You might also like

- Composition SchemeDocument2 pagesComposition SchemeMadhur MadnaniNo ratings yet

- Composition Scheme SEC 10 - GST PDFDocument20 pagesComposition Scheme SEC 10 - GST PDFTushar SinghNo ratings yet

- Provisions of GST Effective From 1St April 2019Document3 pagesProvisions of GST Effective From 1St April 2019Giri SukumarNo ratings yet

- GST Presentation 15032019Document113 pagesGST Presentation 15032019Viky AkNo ratings yet

- GST Changes 9Document3 pagesGST Changes 9Sharad ShahNo ratings yet

- Composition Scheme Sec. 10: Ques-1 What Is Composition Levy Under GST?Document12 pagesComposition Scheme Sec. 10: Ques-1 What Is Composition Levy Under GST?Tapan BarikNo ratings yet

- Goods and Service Tax 1Document30 pagesGoods and Service Tax 1DivyaNo ratings yet

- GST Composition SchemeDocument4 pagesGST Composition SchemeKushal SethiNo ratings yet

- GST Oct 17Document23 pagesGST Oct 17himanNo ratings yet

- Analysis of The GST Law: Is Your Business Prepared For The Change?Document23 pagesAnalysis of The GST Law: Is Your Business Prepared For The Change?Minecraft ServerNo ratings yet

- Goods and Service Tax (GST)Document17 pagesGoods and Service Tax (GST)Manav SethiNo ratings yet

- GST Impact On Restaurants in IndiaDocument19 pagesGST Impact On Restaurants in IndiaVarun RimmalapudiNo ratings yet

- Composition Levy: Presentation By: Vishal Somai Sr. Faculty of Direct & Indirect TaxDocument19 pagesComposition Levy: Presentation By: Vishal Somai Sr. Faculty of Direct & Indirect TaxTRANSFORMERS PRIMENo ratings yet

- Taxguru - In-Section 10 CGST Act 2017 Composition Levy Under GSTDocument5 pagesTaxguru - In-Section 10 CGST Act 2017 Composition Levy Under GSTTheEnigmatic AccountantNo ratings yet

- GST Presentation MsmeDocument114 pagesGST Presentation MsmeViky AkNo ratings yet

- GST Assign.Document23 pagesGST Assign.Saif Ali KhanNo ratings yet

- Mrunal's Economy Pillar#2A: Budget Revenue Part Tax-Receipts Page 136Document3 pagesMrunal's Economy Pillar#2A: Budget Revenue Part Tax-Receipts Page 136Washim Alam50CNo ratings yet

- Acc. PracticalDocument16 pagesAcc. PracticalSrijan BhambeeNo ratings yet

- Goods and Service Tax (GST)Document19 pagesGoods and Service Tax (GST)Saurabh Kumar SharmaNo ratings yet

- GST Basic For WebsiteDocument17 pagesGST Basic For WebsiteUdit JalanNo ratings yet

- When Is It Required For A Business Owner To Register For GST?Document4 pagesWhen Is It Required For A Business Owner To Register For GST?sai sowmiNo ratings yet

- Goods and Services Tax (GST) : Unit VDocument35 pagesGoods and Services Tax (GST) : Unit VDeborahNo ratings yet

- Composition Scheme and Registration Unit 2Document9 pagesComposition Scheme and Registration Unit 2Cupid FriendNo ratings yet

- Basic Understanding of GST in IndiaDocument13 pagesBasic Understanding of GST in IndiasrivarshiniNo ratings yet

- 04 01 1 PresentationonGSTversion4Document32 pages04 01 1 PresentationonGSTversion4Srinivas Pavan KumarNo ratings yet

- Faqs On New GST Retu Rns FormsDocument14 pagesFaqs On New GST Retu Rns FormsFizo KjNo ratings yet

- Composition SchemeDocument9 pagesComposition SchemeNeha NayakNo ratings yet

- Impacts of GST On Indian EconomyDocument14 pagesImpacts of GST On Indian EconomyR.Deepak KannaNo ratings yet

- Composition SchemeDocument10 pagesComposition SchemeAnonymous xH9VFaNUNo ratings yet

- When Is It Required For A Business Owner To Register For GST?Document3 pagesWhen Is It Required For A Business Owner To Register For GST?sai sowmiNo ratings yet

- When Is It Required For A Business Owner To Register For GST?Document3 pagesWhen Is It Required For A Business Owner To Register For GST?sai sowmiNo ratings yet

- Compostion SchemeDocument6 pagesCompostion SchemeK S RNo ratings yet

- Goods and Services Tax: By:-Ritvic PulwaniDocument10 pagesGoods and Services Tax: By:-Ritvic PulwaniNikhil VermaNo ratings yet

- Overview of GSTDocument83 pagesOverview of GSTPankaj MahantaNo ratings yet

- Compliance ManualDocument52 pagesCompliance ManualNupur GajjarNo ratings yet

- Central Taxes Replaced by GSTDocument6 pagesCentral Taxes Replaced by GSTBijosh ThomasNo ratings yet

- Ayush PendDocument62 pagesAyush PendPankaj MahantaNo ratings yet

- Presentation On GSTDocument24 pagesPresentation On GSTsajidneki365No ratings yet

- Chapter 1: Introduction To GST 1.1 Basics of GST 1.1.1 What Is GST?Document13 pagesChapter 1: Introduction To GST 1.1 Basics of GST 1.1.1 What Is GST?Ashutosh papelNo ratings yet

- 37 GST Council MeetingDocument5 pages37 GST Council MeetingChinmay BhatNo ratings yet

- Understanding Goods and Services TaxDocument23 pagesUnderstanding Goods and Services TaxGANGARAJU NALINo ratings yet

- Understanding Goods and Services TaxDocument23 pagesUnderstanding Goods and Services TaxTEst User 44452No ratings yet

- India Chartbook: GST - Getting Simplified TaxationDocument49 pagesIndia Chartbook: GST - Getting Simplified TaxationnitroglyssNo ratings yet

- GST NotesDocument39 pagesGST NotesCrick CompactNo ratings yet

- Harsh Kandele-19mbar0242-Cia2-ItDocument9 pagesHarsh Kandele-19mbar0242-Cia2-ItHarsh KandeleNo ratings yet

- Synopsis of Budget For Fy 2068-69 Prepared by G. K. Agrawal & Co.Document33 pagesSynopsis of Budget For Fy 2068-69 Prepared by G. K. Agrawal & Co.knmodiNo ratings yet

- Overview GSTDocument56 pagesOverview GSTrahulNo ratings yet

- A Study On Goods & Service TaxDocument15 pagesA Study On Goods & Service Taxgaikwadswapnil0603No ratings yet

- Lec 6 Income Tax RatesDocument4 pagesLec 6 Income Tax Ratesrehan87100% (2)

- GST On Restaurants GST Regime: Rate of Bills Type of Restaurants Tax RateDocument17 pagesGST On Restaurants GST Regime: Rate of Bills Type of Restaurants Tax RateshyamNo ratings yet

- Role of CS in GSTDocument66 pagesRole of CS in GSThareshmsNo ratings yet

- Goods and Services Tax (GST) in India: A Presentation by KRISHNA SHUKLADocument30 pagesGoods and Services Tax (GST) in India: A Presentation by KRISHNA SHUKLAKrishna ShuklaNo ratings yet

- GST - Monsoon - Elections - Fundamental AnalysisDocument9 pagesGST - Monsoon - Elections - Fundamental AnalysisJerin JoyNo ratings yet

- GST Unit 1Document52 pagesGST Unit 1SANSKRITI YADAV 22DM236No ratings yet

- Compliance Manual F.Y. 2020 21 A.Y.2021 22 PDFDocument52 pagesCompliance Manual F.Y. 2020 21 A.Y.2021 22 PDFTHERMAL TECH ENGINEERINGNo ratings yet

- CGST LawDocument30 pagesCGST LawPranit Anil ChavanNo ratings yet

- GST Composition SchemeDocument2 pagesGST Composition SchemeRohan SinhaNo ratings yet

- Understanding Goods and Services TaxDocument23 pagesUnderstanding Goods and Services TaxPragya TyagiNo ratings yet

- Goods and Services Tax (GST) Filing Made Easy: Free Software Literacy SeriesFrom EverandGoods and Services Tax (GST) Filing Made Easy: Free Software Literacy SeriesNo ratings yet

- F T I L: Sunday, June 13, 2021Document74 pagesF T I L: Sunday, June 13, 2021Asutosh PradhanNo ratings yet

- InvoiceDocument1 pageInvoiceRaj mishraNo ratings yet

- PUNE - Hotel StayDocument2 pagesPUNE - Hotel StaySantosh DeshpandeNo ratings yet

- Tendernotice 1Document122 pagesTendernotice 1Goutam MandalNo ratings yet

- PSPCL: (Pgbillpay - Aspx) (Pgbillpay - Aspx)Document2 pagesPSPCL: (Pgbillpay - Aspx) (Pgbillpay - Aspx)Rohit KumarNo ratings yet

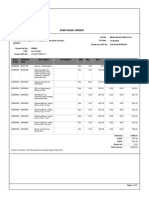

- Cloudnine PODocument2 pagesCloudnine POAnonymous lFoxYANo ratings yet

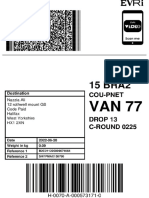

- H0070A0005731710 labelAndInvoiceMergeDocument2 pagesH0070A0005731710 labelAndInvoiceMergeAnupam SinghNo ratings yet

- Cash User Manual PDFDocument60 pagesCash User Manual PDFGaurish BorkarNo ratings yet

- Money Transfer API Service ProposalDocument6 pagesMoney Transfer API Service ProposalAnagh RajNo ratings yet

- Result of GSTDocument8 pagesResult of GSTsantosh mondalNo ratings yet

- Effect of GST On The Indian EconomyDocument4 pagesEffect of GST On The Indian EconomyShubham GargNo ratings yet

- Billing Address: Tax InvoiceDocument1 pageBilling Address: Tax InvoiceChandresh SinghNo ratings yet

- (Original For Recipient) : Sl. No Description Unit Price Discount Qty Net Amount Tax Rate Tax Type Tax Amount Total AmountDocument1 page(Original For Recipient) : Sl. No Description Unit Price Discount Qty Net Amount Tax Rate Tax Type Tax Amount Total Amountsrikanth121No ratings yet

- GCC July 2020 1Document111 pagesGCC July 2020 1krishnanandvermaNo ratings yet

- Shail Enterprises: Tax InvoiceDocument1 pageShail Enterprises: Tax InvoicenirajNo ratings yet

- GST NAV 2016 Setup For IndiaDocument93 pagesGST NAV 2016 Setup For IndiaKenneth LunaNo ratings yet

- Aarthika Charche Vol2 No1Document74 pagesAarthika Charche Vol2 No1Das JavaNo ratings yet

- Your Vi Bill: Mr. Vignesh VDocument4 pagesYour Vi Bill: Mr. Vignesh VVigneshvkeyNo ratings yet

- Fixedline and Broadband Services: Your Account Summary This Month'S ChargesDocument3 pagesFixedline and Broadband Services: Your Account Summary This Month'S ChargesSai PranayNo ratings yet

- Management Representation Letter For GST AuditDocument5 pagesManagement Representation Letter For GST AuditCA Prince GargNo ratings yet

- Term Insurance Premium Receipt: Personal DetailsDocument1 pageTerm Insurance Premium Receipt: Personal DetailsRanjith BNo ratings yet

- 127-22-23-200kva ServoDocument1 page127-22-23-200kva ServoRachna patelNo ratings yet

- Ca Final: Paper 8: Indirect Tax LawsDocument499 pagesCa Final: Paper 8: Indirect Tax LawsMaroju Rajitha100% (1)

- GST SettlementDocument32 pagesGST SettlementSrinivas KovvurNo ratings yet

- FlatskimDocument3 pagesFlatskimAbhijit C. BireNo ratings yet

- Guidance Note-Claim of ITC As Per GSTR 2B - Taxguru - inDocument4 pagesGuidance Note-Claim of ITC As Per GSTR 2B - Taxguru - inpradeepkumarsnairNo ratings yet

- 100 Judgments Under GST in 2023-Jan 24Document103 pages100 Judgments Under GST in 2023-Jan 24calmincometax36No ratings yet

- India S Import Coal and Coke Report by Iman ResourcesDocument51 pagesIndia S Import Coal and Coke Report by Iman ResourcesNageswar MakalaNo ratings yet

- Tax InvoiceDocument1 pageTax Invoicesa4314256No ratings yet

- MQC00190DDocument5 pagesMQC00190DGaneshkumar AmbedkarNo ratings yet