNo ratings yet

- The Anatomy of A Crisis: Speculative BubbleDocument3 pagesThe Anatomy of A Crisis: Speculative BubbleVbiidbdiaan ExistimeNo ratings yet

- Q: - "Why Is British Banking in Crisis?" Provide Reasons and Suggest Possible Solutions?Document6 pagesQ: - "Why Is British Banking in Crisis?" Provide Reasons and Suggest Possible Solutions?scorpio786No ratings yet

- Subprime Mortgage Crisis ExplainedDocument4 pagesSubprime Mortgage Crisis ExplainedAnkita NighutNo ratings yet

- The Financial Crisis of 2008: What Happened in Simple TermsDocument2 pagesThe Financial Crisis of 2008: What Happened in Simple TermsBig ALNo ratings yet

- Factors That Led To Global Financial CrisisDocument3 pagesFactors That Led To Global Financial CrisisCharles GarrettNo ratings yet

- Napier University MSC Accounting and Finance Module - Finance ManagementDocument13 pagesNapier University MSC Accounting and Finance Module - Finance ManagementDharmesh PrajapatiNo ratings yet

- FinTech Rising: Navigating the maze of US & EU regulationsFrom EverandFinTech Rising: Navigating the maze of US & EU regulationsRating: 5 out of 5 stars5/5 (1)

- Case Study 1 - What Was The Financial Crisis of 2007-2008Document4 pagesCase Study 1 - What Was The Financial Crisis of 2007-2008Anh NguyenNo ratings yet

- Finance Assignment 2: Financial Crisis of 2008: Housing Market in USADocument2 pagesFinance Assignment 2: Financial Crisis of 2008: Housing Market in USADipankar BasumataryNo ratings yet

- 2008crisissummary1 1Document3 pages2008crisissummary1 1Syed Rafey AbbasNo ratings yet

- Sub-Prime Credit Crisis of 07Document56 pagesSub-Prime Credit Crisis of 07Martin AndelmanNo ratings yet

- DiamondDocument15 pagesDiamondMaxim FilippovNo ratings yet

- US Subprime MortgageDocument9 pagesUS Subprime MortgageN MNo ratings yet

- Banking & Finance Basics Class 8Document39 pagesBanking & Finance Basics Class 8Anèse mabouanaNo ratings yet

- U.S. Subprime Mortgage Crisis (A & B)Document8 pagesU.S. Subprime Mortgage Crisis (A & B)prabhat kumarNo ratings yet

- Case BackgroundDocument7 pagesCase Backgroundabhilash191No ratings yet

- Notes On Basel IIIDocument11 pagesNotes On Basel IIIprat05No ratings yet

- Inside Job documentary summary and key questionsDocument6 pagesInside Job documentary summary and key questionsJill SanghrajkaNo ratings yet

- Mortgage Credit CrisisDocument5 pagesMortgage Credit Crisisasfand yar waliNo ratings yet

- Derivatives (Fin402) : Assignment: EssayDocument5 pagesDerivatives (Fin402) : Assignment: EssayNga Thị NguyễnNo ratings yet

- Sub Prime Overview For Samir 1 Final 97-2003 FormatDocument10 pagesSub Prime Overview For Samir 1 Final 97-2003 FormatAliasgar SuratwalaNo ratings yet

- Bankruptcy of Lehman Brothers - A Pointer of Subprime CrisisDocument7 pagesBankruptcy of Lehman Brothers - A Pointer of Subprime Crisisvidovdan9852No ratings yet

- Financial Crisis of 2007Document6 pagesFinancial Crisis of 2007absolutelyarpitaNo ratings yet

- U110130 IEEP Report MeDocument1 pageU110130 IEEP Report Meanuragnitj9017No ratings yet

- Course File 3-AssessmentDocument5 pagesCourse File 3-AssessmentLilibeth OrongNo ratings yet

- Subprime Mortgage CrisisDocument18 pagesSubprime Mortgage Crisisredheattauras0% (1)

- VF The GFC and Debt CrisisDocument28 pagesVF The GFC and Debt CrisisMehdi SamNo ratings yet

- Anul III Trad Business English Part III 15 Noiembrie 2014Document6 pagesAnul III Trad Business English Part III 15 Noiembrie 2014Ana-Maria Dumitroiu0% (1)

- Risk Management Failures During The Financial Crisis: November 2011Document27 pagesRisk Management Failures During The Financial Crisis: November 2011Khushi ShahNo ratings yet

- Case Study On Subprime CrisisDocument24 pagesCase Study On Subprime CrisisNakul SainiNo ratings yet

- UssamaDocument12 pagesUssamaRizwan RizzuNo ratings yet

- The Great Recession 2007-09Document8 pagesThe Great Recession 2007-09Muhammad Taha AmerjeeNo ratings yet

- FI K204040181 - TranGiaHanDocument7 pagesFI K204040181 - TranGiaHanHân TrầnNo ratings yet

- Financial Instruments Responsible For Global Financial CrisisDocument15 pagesFinancial Instruments Responsible For Global Financial Crisisabhishek gupte100% (4)

- ProjectDocument7 pagesProjectmalik waseemNo ratings yet

- 2007 Subprime Mortgage Financial CrisisDocument12 pages2007 Subprime Mortgage Financial CrisisMuhammad Arief Billah100% (8)

- Causes of the Financial CrisisDocument2 pagesCauses of the Financial CrisisJoaquim MorenoNo ratings yet

- C061 - Enverga - Reaction PaperDocument4 pagesC061 - Enverga - Reaction Paperliberace cabreraNo ratings yet

- Chapter 7: International Banking and Money MarketDocument2 pagesChapter 7: International Banking and Money MarketVeeranjaneyulu KacherlaNo ratings yet

- NINJA Loans To Blame For Financial CrisisDocument25 pagesNINJA Loans To Blame For Financial Crisischapy86No ratings yet

- Mortage Crises. (Adeel Ahmad)Document6 pagesMortage Crises. (Adeel Ahmad)Adeel AhmadNo ratings yet

- Why Giants Like Lehman Brothers & Many More FailedDocument12 pagesWhy Giants Like Lehman Brothers & Many More Failedtarunsoni88No ratings yet

- Sub Prime Crisis....Document18 pagesSub Prime Crisis....vidha_s23No ratings yet

- Crisis FinancieraDocument4 pagesCrisis Financierahawk91No ratings yet

- Financial Crisis 2Document12 pagesFinancial Crisis 2neevanjain121No ratings yet

- 2008 Financial CrisisDocument9 pages2008 Financial CrisisalexNo ratings yet

- Safi Ullah BBA-7 (B) 011-18-0047Document10 pagesSafi Ullah BBA-7 (B) 011-18-0047Mir safi balochNo ratings yet

- Subprime Crisis FeiDocument13 pagesSubprime Crisis FeiDavuluri SasiNo ratings yet

- The Collapse of Continental IllinoisDocument7 pagesThe Collapse of Continental IllinoisginaNo ratings yet

- Financial InstituitionsDocument2 pagesFinancial InstituitionsSidra NadeemNo ratings yet

- Causes and Effects of Economic and Financial CrisesDocument26 pagesCauses and Effects of Economic and Financial Criseshizkel hermNo ratings yet

- G22005 - U.S. Subprime Mortgage CrisisDocument6 pagesG22005 - U.S. Subprime Mortgage Crisisamrithap10No ratings yet

- The Financial Crisis of 2008Document2 pagesThe Financial Crisis of 2008Soufiane ZibouhNo ratings yet

- Subprime Mortgage CrisisDocument12 pagesSubprime Mortgage Crisiskrishna sunilNo ratings yet

- How Destruction Happened?: FICO Score S of Below 620. Because TheseDocument5 pagesHow Destruction Happened?: FICO Score S of Below 620. Because ThesePramod KhandelwalNo ratings yet

- Market Uncertainties and Measures of ECBDocument4 pagesMarket Uncertainties and Measures of ECBAkshat GoelNo ratings yet

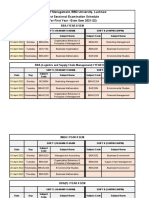

- Scheme - Ii Sessional For First Year Students Even Sem 2021-22Document3 pagesScheme - Ii Sessional For First Year Students Even Sem 2021-22Neeraj MauryaNo ratings yet

- SCHEME - Ist SESSIONAL FOR FIRST YEAR STUDENTS EVEN SEM 2021-22Document3 pagesSCHEME - Ist SESSIONAL FOR FIRST YEAR STUDENTS EVEN SEM 2021-22Neeraj MauryaNo ratings yet

- Adobe Scan 2 Jun 2022hankakDocument25 pagesAdobe Scan 2 Jun 2022hankakNeeraj MauryaNo ratings yet

- Personnel Management ObjectivesDocument4 pagesPersonnel Management ObjectivesNeeraj MauryaNo ratings yet

- TQM (Total Quality Management)Document8 pagesTQM (Total Quality Management)Neeraj MauryaNo ratings yet

- Ravi Kumar KiDocument18 pagesRavi Kumar KiNeeraj MauryaNo ratings yet

- SYMP Flyer of EconomicsDocument2 pagesSYMP Flyer of EconomicsNeeraj MauryaNo ratings yet

- JIT (Just in Time)Document12 pagesJIT (Just in Time)Neeraj MauryaNo ratings yet