You might also like

- The Latte FactorDocument10 pagesThe Latte FactorКыр Сосичка100% (1)

- Law of Diminishing Marginal Returns PDFDocument3 pagesLaw of Diminishing Marginal Returns PDFRaj KomolNo ratings yet

- Law of Diminishing Marginal ReturnDocument29 pagesLaw of Diminishing Marginal ReturnTauseef AhmadNo ratings yet

- Law of Diminishing ReturnsDocument28 pagesLaw of Diminishing ReturnsTauseef AhmadNo ratings yet

- Microeconomics Chapter 06Document5 pagesMicroeconomics Chapter 06Hasimuddin TafadarNo ratings yet

- Production and Business Organization: Chapter SixDocument14 pagesProduction and Business Organization: Chapter Sixdipon sakibNo ratings yet

- Economics Chapter 6 SummaryDocument7 pagesEconomics Chapter 6 SummaryAlex HdzNo ratings yet

- Production Function NotesDocument10 pagesProduction Function NotesSzaeNo ratings yet

- Web Ver Diminishing ReturnsDocument7 pagesWeb Ver Diminishing Returnsnasir1975No ratings yet

- Production Function Laws of ReturnsDocument9 pagesProduction Function Laws of ReturnsTarunNo ratings yet

- 3.1 Production Analysis and Concept of MarginalityDocument4 pages3.1 Production Analysis and Concept of MarginalityFoisal Mahmud RownakNo ratings yet

- Laws of ReturnDocument26 pagesLaws of Returnsteverubial47maxNo ratings yet

- PBD - M3Document20 pagesPBD - M3m2fta2311No ratings yet

- Law of Diminishing Marginal UtilityDocument3 pagesLaw of Diminishing Marginal Utilityanon_79168841No ratings yet

- Increasing Returns To Scale in ProductionDocument8 pagesIncreasing Returns To Scale in ProductionjulieNo ratings yet

- Lesson 2 For Macro EconomicsDocument7 pagesLesson 2 For Macro Economicskarlmossesgeld.oxciano.fNo ratings yet

- Diminishing Returns - Wikip..Document4 pagesDiminishing Returns - Wikip..KumarNo ratings yet

- EcoDocument1 pageEcoracthedevilNo ratings yet

- Unit 3: Managerial EconomicsDocument29 pagesUnit 3: Managerial Economicsarjun singh100% (1)

- Price Elasticity of Demand: Reference Notes For Assignment 5Document9 pagesPrice Elasticity of Demand: Reference Notes For Assignment 5Nikita PatelNo ratings yet

- A2 ECON-119-1 Osunero, LeazyDocument6 pagesA2 ECON-119-1 Osunero, Leazyleanzyjenel domiginaNo ratings yet

- Research Work 2Document2 pagesResearch Work 2kassel PlacienteNo ratings yet

- The Production FunctionDocument9 pagesThe Production FunctionPankaj TirkeyNo ratings yet

- Consumer EquilibriumDocument35 pagesConsumer EquilibriumAngel ChakrabortyNo ratings yet

- WEEK3 LESSON 4 Production FunctionDocument4 pagesWEEK3 LESSON 4 Production FunctionSixd WaznineNo ratings yet

- MBA Managerial Economics Chapter 3Document42 pagesMBA Managerial Economics Chapter 3Melese CherieNo ratings yet

- Theory of Production - 05012015 - 060332AM PDFDocument17 pagesTheory of Production - 05012015 - 060332AM PDFsanaNo ratings yet

- Module 3 QBDocument11 pagesModule 3 QBKevin V bijuNo ratings yet

- Managerial EconomicsDocument55 pagesManagerial EconomicsNelson MarwinNo ratings yet

- Unit-3 EconomicsDocument66 pagesUnit-3 EconomicsMohit SoniNo ratings yet

- Lecture-11 Production TheoryDocument18 pagesLecture-11 Production TheoryMovie SeriesNo ratings yet

- Managerial Economic Note For 3 4 5 ChaptersDocument20 pagesManagerial Economic Note For 3 4 5 ChapterseconoNo ratings yet

- Neoclassical Growth TheoryDocument24 pagesNeoclassical Growth Theoryprince marcNo ratings yet

- Activity 4 QuestionsDocument5 pagesActivity 4 QuestionsReginald ValenciaNo ratings yet

- Production Theory in Economics - 093835Document26 pagesProduction Theory in Economics - 093835abdullahiismailisaNo ratings yet

- Managerial Economics: Activity # 7Document9 pagesManagerial Economics: Activity # 7Vienna MamarilNo ratings yet

- Cost Revision NotesDocument9 pagesCost Revision NotesJyot NarangNo ratings yet

- Managerial Economics Section 1: Production AnalysisDocument30 pagesManagerial Economics Section 1: Production AnalysisishitabaxiNo ratings yet

- Production Function and Cost AnalysisDocument18 pagesProduction Function and Cost Analysisharitha aitsNo ratings yet

- Module 3 - Production and CostDocument27 pagesModule 3 - Production and CostGemman Gabriel MapaNo ratings yet

- Law of Returns: Production FunctionDocument5 pagesLaw of Returns: Production FunctionriyaNo ratings yet

- Chapter 4 - Laws of ProductionDocument33 pagesChapter 4 - Laws of ProductionGarima ThakurNo ratings yet

- Production Unit - 4Document24 pagesProduction Unit - 4Goutham AppuNo ratings yet

- EEA Unit III 2023Document57 pagesEEA Unit III 2023Dr Gampala PrabhakarNo ratings yet

- Economics Project Production FunctionDocument13 pagesEconomics Project Production FunctionApurva Gupta100% (2)

- Production and Business Organization PDFDocument12 pagesProduction and Business Organization PDFUmerSaeedNo ratings yet

- Untitled Document-1Document13 pagesUntitled Document-1Gaurav GuptaNo ratings yet

- Chapter - 6 Production - NidhiDocument16 pagesChapter - 6 Production - NidhiRitesh RajNo ratings yet

- Reason For Increasing Returns (Explained With Diagram)Document3 pagesReason For Increasing Returns (Explained With Diagram)anon_867875085No ratings yet

- Price Level Basket of Selected Goods: InflationDocument7 pagesPrice Level Basket of Selected Goods: InflationBishal ShawNo ratings yet

- Health Econ Report PPT FINAL 1Document21 pagesHealth Econ Report PPT FINAL 1Jannah Faye BilarNo ratings yet

- SSE 106 Microeconomics: Institute of Education, Arts & SciencesDocument30 pagesSSE 106 Microeconomics: Institute of Education, Arts & SciencesAnjo Espela VelascoNo ratings yet

- Eco 2Document3 pagesEco 2Surya RNo ratings yet

- Lecture Notes For Business Economics (BUS-704) - 4: - Dr. Mirza Azizul IslamDocument10 pagesLecture Notes For Business Economics (BUS-704) - 4: - Dr. Mirza Azizul Islamtarek aminNo ratings yet

- Production and Cost AnalysisDocument14 pagesProduction and Cost AnalysisPauline OsorioNo ratings yet

- Theory of Production and Cost BA-IDocument21 pagesTheory of Production and Cost BA-IHitesh BalhaliaNo ratings yet

- Economies of Scale: Marginal ReturnsDocument1 pageEconomies of Scale: Marginal ReturnsPatric CletusNo ratings yet

- Industrial EconomicsDocument26 pagesIndustrial Economicsnishanthreddy89No ratings yet

- Chapter 5: The Theory of Production: Rosey Jazz V. Era Bsba 1B Class No.14Document7 pagesChapter 5: The Theory of Production: Rosey Jazz V. Era Bsba 1B Class No.14ROSEY JAZZ ERANo ratings yet

- Me Unit IiiDocument9 pagesMe Unit IiiDivya DCMNo ratings yet

- Gec PF InsuranceDocument11 pagesGec PF InsuranceBryant Daniel Arguelles GacusNo ratings yet

- History Chapter 7 and 8Document11 pagesHistory Chapter 7 and 8Bryant Daniel Arguelles GacusNo ratings yet

- BAC1 Business OrganizationDocument28 pagesBAC1 Business OrganizationBryant Daniel Arguelles GacusNo ratings yet

- Basic Microeconomics QuizDocument1 pageBasic Microeconomics QuizBryant Daniel Arguelles GacusNo ratings yet

- Basic Microeconomics Context Diminishing ReturnsDocument6 pagesBasic Microeconomics Context Diminishing ReturnsBryant Daniel Arguelles GacusNo ratings yet

- Basic Microeconomics Context Profit MaximizationDocument3 pagesBasic Microeconomics Context Profit MaximizationBryant Daniel Arguelles GacusNo ratings yet

- Basic Microeconomics IMSDocument6 pagesBasic Microeconomics IMSBryant Daniel Arguelles GacusNo ratings yet

- Toaz - Info Accounting by Carl S Warren James M Reeve Jonathan Duchac PRDocument80 pagesToaz - Info Accounting by Carl S Warren James M Reeve Jonathan Duchac PRJa DeNo ratings yet

- 1-Z-Test For Mean PDFDocument20 pages1-Z-Test For Mean PDFKhanal Nilambar0% (1)

- SPF 2000 Bill FormsDocument17 pagesSPF 2000 Bill Formskarunamoorthi_p220957% (7)

- Adobe Scan 02-Jul-2022Document4 pagesAdobe Scan 02-Jul-2022Akshita SethiNo ratings yet

- Marxist Thought On Imperialism Survey and Critique by Charles A. BaroneDocument238 pagesMarxist Thought On Imperialism Survey and Critique by Charles A. BaroneFernandaNo ratings yet

- 2014 Rapala CanadaDocument136 pages2014 Rapala Canadagbqfnq2p8bNo ratings yet

- Tutorial 5Document3 pagesTutorial 5Nur Arisya AinaaNo ratings yet

- Property List 10-26-2020Document146 pagesProperty List 10-26-2020Tont TizzleNo ratings yet

- Brosur ARIN PARTITIONDocument12 pagesBrosur ARIN PARTITIONMomo mwsNo ratings yet

- A Simple Approximation of Tobin's QDocument6 pagesA Simple Approximation of Tobin's Qwxmnxfm57wNo ratings yet

- Chemistry 1 Tutor - Vol 2 - Worksheet 10 - Limiting Reactants - Part 1Document12 pagesChemistry 1 Tutor - Vol 2 - Worksheet 10 - Limiting Reactants - Part 1lightningpj1234No ratings yet

- Seferiadis 2018 PDFDocument88 pagesSeferiadis 2018 PDFOleksandrNo ratings yet

- Ga Sheravest RP EnglischDocument2 pagesGa Sheravest RP EnglischOlariu FaneNo ratings yet

- Arup Scheme Design GuideDocument139 pagesArup Scheme Design GuideDean TyrrellNo ratings yet

- Memorandum of Understanding-SubvendorsDocument3 pagesMemorandum of Understanding-SubvendorsfazilskNo ratings yet

- 1.62 How To Handle Advance Purchase Bookings PDFDocument1 page1.62 How To Handle Advance Purchase Bookings PDFsNo ratings yet

- Crochet PatternsDocument25 pagesCrochet PatternsDoris LiNo ratings yet

- BanKO Partner Outlet LocatorDocument344 pagesBanKO Partner Outlet LocatorBPI Globe BanKONo ratings yet

- Module 4 - DepreciationDocument70 pagesModule 4 - DepreciationGaurav ShekharNo ratings yet

- Transcription - Charl Cilliers (06.09.18)Document86 pagesTranscription - Charl Cilliers (06.09.18)Leila DouganNo ratings yet

- The Leather Biker JacketDocument19 pagesThe Leather Biker JacketMichaela MohamedNo ratings yet

- Cambridge International Advanced Subsidiary and Advanced LevelDocument12 pagesCambridge International Advanced Subsidiary and Advanced LevelZayed BoodhooNo ratings yet

- The Art of Livin' Virtual Live Event - YouTubeDocument1 pageThe Art of Livin' Virtual Live Event - YouTubeViktor VorskiNo ratings yet

- Philippine Manpower and Equipment Productivity RatioDocument4 pagesPhilippine Manpower and Equipment Productivity RatioMaricel Santos AdNo ratings yet

- Paper 6 Efficient and Reliable Handling of Granulated Blast Furnace Slag PDFDocument16 pagesPaper 6 Efficient and Reliable Handling of Granulated Blast Furnace Slag PDFLarisa ChindrișNo ratings yet

- Furniture and Wood Pakistan ImporterDocument10 pagesFurniture and Wood Pakistan ImporterSheroz AhmedNo ratings yet

- Chapter 4 (Color)Document61 pagesChapter 4 (Color)danielNo ratings yet

- الطاقة المتجددة كخيار استراتيجي لتحقيق التنمية المستدامةDocument14 pagesالطاقة المتجددة كخيار استراتيجي لتحقيق التنمية المستدامةُElhadj arabaNo ratings yet

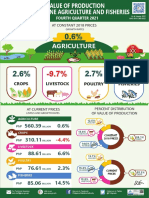

- Infographics, Value of Production in Philippine Agriculture and Fisheries, Fourth Quarter 2021Document1 pageInfographics, Value of Production in Philippine Agriculture and Fisheries, Fourth Quarter 2021Cart LaneNo ratings yet