You might also like

- ACCA - F4 (ENG) Corporate and Business Law - Progress TestsDocument20 pagesACCA - F4 (ENG) Corporate and Business Law - Progress TestsSyed Muzaffar Ali Shah100% (2)

- Ma Mod4 W08Document221 pagesMa Mod4 W08Randy KuswantoNo ratings yet

- CH 5Document51 pagesCH 5Angely May JordanNo ratings yet

- Stephen Paddock NV PDFDocument294 pagesStephen Paddock NV PDFChris vegasNo ratings yet

- Answers To Chapter 4 Exercises: Review and Practice ExercisesDocument10 pagesAnswers To Chapter 4 Exercises: Review and Practice ExercisesHuyen NguyenNo ratings yet

- MA and FMA Full Specimen Exam Answers - 2Document14 pagesMA and FMA Full Specimen Exam Answers - 2zunndraaNo ratings yet

- Break-Even Point and Cost-Volume-Profit Analysis: QuestionsDocument34 pagesBreak-Even Point and Cost-Volume-Profit Analysis: QuestionsGuinevereNo ratings yet

- CH 13Document35 pagesCH 13billybuttonNo ratings yet

- Break-Even Point and Cost-Volume-Profit Analysis: QuestionsDocument39 pagesBreak-Even Point and Cost-Volume-Profit Analysis: QuestionsElijah MontefalcoNo ratings yet

- Ebook Cornerstones of Managerial Accounting Canadian 3Rd Edition Mowen Solutions Manual Full Chapter PDFDocument51 pagesEbook Cornerstones of Managerial Accounting Canadian 3Rd Edition Mowen Solutions Manual Full Chapter PDFxaviaalexandrawp86i100% (12)

- Chapter 2 Marginal CostingDocument21 pagesChapter 2 Marginal CostingLan Nhi NguyenNo ratings yet

- Chapter 8 MowenDocument25 pagesChapter 8 MowenRosamae PialaneNo ratings yet

- MA2 Mock 1-As - 2023-24Document8 pagesMA2 Mock 1-As - 2023-24daniel.maina2005No ratings yet

- Session-16-17-18-CVP AnalysisDocument78 pagesSession-16-17-18-CVP Analysis020Abhisek KhadangaNo ratings yet

- CostingDocument4 pagesCostingDatz HuynhNo ratings yet

- Absorption and Variable Costing, and Inventory Management: Discussion QuestionsDocument28 pagesAbsorption and Variable Costing, and Inventory Management: Discussion QuestionsParth GandhiNo ratings yet

- Chapter 7: Cost-Volume-Profit Analysis Questions: Solutions ManualDocument49 pagesChapter 7: Cost-Volume-Profit Analysis Questions: Solutions ManualdarraNo ratings yet

- SD17 Hybrid F5 Section C Answers Clean Proof PDFDocument12 pagesSD17 Hybrid F5 Section C Answers Clean Proof PDFShaksham SharmaNo ratings yet

- Chapter 4 Answer Cost AccountingDocument19 pagesChapter 4 Answer Cost AccountingJuline Ashley A CarballoNo ratings yet

- Bilu Chap 3Document16 pagesBilu Chap 3borena extensionNo ratings yet

- Cost and Management Accounting Unit 2Document38 pagesCost and Management Accounting Unit 2Minisha GuptaNo ratings yet

- Lecture 5Document39 pagesLecture 5Shixi ZhuNo ratings yet

- Flexible BudgetDocument15 pagesFlexible BudgetDawit AmahaNo ratings yet

- Managerial Accounting 5th Edition Jiambalvo Solutions ManualDocument25 pagesManagerial Accounting 5th Edition Jiambalvo Solutions Manualnhattranel7k1100% (28)

- Managerial CH6 GarriDocument74 pagesManagerial CH6 GarriDalia ElarabyNo ratings yet

- CHAPTER FOUR Cost and MGMT ACCTDocument12 pagesCHAPTER FOUR Cost and MGMT ACCTFeleke TerefeNo ratings yet

- Taller Costeo VariablesDocument10 pagesTaller Costeo VariablesKaroll Joseph Sanchez AlmaralesNo ratings yet

- 107-W7-8-Variable cost-chp05-STDocument48 pages107-W7-8-Variable cost-chp05-STmargaret mariaNo ratings yet

- The Master Budget and Flexible Budgeting: Lecture # 17Document24 pagesThe Master Budget and Flexible Budgeting: Lecture # 17mzNo ratings yet

- Group AssignmentDocument6 pagesGroup AssignmentMuzie Bhengu GoqoloNo ratings yet

- Cost-Management-Accounting-System 3Document89 pagesCost-Management-Accounting-System 3MollaNo ratings yet

- Garrison CH06 AccessibleDocument74 pagesGarrison CH06 AccessibleAlice WuNo ratings yet

- 69 Budgetary Control and Reporting NotesDocument7 pages69 Budgetary Control and Reporting Notesgetcultured69No ratings yet

- Marginal and Absorption CostingDocument8 pagesMarginal and Absorption CostingEniola OgunmonaNo ratings yet

- CMA Class 9 Def FDocument69 pagesCMA Class 9 Def FshishirNo ratings yet

- Cost Accounting and ControlDocument5 pagesCost Accounting and ControlJell DemocerNo ratings yet

- Chapter 13 - Relevant Costs For Decision Making PDFDocument34 pagesChapter 13 - Relevant Costs For Decision Making PDFnafin ayub ArilNo ratings yet

- Flexible BudgetDocument15 pagesFlexible BudgetDawit AmahaNo ratings yet

- Profitability DecisionsDocument9 pagesProfitability DecisionsthekaustuvNo ratings yet

- Cost and Management AccountingDocument11 pagesCost and Management AccountingAlfred MwayutaNo ratings yet

- Chapter Four: Supply I: Managerial Economics Lecturer: Chu-Bin Lin Southwest Jiaotong UniversityDocument27 pagesChapter Four: Supply I: Managerial Economics Lecturer: Chu-Bin Lin Southwest Jiaotong Universitymaria rafiqNo ratings yet

- Cost-Volume-Profit Analysis: A Managerial Planning Tool: Discussion QuestionsDocument48 pagesCost-Volume-Profit Analysis: A Managerial Planning Tool: Discussion QuestionsParth GandhiNo ratings yet

- Chapter 12Document72 pagesChapter 12Samaaraa NorNo ratings yet

- Contribution Price. This Contribution Approach To Pricing Is Most Appropriate When: (1) There Is ADocument7 pagesContribution Price. This Contribution Approach To Pricing Is Most Appropriate When: (1) There Is AEVELYN ROSE MOGAONo ratings yet

- Ch5 LimitingFactorsDocument19 pagesCh5 LimitingFactorsali202101No ratings yet

- Variable & Absorption Costing LectureDocument11 pagesVariable & Absorption Costing LectureElisha Dhowry PascualNo ratings yet

- Chapter 10Document13 pagesChapter 10Tran Huong GiangNo ratings yet

- 02 Profit PlanningDocument32 pages02 Profit PlanningJelliane de la CruzNo ratings yet

- Group 2 Econ ReportingDocument32 pagesGroup 2 Econ ReportingRhesel Kate Endriga TrigoNo ratings yet

- Managerial Accounting 6th Edition Jiambalvo Solutions ManualDocument24 pagesManagerial Accounting 6th Edition Jiambalvo Solutions Manualgenevievetruong9ajpr100% (28)

- Differential AnalysísDocument88 pagesDifferential AnalysísJanes VuNo ratings yet

- Managerial Accounting The Cornerstone of Business Decision Making 7Th Edition Mowen Solutions Manual Full Chapter PDFDocument63 pagesManagerial Accounting The Cornerstone of Business Decision Making 7Th Edition Mowen Solutions Manual Full Chapter PDFKennethRiosmqoz100% (14)

- Solutions To Week 3 Practice Text ExercisesDocument6 pagesSolutions To Week 3 Practice Text Exercisespinkgold48No ratings yet

- Ch13. Flexible Budget-AkmDocument44 pagesCh13. Flexible Budget-AkmPANDHARE SIDDHESHNo ratings yet

- Variable Costing: A Tool For Management: © 2010 The Mcgraw-Hill Companies, IncDocument29 pagesVariable Costing: A Tool For Management: © 2010 The Mcgraw-Hill Companies, IncTurbo TechNo ratings yet

- Chapter 2 Cost Concepts and Design Economics PART 2 With AssignmentDocument30 pagesChapter 2 Cost Concepts and Design Economics PART 2 With AssignmentrplagrosaNo ratings yet

- MA & CA-Merginal & Absorption Costing PDFDocument8 pagesMA & CA-Merginal & Absorption Costing PDFRashfi RussellNo ratings yet

- IPE48116 MainulBari S04 Ch07 Variable-CostingDocument17 pagesIPE48116 MainulBari S04 Ch07 Variable-CostingAhsanul haque JoyNo ratings yet

- Question 1-1-1Document14 pagesQuestion 1-1-1Aqsa AnumNo ratings yet

- ACT202 - Chapter 6Document38 pagesACT202 - Chapter 6arafkhan1623No ratings yet

- FINMAN2 GROUP2 Variable and Absorption CostingDocument88 pagesFINMAN2 GROUP2 Variable and Absorption CostingRye Diaz-SanchezNo ratings yet

- F5-CVP-1 AccaDocument10 pagesF5-CVP-1 AccaAmna HussainNo ratings yet

- Absorption Marginal CostingDocument32 pagesAbsorption Marginal Costingdunks metaNo ratings yet

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageFrom EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- Ref LetterDocument1 pageRef LetterLanre OdubanjoNo ratings yet

- ProposalDocument2 pagesProposalLanre OdubanjoNo ratings yet

- DR$ CR$: Additional InformationDocument1 pageDR$ CR$: Additional InformationLanre OdubanjoNo ratings yet

- F4MLA Section B 2015 Jun QDocument3 pagesF4MLA Section B 2015 Jun QLanre OdubanjoNo ratings yet

- Wealth-Insight - Sep 2023Document76 pagesWealth-Insight - Sep 2023Premnath YadavNo ratings yet

- Bharti Airtel in Africa: Group - 11Document15 pagesBharti Airtel in Africa: Group - 11Srijani DharaNo ratings yet

- Applied Economics - ABM12 - Final Exam - 3 Copies.Document3 pagesApplied Economics - ABM12 - Final Exam - 3 Copies.Bago ResilynNo ratings yet

- My CVDocument2 pagesMy CVNgatamariki JohanssonNo ratings yet

- Concept of Strategy, Concept of Strategic Management and TypeDocument18 pagesConcept of Strategy, Concept of Strategic Management and Typepopat vishal100% (1)

- Chapter 15 - The Marketing Mix - PromotionDocument18 pagesChapter 15 - The Marketing Mix - PromotionHassan ShahidNo ratings yet

- Invoice OD117647490612370000Document2 pagesInvoice OD117647490612370000Dass MNo ratings yet

- MOT Final Project: Keepy CementDocument28 pagesMOT Final Project: Keepy Cementmurary123No ratings yet

- International Business AssignmentDocument11 pagesInternational Business AssignmentRI ShawonNo ratings yet

- LessDocument24 pagesLessMANISHANo ratings yet

- Closing RemarksDocument3 pagesClosing Remarkskiran869100% (1)

- Finweek - December 3, 2015 PDFDocument48 pagesFinweek - December 3, 2015 PDFTulus PramujiNo ratings yet

- Job OrderDocument2 pagesJob Orderrose llarNo ratings yet

- Chapter 2 - SlidesDocument24 pagesChapter 2 - Slidesazade azamiNo ratings yet

- Study of Consumer Perception of Digital Payment ModeDocument14 pagesStudy of Consumer Perception of Digital Payment Modekarthick50% (2)

- Wife Cibil ReportDocument9 pagesWife Cibil ReportElan ThamizhNo ratings yet

- Pathao Company Industrial Dispute in Our Country: Presented byDocument13 pagesPathao Company Industrial Dispute in Our Country: Presented byPapon Sarkar 182-11-656No ratings yet

- SSRN Id2672722Document29 pagesSSRN Id2672722Hassan AdamNo ratings yet

- The Permanent Beta Principle SampleDocument22 pagesThe Permanent Beta Principle SampleMartijn AslanderNo ratings yet

- Tendernotice 1Document2 pagesTendernotice 1Ali Asghar ShahNo ratings yet

- Lavender Report FinalDocument26 pagesLavender Report FinalManiruzzamanApuNo ratings yet

- Hindenburgresearch Com AdaniDocument20 pagesHindenburgresearch Com AdaniOmkar KambleNo ratings yet

- Correspondent BankingDocument13 pagesCorrespondent BankingYash Mittal100% (1)

- PDF IprDocument10 pagesPDF IprUjjwal AnandNo ratings yet

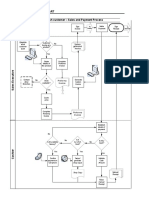

- As-Is-Flow Process Chart: No System Generated InvoiceDocument10 pagesAs-Is-Flow Process Chart: No System Generated Invoicepeter mulilaNo ratings yet

- A Comparative StudyDocument13 pagesA Comparative StudyTushar PingateNo ratings yet

- Local Media8789968818250882023Document26 pagesLocal Media8789968818250882023monica macaleNo ratings yet