You might also like

- Intermediate Accounting 1: a QuickStudy Digital Reference GuideFrom EverandIntermediate Accounting 1: a QuickStudy Digital Reference GuideNo ratings yet

- Refunds: Chapter - 19Document28 pagesRefunds: Chapter - 19Ashma KhanalNo ratings yet

- Transmittal Letter: Republic of The Philippines Department of Finance Bureau of Internal RevenueDocument2 pagesTransmittal Letter: Republic of The Philippines Department of Finance Bureau of Internal RevenueLayne Kendee100% (2)

- Isolator Technology Workshop - Sterility Test Isolator: Engineering - Validation - OperationDocument4 pagesIsolator Technology Workshop - Sterility Test Isolator: Engineering - Validation - OperationRND BiotisNo ratings yet

- Procure To Pay Life CycleDocument13 pagesProcure To Pay Life Cyclerajitha nishanthNo ratings yet

- ProtestLetter TICIDocument4 pagesProtestLetter TICIdbircs100% (4)

- Mega Project Assurance: Volume One - The Terminological DictionaryFrom EverandMega Project Assurance: Volume One - The Terminological DictionaryNo ratings yet

- Bruhat Bengaluru Mahanagara Palike - Revenue Department: Xjdœ LXD - /HZ Eud/ Eĺ Lbx¡E (6 E LDocument1 pageBruhat Bengaluru Mahanagara Palike - Revenue Department: Xjdœ LXD - /HZ Eud/ Eĺ Lbx¡E (6 E LamitthemalNo ratings yet

- GST Chalisa CH 6 - Value of Supply (R)Document5 pagesGST Chalisa CH 6 - Value of Supply (R)Bharatbhusan RoutNo ratings yet

- Technical Perspective On Accounts Receivable Receipts PDFDocument15 pagesTechnical Perspective On Accounts Receivable Receipts PDFvenuvydhyalaNo ratings yet

- Accounting 11 CambridgeDocument393 pagesAccounting 11 CambridgeGokul Bhargav100% (3)

- Material - GSTDocument18 pagesMaterial - GSTDeepak NimmojiNo ratings yet

- Sap Retail BrochureDocument6 pagesSap Retail BrochureRai Ali WafaNo ratings yet

- Torts and Damages Case Digest: Philippine Bank of Commerce V. CA (1997)Document43 pagesTorts and Damages Case Digest: Philippine Bank of Commerce V. CA (1997)Nīc CādīgālNo ratings yet

- R12 Cash Management Payments and ReceiptsDocument13 pagesR12 Cash Management Payments and ReceiptsramasamysatturNo ratings yet

- GST 5.1Document46 pagesGST 5.1Raghav TiwariNo ratings yet

- All The Due Dates and Time Limits in GSTDocument10 pagesAll The Due Dates and Time Limits in GST2d77gp69kzNo ratings yet

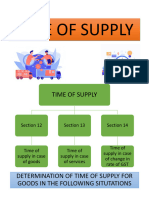

- Time of Supply-IDocument50 pagesTime of Supply-IVaibhav GawadeNo ratings yet

- Invoice InterDocument10 pagesInvoice InterKaylee WrightNo ratings yet

- Time of Supply of ServicesDocument10 pagesTime of Supply of ServicesShiwang AgrawalNo ratings yet

- GST Seminar: Hosted By:-Akola Branch of WICASA of ICAIDocument40 pagesGST Seminar: Hosted By:-Akola Branch of WICASA of ICAINavneetNo ratings yet

- Tos & Vos PDFDocument42 pagesTos & Vos PDFRatulNo ratings yet

- Time of SupplyDocument53 pagesTime of SupplySumeetNo ratings yet

- Chapter 6 - Time of SupplyDocument7 pagesChapter 6 - Time of SupplyDrafts StorageNo ratings yet

- GST PPT (Group 5)Document20 pagesGST PPT (Group 5)Hanna GeorgeNo ratings yet

- GST Notes Unit IIDocument18 pagesGST Notes Unit IImoyopatron4No ratings yet

- 4 GST Time and Value of Supply NotesDocument6 pages4 GST Time and Value of Supply NotesMurali Krishnan RNo ratings yet

- CH 6 Time of Supply PDFDocument48 pagesCH 6 Time of Supply PDFManas Kumar SahooNo ratings yet

- Idt 2Document10 pagesIdt 2manan agrawalNo ratings yet

- GST - Tax Invoice, Debit or Credit Notes, Returns, Payment of Tax PDFDocument78 pagesGST - Tax Invoice, Debit or Credit Notes, Returns, Payment of Tax PDFSapna MalikNo ratings yet

- 5 Time of SupplyDocument18 pages5 Time of SupplyDhana SekarNo ratings yet

- QBT Container Packing Agreement MasterDocument31 pagesQBT Container Packing Agreement MasterqldbulkterminalsNo ratings yet

- Time of SupplyDocument4 pagesTime of SupplyAarushi GuptaNo ratings yet

- UNIT 2 (4) Time of SupplyDocument15 pagesUNIT 2 (4) Time of SupplySania KhanNo ratings yet

- Levy in GST S.No Particulars 1 Time of SupplyDocument7 pagesLevy in GST S.No Particulars 1 Time of SupplyAnonymous ikQZphNo ratings yet

- Time of SupplyDocument28 pagesTime of SupplySam RockerNo ratings yet

- Composit & Mixed SupplyDocument30 pagesComposit & Mixed Supplypajemakiii9No ratings yet

- GST - Time of Supply of Goods (Summary)Document1 pageGST - Time of Supply of Goods (Summary)Saksham KathuriaNo ratings yet

- 46787bosfinal p8 Part1 Cp10Document47 pages46787bosfinal p8 Part1 Cp10virmani123No ratings yet

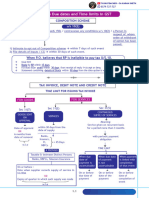

- Tax Invoice & E-Way BillDocument33 pagesTax Invoice & E-Way BillDayal SinghNo ratings yet

- Invoicing Under Goods and Service TAXDocument37 pagesInvoicing Under Goods and Service TAXAmit GuptaNo ratings yet

- E Flier Credit Notes in GSTDocument2 pagesE Flier Credit Notes in GSTSneha AgarwalNo ratings yet

- 74811bos60500 cp2Document102 pages74811bos60500 cp2Kapil KumarNo ratings yet

- Refund ChartDocument1 pageRefund ChartManiGandan CNo ratings yet

- GST For Nov 2022 & May 2023 Exams (GST Time of Supply of ServicesDocument1 pageGST For Nov 2022 & May 2023 Exams (GST Time of Supply of ServicesVikasNo ratings yet

- Time of Supply: General Time Limit For Raising InvoicesDocument4 pagesTime of Supply: General Time Limit For Raising InvoicesPrasanthNo ratings yet

- Supply Under GSTDocument14 pagesSupply Under GSTTreesa Mary RejiNo ratings yet

- @csupdates ATLP REVISION NotesDocument35 pages@csupdates ATLP REVISION NotesSyed BukhariNo ratings yet

- GST - V2 - May 2023Document326 pagesGST - V2 - May 2023FhfhhNo ratings yet

- Tax, GST, Transfer PricingDocument11 pagesTax, GST, Transfer Pricingbiplav2uNo ratings yet

- Indirect Tax and GST - Unit IIIDocument43 pagesIndirect Tax and GST - Unit IIIPRATIK JAINNo ratings yet

- Sop BrochureDocument6 pagesSop BrochurePhonemyat MoeNo ratings yet

- Unit II - Part IV - Revised - Time and Value of Supply 04-08-2021Document9 pagesUnit II - Part IV - Revised - Time and Value of Supply 04-08-2021Milan ChandaranaNo ratings yet

- Chapter 7 - Value of Supply - NotesDocument16 pagesChapter 7 - Value of Supply - NotesPuran GuptaNo ratings yet

- Value of SupplyDocument12 pagesValue of SupplyDrishti100% (1)

- Time of Supply: CMA Bhogavalli Mallikarjuna GuptaDocument5 pagesTime of Supply: CMA Bhogavalli Mallikarjuna Guptagurusha bhallaNo ratings yet

- S. 16: Eligibility & Conditions: Receipt of Document Forward Charge Cases (FCM)Document3 pagesS. 16: Eligibility & Conditions: Receipt of Document Forward Charge Cases (FCM)MANU SHANKARNo ratings yet

- MP 040909-SD-EngDocument7 pagesMP 040909-SD-EngDeepak TiggaNo ratings yet

- Time of Supply INTERDocument20 pagesTime of Supply INTERKaylee WrightNo ratings yet

- 4 Time of SupplyDocument43 pages4 Time of SupplynashwauefaNo ratings yet

- GST1Document25 pagesGST1DeepikaNo ratings yet

- Time and Value of Supply-4Document73 pagesTime and Value of Supply-4Muhammad MehrajNo ratings yet

- Supply Under GST GSTDocument76 pagesSupply Under GST GSTViral OkNo ratings yet

- Meaning and Scope of Supply Under GSTDocument5 pagesMeaning and Scope of Supply Under GSTRohit BajpaiNo ratings yet

- Invoicing Under Goods and Service TAXDocument21 pagesInvoicing Under Goods and Service TAXMichealNo ratings yet

- Time of Supply PDFDocument16 pagesTime of Supply PDFNaveed AnsariNo ratings yet

- Reverse Charge MechanismDocument3 pagesReverse Charge MechanismjaipalmeNo ratings yet

- Value of Supply: Learning OutcomesDocument85 pagesValue of Supply: Learning OutcomesAdventure TimeNo ratings yet

- Supply Under GST: GlimpsesDocument19 pagesSupply Under GST: GlimpsesAdventure TimeNo ratings yet

- IDT FullDocument72 pagesIDT Fullpandeyaman7608No ratings yet

- Idt 5Document5 pagesIdt 5manan agrawalNo ratings yet

- Idt 4Document10 pagesIdt 4manan agrawalNo ratings yet

- Idt 2Document10 pagesIdt 2manan agrawalNo ratings yet

- Idt 1Document10 pagesIdt 1manan agrawalNo ratings yet

- CashDocument11 pagesCashCharles Andrew De VeraNo ratings yet

- Uni-5 User Manual1Document298 pagesUni-5 User Manual1Ian WashishNo ratings yet

- Camilla Stryker 721 ManualDocument20 pagesCamilla Stryker 721 Manualbiomedico internationalNo ratings yet

- Safe Deposit Box Account Rental Agreement Rules and RegulationsDocument6 pagesSafe Deposit Box Account Rental Agreement Rules and RegulationsJohn29999No ratings yet

- Transmittal 2Document7 pagesTransmittal 2King Aces OperationsNo ratings yet

- Vouchers Holiday Homework 2Document4 pagesVouchers Holiday Homework 2khushiNo ratings yet

- FB60 - F-43 - Duplicate Invoice CheckDocument4 pagesFB60 - F-43 - Duplicate Invoice CheckdaulathNo ratings yet

- General Ledger PDFDocument33 pagesGeneral Ledger PDFSahitee BasaniNo ratings yet

- ReceiptDocument1 pageReceiptReem ShehabNo ratings yet

- Analysis of Income Tax in AfghanistanDocument47 pagesAnalysis of Income Tax in Afghanistanmasoud_dostNo ratings yet

- Value Added Tax (VAT)Document37 pagesValue Added Tax (VAT)Minh Hương TrầnNo ratings yet

- Business Bureau - Business PermitDocument42 pagesBusiness Bureau - Business PermitJessielleNo ratings yet

- STC Vat Test Bank 1Document29 pagesSTC Vat Test Bank 1alden123No ratings yet

- Medicash Claim FormDocument6 pagesMedicash Claim Formwaran RMNo ratings yet

- (To Be Published in The Gazette of India, Extraordinary, Part Ii, Section 3, Sub-Section (I) )Document47 pages(To Be Published in The Gazette of India, Extraordinary, Part Ii, Section 3, Sub-Section (I) )HimanshuKaushikNo ratings yet

- Arn Receipt GST Rfd-01a 10ctupk3011q1zh ExbclDocument1 pageArn Receipt GST Rfd-01a 10ctupk3011q1zh ExbclRAHUL AGGARWALNo ratings yet

- 7 TDP Excise DutyDocument41 pages7 TDP Excise DutyPranav TubajiNo ratings yet

- 64 Aba 2 AbDocument5 pages64 Aba 2 Abgi estevesNo ratings yet

- NTC ObsevationsDocument3 pagesNTC ObsevationsMuzaffar UddinNo ratings yet

- AE 101 Module 3 Lessons 1 2Document23 pagesAE 101 Module 3 Lessons 1 2Arly Kurt TorresNo ratings yet