You might also like

- bispap128Document23 pagesbispap128BhanusreeNo ratings yet

- E Naira Digital Currency and Financial Performance of Listed Deposit Money Banks in NigeriaDocument8 pagesE Naira Digital Currency and Financial Performance of Listed Deposit Money Banks in NigeriaEditor IJTSRDNo ratings yet

- I - CNBC Indonesia - 101223 - Digital Rupiah Issuance 2024, Explanation From BI BossDocument3 pagesI - CNBC Indonesia - 101223 - Digital Rupiah Issuance 2024, Explanation From BI BossAuviNo ratings yet

- Rene Ndekwe International Business ADocument5 pagesRene Ndekwe International Business ARene NdekweNo ratings yet

- Significant Effect of The Central Bank Digital Currency On The Design of Monetary PolicyDocument28 pagesSignificant Effect of The Central Bank Digital Currency On The Design of Monetary PolicyArif RamadhanNo ratings yet

- Monetary Policy, Central Bank Digital Currency: A Study in VietnamDocument10 pagesMonetary Policy, Central Bank Digital Currency: A Study in Vietnamindex PubNo ratings yet

- Digital CurrencyDocument17 pagesDigital CurrencyHanumanthNo ratings yet

- Forum 20211124wp enDocument29 pagesForum 20211124wp enErinda MalajNo ratings yet

- Central Bank Digital Currencies and The Future of Money Part1Document10 pagesCentral Bank Digital Currencies and The Future of Money Part105-Xll C-Riya BaskeyNo ratings yet

- Are Economic Factors Driving BitCoin Transactions An Analysis of Select EconomiesDocument13 pagesAre Economic Factors Driving BitCoin Transactions An Analysis of Select EconomiesLeandro LopesNo ratings yet

- Central Bank Digital CurrencyDocument28 pagesCentral Bank Digital CurrencyBlack JewNo ratings yet

- Role of Islamic Finance in The Face of The Digital Currency RevolutionDocument11 pagesRole of Islamic Finance in The Face of The Digital Currency RevolutionMuhammad RizwanNo ratings yet

- Everything You Need To Know About Chinas Digitized CurrencyrkqiuDocument5 pagesEverything You Need To Know About Chinas Digitized Currencyrkqiujamesleg4No ratings yet

- Black Book Jatin Vaja 52Document29 pagesBlack Book Jatin Vaja 52Jatin VajaNo ratings yet

- Technological Advances in Recent Years Have Led To A Growing Number of FastDocument4 pagesTechnological Advances in Recent Years Have Led To A Growing Number of Fastnabila tasanNo ratings yet

- Edcoin: - Project OverviewDocument10 pagesEdcoin: - Project OverviewEnitan BelloNo ratings yet

- Project Proposal For Emergence of Ewallet in NepalDocument11 pagesProject Proposal For Emergence of Ewallet in NepalChandan YadavNo ratings yet

- Everything You Must Know About The Chinese Digital CurrencylrqlhDocument5 pagesEverything You Must Know About The Chinese Digital Currencylrqlhsingeraries9No ratings yet

- The Effect of Cashless Banking On Ethiopian EconomyDocument11 pagesThe Effect of Cashless Banking On Ethiopian EconomyAnonymous kbmKQLe0JNo ratings yet

- Everything You Need To Learn About Chinas Digital CurrencymqnyaDocument5 pagesEverything You Need To Learn About Chinas Digital Currencymqnyabakeralley5No ratings yet

- EcoMatrix KKDocument5 pagesEcoMatrix KKKunal KumarNo ratings yet

- Research On The Impact of Digital Currency On Commercial BanksDocument5 pagesResearch On The Impact of Digital Currency On Commercial Banks05-Xll C-Riya BaskeyNo ratings yet

- Economies 08 000412Document28 pagesEconomies 08 000412Keamogetse MotlogeloaNo ratings yet

- The Future of Merchant Crypto PaymentsDocument25 pagesThe Future of Merchant Crypto PaymentsYudha Sidhikoro AjiNo ratings yet

- The Role of RBI On Implementation of Digital Currencies in IndiaDocument5 pagesThe Role of RBI On Implementation of Digital Currencies in IndiaEditor IJTSRDNo ratings yet

- Everything You Need To Be Aware of About Chinas Digital CurrencyzkgzuDocument5 pagesEverything You Need To Be Aware of About Chinas Digital Currencyzkgzubailend5No ratings yet

- What Is Central Bank Digital CurrencyDocument5 pagesWhat Is Central Bank Digital Currencyguptaom9839No ratings yet

- 209 290 43 MoneyAndBankingDocument12 pages209 290 43 MoneyAndBankingPalak GuptaNo ratings yet

- The Future of Merchant Crypto PaymentsDocument25 pagesThe Future of Merchant Crypto PaymentsGideon ListanoNo ratings yet

- Operational Aspects of Digital Yuan: From Minting To SpendingDocument3 pagesOperational Aspects of Digital Yuan: From Minting To SpendingJohnson JayNo ratings yet

- A Study On Digital Payments System & Consumer Perception: An Empirical SurveyDocument11 pagesA Study On Digital Payments System & Consumer Perception: An Empirical SurveyDeepa VishwakarmaNo ratings yet

- Crypto Currency Landscape in IndiaDocument3 pagesCrypto Currency Landscape in IndiaYADAVAMITKUMAR007No ratings yet

- 448-Article Text-1098-1-10-20201117Document13 pages448-Article Text-1098-1-10-20201117Digital Pergola100% (1)

- Digital Payments: Challenges and Solutions: Srihari Kulkarni, Abdul Shahanaz TajDocument6 pagesDigital Payments: Challenges and Solutions: Srihari Kulkarni, Abdul Shahanaz Tajnilofer shallyNo ratings yet

- Economies 08 00041 v2Document27 pagesEconomies 08 00041 v2DonaldNo ratings yet

- Digital Finance - UNIT 1Document7 pagesDigital Finance - UNIT 1NAVYA JUNEJA 2023323No ratings yet

- The Development and Impact of Central Bank Digital Currency: Xujia Huang, Ziyu Yang, Chenkai ZhouDocument6 pagesThe Development and Impact of Central Bank Digital Currency: Xujia Huang, Ziyu Yang, Chenkai Zhouyinfu822No ratings yet

- 2. Reading 2 (Tronnier 2022)Document13 pages2. Reading 2 (Tronnier 2022)Nhật Linh NguyễnNo ratings yet

- F 3251 SuerfDocument9 pagesF 3251 SuerfMai ngoc thangNo ratings yet

- CBDC ProposalDocument5 pagesCBDC ProposalUt PearlsNo ratings yet

- Virtual Taka in Bangladesh ContextDocument3 pagesVirtual Taka in Bangladesh ContextMohammad Shahjahan SiddiquiNo ratings yet

- F 3251 SuerfDocument9 pagesF 3251 SuerfMai ngoc thangNo ratings yet

- Summary of Business ReportDocument13 pagesSummary of Business ReportGungun GoyalNo ratings yet

- Visa Digital Currency OverviewDocument12 pagesVisa Digital Currency OverviewViviane BocalonNo ratings yet

- Topic 2 - The Benfits and Limitations of Digital Currency in India - Corporate Tax PlanningDocument34 pagesTopic 2 - The Benfits and Limitations of Digital Currency in India - Corporate Tax PlanningRohit GhaiNo ratings yet

- 5 Tronnier 2022 (CBDC Privacy)Document21 pages5 Tronnier 2022 (CBDC Privacy)Phạm Hoàng YếnNo ratings yet

- Level of Awareness and Adoption of Cryptocurrency Among College Students in General Santos CityDocument36 pagesLevel of Awareness and Adoption of Cryptocurrency Among College Students in General Santos CityMelanie SamsonaNo ratings yet

- Future of Money Blume Part2Document45 pagesFuture of Money Blume Part2Jai AggarwalNo ratings yet

- Role of Govt in Digital EconomyDocument3 pagesRole of Govt in Digital EconomySayan SahayNo ratings yet

- REVIEW LITERATURE Digital PaymentsDocument7 pagesREVIEW LITERATURE Digital PaymentsMahimalluru Charan KumarNo ratings yet

- Why 2020 Is The Year of StablecoinDocument2 pagesWhy 2020 Is The Year of StablecoinHola HfsaNo ratings yet

- Interest in Using E-Wallet On The Millennial Generation in Special Region of Yogyakarta (Journal 2021)Document19 pagesInterest in Using E-Wallet On The Millennial Generation in Special Region of Yogyakarta (Journal 2021)Elma Roxanne DalaNo ratings yet

- E-Payment System in Saudi Arabia PDFDocument16 pagesE-Payment System in Saudi Arabia PDFRohan MehtaNo ratings yet

- International PaymentsDocument27 pagesInternational PaymentsVy TranNo ratings yet

- What Are Bitcoins and Virtual CurrenciesDocument5 pagesWhat Are Bitcoins and Virtual CurrenciesIleana Mariaa StoenescuNo ratings yet

- Thuc Trang Su Dung Vi Dien Tu Tai Viet NamDocument45 pagesThuc Trang Su Dung Vi Dien Tu Tai Viet NamMin Chan JungNo ratings yet

- Adoption of Digital Payment System by Consumer: A Review of LiteratureDocument8 pagesAdoption of Digital Payment System by Consumer: A Review of LiteratureRavi VermaNo ratings yet

- Crypto Currencies and Their Impact On Economy and Banking SystemsDocument18 pagesCrypto Currencies and Their Impact On Economy and Banking SystemsZohaib AliNo ratings yet

- Honduras Tech University Bitcoin HomeworkDocument8 pagesHonduras Tech University Bitcoin HomeworkJuditNo ratings yet

- Mary T ReportDocument44 pagesMary T ReportAbdulrahman AhmadNo ratings yet

- Soil OrganismDocument15 pagesSoil OrganismAbdulrahman AhmadNo ratings yet

- Department of Accounting and TaxationDocument1 pageDepartment of Accounting and TaxationAbdulrahman AhmadNo ratings yet

- HRM AssignmentDocument6 pagesHRM AssignmentAbdulrahman AhmadNo ratings yet

- Introduction 12Document4 pagesIntroduction 12Abdulrahman AhmadNo ratings yet

- GIS Methods Chapter 3 NigeriaDocument3 pagesGIS Methods Chapter 3 NigeriaAbdulrahman AhmadNo ratings yet

- IDFC FIRST Bank StatementDocument4 pagesIDFC FIRST Bank StatementRutvik PandyaNo ratings yet

- Contoh Remittance AdviceDocument1 pageContoh Remittance AdviceFATAHILLAH SHOLAHUDDINSWARDANINo ratings yet

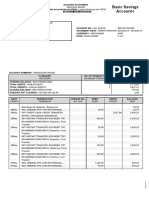

- Basic Savings Account-I: Penyata AkaunDocument3 pagesBasic Savings Account-I: Penyata AkaunIhsan Mazlan100% (3)

- Account Statement: Penyata AkaunDocument54 pagesAccount Statement: Penyata AkaunAthirah Zulkiflee100% (1)

- Digital Payment Methods in IndiaDocument71 pagesDigital Payment Methods in Indiavinayak tiwariNo ratings yet

- e-StatementBRImo 353101003955505 Aug2023 20230907 232957Document4 pagese-StatementBRImo 353101003955505 Aug2023 20230907 232957AereeNo ratings yet

- Bulk Credit Card DetailsDocument2 pagesBulk Credit Card Detailstyler100% (4)

- Ecran TelefonDocument3 pagesEcran TelefonAlexandra Adriana RaduNo ratings yet

- B2B Collaboration Flowchart: Electronic MallDocument1 pageB2B Collaboration Flowchart: Electronic MallanggonoutomoNo ratings yet

- E-Wallet Penetration - Literature Review 2Document2 pagesE-Wallet Penetration - Literature Review 2kirankumarchandra100% (1)

- Get More Ecommerce Sales with Trending TacticsDocument9 pagesGet More Ecommerce Sales with Trending TacticsOasysNo ratings yet

- Master-TSP-ListSBDG TSPslist V11.2 LatestDocument358 pagesMaster-TSP-ListSBDG TSPslist V11.2 LatestIsmed Ulam Raja100% (1)

- E-Banking Practices in Selected Public and Private Sector BanksDocument6 pagesE-Banking Practices in Selected Public and Private Sector BanksJournal of Computer ApplicationsNo ratings yet

- 2017 Fintech 50 PDFDocument80 pages2017 Fintech 50 PDFHenkholal HaokipNo ratings yet

- Buy Verified CashApp AccountDocument11 pagesBuy Verified CashApp AccountDonnie SanchezNo ratings yet

- Cash Receipt TemplateDocument1 pageCash Receipt TemplateCristine BilocuraNo ratings yet

- 1711087820916iifk3tRuaIZUbEyyDocument3 pages1711087820916iifk3tRuaIZUbEyyashutoshbbk786No ratings yet

- Statement Bank March Delavid Distributor LLC A2cb2f38f9Document10 pagesStatement Bank March Delavid Distributor LLC A2cb2f38f9Madelyn Vasquez100% (1)

- IFFMDocument8 pagesIFFMNishant AnandNo ratings yet

- ISG PAY - Integration Document - V1 2 LatestDocument26 pagesISG PAY - Integration Document - V1 2 LatestjyothimarkalNo ratings yet

- Test Card CreditDocument32 pagesTest Card CreditHerard Gravi100% (4)

- E StatementDocument3 pagesE StatementTimmy Sze0% (1)

- American Express - BS 2019Document1 pageAmerican Express - BS 2019Max PatelNo ratings yet

- SBI EPay Payment AggregatorDocument17 pagesSBI EPay Payment Aggregatorsrinivasa annamayya100% (1)

- Payment Systems Department: Head Office, Dhaka 1000Document6 pagesPayment Systems Department: Head Office, Dhaka 1000Ashok Chandra HalderNo ratings yet

- CPSPM 66127250 1675446430Document36 pagesCPSPM 66127250 1675446430Vikas100% (2)

- Crypto Currency and Block ChainDocument38 pagesCrypto Currency and Block ChainShabeel ShabuNo ratings yet

- Fintech Research PaperDocument14 pagesFintech Research Paperaulia amartiwiNo ratings yet

- PDFDocument2 pagesPDFSanjiv VermaNo ratings yet

- Debit Mandate Form NACH / ECS / DIRECT DEBIT: Mthly Qtly H-Yrly Yrly As & When PresentedDocument1 pageDebit Mandate Form NACH / ECS / DIRECT DEBIT: Mthly Qtly H-Yrly Yrly As & When PresentedPerumal sNo ratings yet

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialNo ratings yet

- Venture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistFrom EverandVenture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistRating: 4.5 out of 5 stars4.5/5 (73)

- Joy of Agility: How to Solve Problems and Succeed SoonerFrom EverandJoy of Agility: How to Solve Problems and Succeed SoonerRating: 4 out of 5 stars4/5 (1)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 4.5 out of 5 stars4.5/5 (14)

- The Caesars Palace Coup: How a Billionaire Brawl Over the Famous Casino Exposed the Power and Greed of Wall StreetFrom EverandThe Caesars Palace Coup: How a Billionaire Brawl Over the Famous Casino Exposed the Power and Greed of Wall StreetRating: 5 out of 5 stars5/5 (2)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisFrom EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisRating: 5 out of 5 stars5/5 (6)

- Mastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsFrom EverandMastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsNo ratings yet

- Financial Risk Management: A Simple IntroductionFrom EverandFinancial Risk Management: A Simple IntroductionRating: 4.5 out of 5 stars4.5/5 (7)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelFrom Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelNo ratings yet

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursFrom EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursRating: 4.5 out of 5 stars4.5/5 (34)

- Investment Valuation: Tools and Techniques for Determining the Value of any Asset, University EditionFrom EverandInvestment Valuation: Tools and Techniques for Determining the Value of any Asset, University EditionRating: 5 out of 5 stars5/5 (1)

- Value: The Four Cornerstones of Corporate FinanceFrom EverandValue: The Four Cornerstones of Corporate FinanceRating: 4.5 out of 5 stars4.5/5 (18)

- Product-Led Growth: How to Build a Product That Sells ItselfFrom EverandProduct-Led Growth: How to Build a Product That Sells ItselfRating: 5 out of 5 stars5/5 (1)

- How to Measure Anything: Finding the Value of Intangibles in BusinessFrom EverandHow to Measure Anything: Finding the Value of Intangibles in BusinessRating: 3.5 out of 5 stars3.5/5 (4)

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingFrom EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingRating: 4.5 out of 5 stars4.5/5 (17)

- Add Then Multiply: How small businesses can think like big businesses and achieve exponential growthFrom EverandAdd Then Multiply: How small businesses can think like big businesses and achieve exponential growthNo ratings yet

- Ready, Set, Growth hack:: A beginners guide to growth hacking successFrom EverandReady, Set, Growth hack:: A beginners guide to growth hacking successRating: 4.5 out of 5 stars4.5/5 (93)

- Financial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityFrom EverandFinancial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityRating: 4.5 out of 5 stars4.5/5 (4)

- Startup CEO: A Field Guide to Scaling Up Your Business (Techstars)From EverandStartup CEO: A Field Guide to Scaling Up Your Business (Techstars)Rating: 4.5 out of 5 stars4.5/5 (4)

- Warren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorFrom EverandWarren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorNo ratings yet

- Note Brokering for Profit: Your Complete Work At Home Success ManualFrom EverandNote Brokering for Profit: Your Complete Work At Home Success ManualNo ratings yet