You might also like

- ILIT Power Point October 2010Document8 pagesILIT Power Point October 2010Christopher GuestNo ratings yet

- Aras Jung Curriculum IndividualDocument72 pagesAras Jung Curriculum IndividualdianavaleriaalvarezNo ratings yet

- TCM FD20-25Document579 pagesTCM FD20-25Socma Reachstackers100% (2)

- Glazing Risk AssessmentDocument6 pagesGlazing Risk AssessmentKaren OlivierNo ratings yet

- SBI Reverse Mortgage LoanDocument5 pagesSBI Reverse Mortgage LoanVishwa Prasanna Kumar100% (1)

- Should Municipal Bonds be a Tool in Your Retirement Planning Toolbox?From EverandShould Municipal Bonds be a Tool in Your Retirement Planning Toolbox?No ratings yet

- Income From House PropertyDocument27 pagesIncome From House Propertyanon-713603100% (4)

- Phe Manual 1000e GB tcm11-7539Document36 pagesPhe Manual 1000e GB tcm11-7539iwan kurniawanNo ratings yet

- A Haven on Earth: Singapore Economy Without Duties and TaxesFrom EverandA Haven on Earth: Singapore Economy Without Duties and TaxesNo ratings yet

- P Remission of ABSD (TRUST) 22052023Document4 pagesP Remission of ABSD (TRUST) 22052023charmeyan1scribdNo ratings yet

- TDSR & MAS 632 (External) - 131210-2Document15 pagesTDSR & MAS 632 (External) - 131210-2hi2joeyNo ratings yet

- cLUBBING OF iNCOMEDocument18 pagescLUBBING OF iNCOMEDipinderNo ratings yet

- RBI Bonds Product NoteDocument2 pagesRBI Bonds Product NoteYash SoniNo ratings yet

- Reverse Mortgage BY Public Sector BanksDocument26 pagesReverse Mortgage BY Public Sector BanksJuliet PetersNo ratings yet

- Case Study On Housing Loan For Banking StudentsDocument4 pagesCase Study On Housing Loan For Banking StudentsMuralidharprasad Ayaluru75% (4)

- Government BusinessDocument17 pagesGovernment BusinessManish AroraNo ratings yet

- Life Insurance Corporation of India PDFDocument6 pagesLife Insurance Corporation of India PDFAxe ExaNo ratings yet

- Housing Finance IndustryDocument18 pagesHousing Finance IndustrySiva annaNo ratings yet

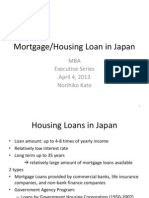

- Mortgage Loans in JapanDocument16 pagesMortgage Loans in JapanBayarmagnay BaasansurenNo ratings yet

- BT ON EMI TNCDocument3 pagesBT ON EMI TNCRahul BaraiyaNo ratings yet

- Cent Grih Lakshmi Home LoanDocument1 pageCent Grih Lakshmi Home Loanakbar khanNo ratings yet

- Sbi Home Loan InfoDocument4 pagesSbi Home Loan InfoBhargavaSharmaNo ratings yet

- Home Loan MitcDocument4 pagesHome Loan Mitcdrgayen6042No ratings yet

- Flexipay - Terms & ConditionsDocument3 pagesFlexipay - Terms & ConditionsKaranveer SinghNo ratings yet

- 158 Jaimin Arun Vasani TyBaf Indirect Tax AssigmentDocument17 pages158 Jaimin Arun Vasani TyBaf Indirect Tax AssigmentJaimin VasaniNo ratings yet

- Terms and ConditionsDocument4 pagesTerms and ConditionsThatukuru LakshmanNo ratings yet

- Flexipay TNCDocument5 pagesFlexipay TNCvenkateshvaddipogu11No ratings yet

- Pagibig UpdatesDocument5 pagesPagibig UpdatesKeiah CailaoNo ratings yet

- GSIS BenefitsDocument17 pagesGSIS BenefitsRandy MusaNo ratings yet

- Sbi Home Loan MitcDocument4 pagesSbi Home Loan MitcfeeldboyNo ratings yet

- Additional Buyer Stamp Duty-Fact-SheetDocument3 pagesAdditional Buyer Stamp Duty-Fact-SheetyusehaiNo ratings yet

- Employees Housing Loan-667-666 NF-546 NF-523 NF-482 NF-461 NF-462 NF-967 NF-803 NF-760Document6 pagesEmployees Housing Loan-667-666 NF-546 NF-523 NF-482 NF-461 NF-462 NF-967 NF-803 NF-760Santosh KumarNo ratings yet

- The "Best Practices" When Using Fore! Trust Software After Enactment of The Secure ActDocument6 pagesThe "Best Practices" When Using Fore! Trust Software After Enactment of The Secure ActENo ratings yet

- Modified Guidelines On The Pag-IBIG Fund Affordable Housing ProgramDocument10 pagesModified Guidelines On The Pag-IBIG Fund Affordable Housing ProgramnadinemuchNo ratings yet

- Reverse Mortgage: A Tool For Old Age Pensions: Presented By:VINAY HANSDocument17 pagesReverse Mortgage: A Tool For Old Age Pensions: Presented By:VINAY HANSanurag_santNo ratings yet

- Product Brief - Home LoanDocument3 pagesProduct Brief - Home LoanxingnanNo ratings yet

- These Faqs Are Subject To Changes From Time To TimeDocument6 pagesThese Faqs Are Subject To Changes From Time To TimeEntomic ChemicalsNo ratings yet

- Credit Risk Guarantee Fund Scheme For Low Income HousingDocument20 pagesCredit Risk Guarantee Fund Scheme For Low Income HousingRaja SundaramNo ratings yet

- Century Royale Brochure Ver 05 (1) - 11-11Document1 pageCentury Royale Brochure Ver 05 (1) - 11-11arunsm1611No ratings yet

- Opening of Term DepositDocument8 pagesOpening of Term DepositDeepak RoyNo ratings yet

- Reverse MortgageDocument12 pagesReverse MortgageAryan KumarNo ratings yet

- Underwriting of Shares and Debentures.Document26 pagesUnderwriting of Shares and Debentures.DeathRayShot -No ratings yet

- Sbi Life - Pradhan Mantri Jeevan Jyoti Bima Yojana (Uin: 111G102V01)Document1 pageSbi Life - Pradhan Mantri Jeevan Jyoti Bima Yojana (Uin: 111G102V01)Doel MajumderNo ratings yet

- Income From House Property: Prepared By: Vaishali NaroliaDocument15 pagesIncome From House Property: Prepared By: Vaishali NaroliaROYNo ratings yet

- Topic 5b-Interest IncomeDocument21 pagesTopic 5b-Interest IncomeAgnesNo ratings yet

- Akshay NidhiDocument5 pagesAkshay NidhiGuru RamanathanNo ratings yet

- Housing Loan March 2014Document2 pagesHousing Loan March 2014Deborah JenningsNo ratings yet

- Saral Pension Brochure For ReferenceDocument12 pagesSaral Pension Brochure For ReferenceKarthikeyan SakthivelNo ratings yet

- Theoretical Framework of Home LoanDocument8 pagesTheoretical Framework of Home LoanTulika GuhaNo ratings yet

- Solutions To Chapter 13 Problems 1Document3 pagesSolutions To Chapter 13 Problems 1Hira ParachaNo ratings yet

- Benefits:: (A Non-Linked, Participating, Limited Premium, Individual, Life Assurance Savings Plan)Document11 pagesBenefits:: (A Non-Linked, Participating, Limited Premium, Individual, Life Assurance Savings Plan)coolestkasinovaNo ratings yet

- Clss Affidavit PDF NewDocument2 pagesClss Affidavit PDF NewBalabasker Padmanabhan63% (8)

- Revised Note On MWP ActDocument6 pagesRevised Note On MWP ActChess LordNo ratings yet

- Income From House PropertyDocument26 pagesIncome From House PropertysnehalgaikwadNo ratings yet

- City Sky Co: Laws Related To The CaseDocument12 pagesCity Sky Co: Laws Related To The Casesv03No ratings yet

- Income TaxDocument12 pagesIncome TaxArvind RioNo ratings yet

- Clubbing ChapterDocument4 pagesClubbing ChapterManohar LalNo ratings yet

- Sbi Personal Finance MitcDocument2 pagesSbi Personal Finance MitcHumaid ShaikhNo ratings yet

- Marketing of Financial Services AsignmentDocument11 pagesMarketing of Financial Services AsignmentMohit KumarNo ratings yet

- Vested & Contingent InterestDocument4 pagesVested & Contingent InterestIngénieur Électrique100% (1)

- Chapter 5 Income of Other Persons Included in Assessee S Total IncomeDocument8 pagesChapter 5 Income of Other Persons Included in Assessee S Total IncomeRaj Pati SundiNo ratings yet

- XYZHL Application Form - Editable - FinalDocument5 pagesXYZHL Application Form - Editable - FinalamiteshnegiNo ratings yet

- Stages of Life in A Human BeingDocument18 pagesStages of Life in A Human BeingNicholas LimNo ratings yet

- JSJ Sels ChartDocument1 pageJSJ Sels ChartNicholas LimNo ratings yet

- (Undefined Series For Scimag) - Libgen - LiDocument7 pages(Undefined Series For Scimag) - Libgen - LiNicholas LimNo ratings yet

- 3 Day Diet RecordDocument4 pages3 Day Diet RecordNicholas LimNo ratings yet

- 6S Quality Process (Pharmanex & Nu Skin) SG160113Document1 page6S Quality Process (Pharmanex & Nu Skin) SG160113Nicholas LimNo ratings yet

- Deep Dry Needling of The Shoulder Muscles: Carel Bron Jo L.M. Franssen Betty T.M. BeersmaDocument13 pagesDeep Dry Needling of The Shoulder Muscles: Carel Bron Jo L.M. Franssen Betty T.M. BeersmaNicholas LimNo ratings yet

- Nutrition Exam 1: FortifiedDocument8 pagesNutrition Exam 1: FortifiedNicholas LimNo ratings yet

- Truchiro Tribe Handout Coronavirus 1Document1 pageTruchiro Tribe Handout Coronavirus 1Nicholas LimNo ratings yet

- Syncronex Single Copy 3.1 Users GuideDocument208 pagesSyncronex Single Copy 3.1 Users GuideTony BoscoNo ratings yet

- DSNHP00197140000690828 2022Document2 pagesDSNHP00197140000690828 2022Vidya SagarNo ratings yet

- Ooip Volume MbeDocument19 pagesOoip Volume Mbefoxnew11No ratings yet

- tgs2600 Product Information Rev02 PDFDocument2 pagestgs2600 Product Information Rev02 PDFAbhishek SinghNo ratings yet

- Weforma WBZ ENDocument18 pagesWeforma WBZ ENRuben PauwelsNo ratings yet

- Software Lab Assignment 2Document4 pagesSoftware Lab Assignment 2atatsalamaNo ratings yet

- Honeywell S4565 CVI Ignition ControlDocument66 pagesHoneywell S4565 CVI Ignition ControlcarlosNo ratings yet

- GRFU Description: Huawei Technologies Co., LTDDocument9 pagesGRFU Description: Huawei Technologies Co., LTDJamal HagiNo ratings yet

- CAE Listening Practice Test 13 Printable - EngExam - InfoDocument2 pagesCAE Listening Practice Test 13 Printable - EngExam - InfoCarolina MartinezNo ratings yet

- Suzanne Cardenas Uesj Thesis 2020Document92 pagesSuzanne Cardenas Uesj Thesis 2020api-262960549No ratings yet

- Pugh ChartDocument1 pagePugh Chartapi-92134725No ratings yet

- Literature & MedicineDocument14 pagesLiterature & MedicineJoyce LeungNo ratings yet

- 1570-Article Text-4693-1-10-20190709Document18 pages1570-Article Text-4693-1-10-20190709Innocent PhiriNo ratings yet

- Diode Equivalent ModelsDocument9 pagesDiode Equivalent ModelsJay Ey0% (1)

- Web Development Internship TaskDocument12 pagesWeb Development Internship TaskradhaNo ratings yet

- 15 TribonDocument10 pages15 Tribonlequanghung98No ratings yet

- A Catalogue of SturmDocument10 pagesA Catalogue of SturmNellis BlancoNo ratings yet

- Pemco OperationsDocument76 pagesPemco OperationsRodrigo PereiraNo ratings yet

- Topic 1: Introduction To Telecommunication: SPM1012: Telecommunication and NetworkingDocument22 pagesTopic 1: Introduction To Telecommunication: SPM1012: Telecommunication and Networkingkhalfan athmanNo ratings yet

- 7th NisssDocument9 pages7th NisssVedang PandeyNo ratings yet

- Omni Bas Outdoor Product CatalogDocument70 pagesOmni Bas Outdoor Product CatalogVladislav GordeevNo ratings yet

- Weekly Science Report 29th July 2022Document12 pagesWeekly Science Report 29th July 2022John SmithNo ratings yet

- Goal SeekDocument7 pagesGoal SeekdNo ratings yet

- lmp91000 PDFDocument31 pageslmp91000 PDFJoão CostaNo ratings yet

- ECE - 1551 Digital Logic Lecture 15: Combinational Circuits: Assistant Prof. Fareena SaqibDocument19 pagesECE - 1551 Digital Logic Lecture 15: Combinational Circuits: Assistant Prof. Fareena SaqibAll aboutNo ratings yet

- Lambda Calculus CLCDocument38 pagesLambda Calculus CLCDan Mark Pidor BagsicanNo ratings yet