You might also like

- Prelim ReviewDocument41 pagesPrelim ReviewKrisan Rivera100% (1)

- 6870 - FAR First PreboardDocument14 pages6870 - FAR First PreboardZiee00No ratings yet

- Cannon Ball Review With Exercises PART 1Document11 pagesCannon Ball Review With Exercises PART 1Genelyn Langote100% (1)

- Use The Following Information For The Next Two (2) QuestionsDocument37 pagesUse The Following Information For The Next Two (2) QuestionsAbdulmajed Unda Mimbantas50% (4)

- Review Notes On Securities Regulation Code A. State Policy, PurposeDocument9 pagesReview Notes On Securities Regulation Code A. State Policy, PurposeReagan Sabate Peñaflor JD100% (1)

- Quiz 1 INTACCDocument13 pagesQuiz 1 INTACCGellie BuenaventuraNo ratings yet

- Special Report: Freedom MultiplierDocument59 pagesSpecial Report: Freedom MultiplierDeniz Cirpan100% (1)

- Atlas Copco Xas 90 Parts ManualDocument2 pagesAtlas Copco Xas 90 Parts ManualJose Carmona33% (9)

- P08. Cash & Accrual BasisDocument3 pagesP08. Cash & Accrual Basisayushiridara kwonNo ratings yet

- Cpa Review School of The Philippines ManilaDocument14 pagesCpa Review School of The Philippines ManilaVanessa Anne Acuña DavisNo ratings yet

- Financial StatementsDocument6 pagesFinancial StatementsLuiNo ratings yet

- Accounts Receivable and Receivable FinancingDocument4 pagesAccounts Receivable and Receivable FinancingLui50% (2)

- Chapter 2Document20 pagesChapter 2Coursehero PremiumNo ratings yet

- Receivables ProblemsDocument5 pagesReceivables ProblemsAbbygailNo ratings yet

- FAR PreBoard (1) CPAR BATCH90Document18 pagesFAR PreBoard (1) CPAR BATCH90Bella ChoiNo ratings yet

- Valix Book Chapt 1 5 Probs PDFDocument34 pagesValix Book Chapt 1 5 Probs PDFRengeline LucasNo ratings yet

- Problem 1 - 1 (IAA) : RequiredDocument11 pagesProblem 1 - 1 (IAA) : RequiredMareah Evanne Bahan50% (2)

- BAICC2X-Solution Supplementary - Week 1docxDocument7 pagesBAICC2X-Solution Supplementary - Week 1docxMitchie FaustinoNo ratings yet

- FAR 03-19 Loans and Receivables DiscussionDocument20 pagesFAR 03-19 Loans and Receivables DiscussionHana Grace MamangunNo ratings yet

- Financial Accounting and Reporting Problems Freebie PDFDocument46 pagesFinancial Accounting and Reporting Problems Freebie PDFC/PVT DAET, SHAINA JOYNo ratings yet

- 6727 Statement of Financial PositionDocument3 pages6727 Statement of Financial PositionJane ValenciaNo ratings yet

- Far (Q)Document14 pagesFar (Q)Jee Pare100% (1)

- China Banking V CADocument3 pagesChina Banking V CARaymart SalamidaNo ratings yet

- Cpa Review School of The Philippines ManilaDocument3 pagesCpa Review School of The Philippines ManilaAljur SalamedaNo ratings yet

- FAR - Final Preboard CPAR 92Document14 pagesFAR - Final Preboard CPAR 92joyhhazelNo ratings yet

- Statement of Financial PositionDocument3 pagesStatement of Financial Positionlyka0% (1)

- Human Resource Management Practices in Bangladesh: A Review Paper On Selective HRM FunctionsDocument8 pagesHuman Resource Management Practices in Bangladesh: A Review Paper On Selective HRM FunctionsSuhas ChowdhuryNo ratings yet

- P1 QuestionsDocument31 pagesP1 QuestionsWillen Christia M. MadulidNo ratings yet

- 6883 - Statement of Financial PositionDocument2 pages6883 - Statement of Financial PositionMaximusNo ratings yet

- Cpa Review School of The Philippines ManilaDocument2 pagesCpa Review School of The Philippines ManilaKyrie Gwynette OlarveNo ratings yet

- Cpa Review School of The Philippines ManilaDocument2 pagesCpa Review School of The Philippines ManilaJoyce Anne DugayNo ratings yet

- 7017 - Preweek Lecture FAR ProblemsDocument8 pages7017 - Preweek Lecture FAR ProblemsJohn Paul ArrozaNo ratings yet

- Review - SFP To Interim ReportingDocument3 pagesReview - SFP To Interim ReportingAna Marie IllutNo ratings yet

- Chapter 2 Problems - IADocument8 pagesChapter 2 Problems - IAKimochi SenpaiiNo ratings yet

- ACCTG 102 (Cash and Cash Equivalent)Document4 pagesACCTG 102 (Cash and Cash Equivalent)Yoonah KimNo ratings yet

- Cpa Review School of The Philipines Manila Financial Accounting and Reporting JULY 2021 First Preboard Examination SITUATION 1 - Three Unrelated EntitiesDocument15 pagesCpa Review School of The Philipines Manila Financial Accounting and Reporting JULY 2021 First Preboard Examination SITUATION 1 - Three Unrelated EntitiesSophia PerezNo ratings yet

- FAR B92 1st PB PDFDocument14 pagesFAR B92 1st PB PDFomer 2 gerdNo ratings yet

- 7078 - Single Entry and Error CorrectionDocument2 pages7078 - Single Entry and Error CorrectionaceNo ratings yet

- Ap 9002-2 LiabilitiesDocument6 pagesAp 9002-2 LiabilitiesSirNo ratings yet

- Cpa Review School of The Philippines ManilaDocument2 pagesCpa Review School of The Philippines ManilaRaquel Villar DayaoNo ratings yet

- Receivables QuizDocument2 pagesReceivables Quizhoneyjoy salapantanNo ratings yet

- Cash and Cash EquivalentsDocument3 pagesCash and Cash EquivalentsJessica JamonNo ratings yet

- 6809 Accounts ReceivableDocument2 pages6809 Accounts ReceivableEsse Valdez0% (1)

- Cash and Cash Equivalents Problem SetDocument3 pagesCash and Cash Equivalents Problem Setmarinel pioquidNo ratings yet

- Cash and Cash Equivalents Quizzer 1Document5 pagesCash and Cash Equivalents Quizzer 1yna kyleneNo ratings yet

- Quiz ZDocument5 pagesQuiz ZShannen CalimagNo ratings yet

- Statement of Financial PositionDocument3 pagesStatement of Financial PositionDJ NicartNo ratings yet

- Mock QE Questionnaire - Second Year Answer KeyDocument30 pagesMock QE Questionnaire - Second Year Answer KeyBrian Daniel BayotNo ratings yet

- 7160 - FAR Preweek ProblemDocument14 pages7160 - FAR Preweek ProblemMAS CPAR 93No ratings yet

- This Study Resource Was: (Stale Check)Document2 pagesThis Study Resource Was: (Stale Check)Lyca Mae CubangbangNo ratings yet

- Cash and Cash EquivalentsDocument8 pagesCash and Cash EquivalentsNMCartNo ratings yet

- Far PreweekDocument18 pagesFar PreweekHarvey OchoaNo ratings yet

- Test 2 FarDocument3 pagesTest 2 FarMa Jodelyn RosinNo ratings yet

- FM Quiz Set ADocument3 pagesFM Quiz Set AShaira Mae TomasNo ratings yet

- (Cpar2016) Far-6183 (Statement of Financial Position and Comprehensive Income)Document2 pages(Cpar2016) Far-6183 (Statement of Financial Position and Comprehensive Income)Irene ArantxaNo ratings yet

- Acctg 102 Prelim Exam With SolutionsDocument12 pagesAcctg 102 Prelim Exam With SolutionsYsabel ApostolNo ratings yet

- ACC203 - AssignmentDocument2 pagesACC203 - AssignmentHailsey WinterNo ratings yet

- Anskey 1-1Document8 pagesAnskey 1-1De MarcusNo ratings yet

- Bsa1acash and Cash Equivalents For Discussion PurposesDocument12 pagesBsa1acash and Cash Equivalents For Discussion PurposesSafe PlaceNo ratings yet

- ACCTG 16 FAR W2 Problems PDFDocument5 pagesACCTG 16 FAR W2 Problems PDFLabLab ChattoNo ratings yet

- Composition of Cash Petty CashDocument7 pagesComposition of Cash Petty CashRyou ShinodaNo ratings yet

- 1.3.2 Practice ProblemsDocument5 pages1.3.2 Practice ProblemsBea FalnicanNo ratings yet

- Financial Acctg & Reporting 1 - CASE ANALYSIS SUMMARYDocument23 pagesFinancial Acctg & Reporting 1 - CASE ANALYSIS SUMMARYJaquelyn ClataNo ratings yet

- One Year of Living with COVID-19: An Assessment of How ADB Members Fought the Pandemic in 2020From EverandOne Year of Living with COVID-19: An Assessment of How ADB Members Fought the Pandemic in 2020No ratings yet

- Joan Salgado Aud-Prob AssignmentDocument8 pagesJoan Salgado Aud-Prob AssignmentEsse ValdezNo ratings yet

- Valdez Blessed Nizelle - Midterm Assignemnt - Aud ProbDocument9 pagesValdez Blessed Nizelle - Midterm Assignemnt - Aud ProbEsse ValdezNo ratings yet

- Nicolas April Gwyneth S Midterm Assisgnemt Auditing ProblemsDocument8 pagesNicolas April Gwyneth S Midterm Assisgnemt Auditing ProblemsEsse ValdezNo ratings yet

- Clemente Ronaliza Auditing ProblemsDocument9 pagesClemente Ronaliza Auditing ProblemsEsse ValdezNo ratings yet

- Assignment Auditing Problemmichelle PagulayanDocument7 pagesAssignment Auditing Problemmichelle PagulayanEsse ValdezNo ratings yet

- Name: Shenielyn B. Napolitano BSA 3A Source: Roque Book: QuestionsDocument7 pagesName: Shenielyn B. Napolitano BSA 3A Source: Roque Book: QuestionsEsse ValdezNo ratings yet

- Auditing Problem Assignment Lyeca JoieDocument12 pagesAuditing Problem Assignment Lyeca JoieEsse ValdezNo ratings yet

- Problem 1: InvestmentsDocument7 pagesProblem 1: InvestmentsEsse ValdezNo ratings yet

- Christine Joy Abad AssignmentDocument8 pagesChristine Joy Abad AssignmentEsse ValdezNo ratings yet

- Cpa Review School of The Philippines ManilaDocument2 pagesCpa Review School of The Philippines ManilaEsse ValdezNo ratings yet

- 6806 Operating Segment and Interim ReportingDocument2 pages6806 Operating Segment and Interim ReportingEsse ValdezNo ratings yet

- 6809 Accounts ReceivableDocument2 pages6809 Accounts ReceivableEsse Valdez0% (1)

- 6811 Notes Receivable and Loan ImpairmentDocument2 pages6811 Notes Receivable and Loan ImpairmentEsse ValdezNo ratings yet

- Cpa Review School of The Philippines ManilaDocument2 pagesCpa Review School of The Philippines ManilaEsse ValdezNo ratings yet

- Micro Matic Student ManualDocument86 pagesMicro Matic Student ManualrtkobyNo ratings yet

- Imtiaz Ahmed: House No.B-1485 B.Ali .Shah Sukkur Contacts # 0334-4242180 0333-2434626Document3 pagesImtiaz Ahmed: House No.B-1485 B.Ali .Shah Sukkur Contacts # 0334-4242180 0333-2434626Muhammad ZeeshanNo ratings yet

- NDT Project PCVDocument9 pagesNDT Project PCVRizwan KhalidNo ratings yet

- After Effect of Corona Virus in Garments Industry PDFDocument9 pagesAfter Effect of Corona Virus in Garments Industry PDF360 degree TextileNo ratings yet

- Chapter 1 (Introduction)Document26 pagesChapter 1 (Introduction)Kshitij Shingade100% (1)

- 10.2 Function Algebra Practice PDFDocument5 pages10.2 Function Algebra Practice PDFlex zeusNo ratings yet

- Topic 3Document28 pagesTopic 3Learner's LicenseNo ratings yet

- Ang Bansang Walang Panitikan Ay Isang Bansang Walang Buhay.Document2 pagesAng Bansang Walang Panitikan Ay Isang Bansang Walang Buhay.mEOW SNo ratings yet

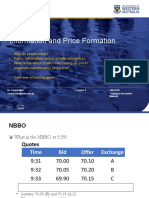

- Information and Price FormationDocument36 pagesInformation and Price FormationDylan AdrianNo ratings yet

- Political Virtue and Economic Leadership - Lee Kuan Yew and Ferdinand Marcos ComparedDocument20 pagesPolitical Virtue and Economic Leadership - Lee Kuan Yew and Ferdinand Marcos ComparedRheyNo ratings yet

- Service Agreement For Annual Physical ExamDocument9 pagesService Agreement For Annual Physical ExamJher BerNo ratings yet

- Articles of Incorporation and By-Laws - Microfinance NgoDocument14 pagesArticles of Incorporation and By-Laws - Microfinance NgomelvinNo ratings yet

- Analisis Keberlanjutan Aksesibilitas Angkutan Umum Di Kota SukabumiDocument19 pagesAnalisis Keberlanjutan Aksesibilitas Angkutan Umum Di Kota Sukabumisahidan thoybahNo ratings yet

- Coa Circular 2009-002Document21 pagesCoa Circular 2009-002Krizzel SandovalNo ratings yet

- 1-4 LectureDocument146 pages1-4 LectureAmal MobarakiNo ratings yet

- Chapter 1 BusinessTradeAndCommerceDocument21 pagesChapter 1 BusinessTradeAndCommerceAnuj Kumar SinghNo ratings yet

- SBI Genral Claim Form & Check List (1) SssDocument6 pagesSBI Genral Claim Form & Check List (1) Ssspshantanu123No ratings yet

- Essay On Mother Teresa For KidsDocument4 pagesEssay On Mother Teresa For KidsafhbgdmbtNo ratings yet

- SBI Ad FinalDocument1 pageSBI Ad Finalsrirammadhira88No ratings yet

- Transaction Cycles and Accounting ApplicationsDocument35 pagesTransaction Cycles and Accounting ApplicationsSelamawit Taddesse100% (1)

- Module 6Document34 pagesModule 6Brian Daniel BayotNo ratings yet

- IGCSE BusinessDocument4 pagesIGCSE Businesstimes tongNo ratings yet

- IC Business Budget 10897Document3 pagesIC Business Budget 10897Tougou JLSNo ratings yet

- SR Arapan Janice D.Document1 pageSR Arapan Janice D.Janice ArapanNo ratings yet

- JD For Marketing Manager - ICICI BankDocument1 pageJD For Marketing Manager - ICICI BankPrachi AroraNo ratings yet