You might also like

- HOSHIZAKI SERVICE MANUAL Logic Board Settings E1ck-811 PDFDocument118 pagesHOSHIZAKI SERVICE MANUAL Logic Board Settings E1ck-811 PDFLeo50% (2)

- Lecture 11Document4 pagesLecture 11armailgmNo ratings yet

- WIRING DIAGRAM Wifi VendoDocument5 pagesWIRING DIAGRAM Wifi VendoDikdik PribadiNo ratings yet

- Simple Test for Heteroscedasticity and Random Coefficient VariationDocument9 pagesSimple Test for Heteroscedasticity and Random Coefficient VariationPedro ManoelNo ratings yet

- Second-Order Nonlinear Least Squares Estimation: Liqun WangDocument18 pagesSecond-Order Nonlinear Least Squares Estimation: Liqun WangJyoti GargNo ratings yet

- Switching Regression Models and Fuzzy Clustering: Richard CDocument10 pagesSwitching Regression Models and Fuzzy Clustering: Richard CAli Umair KhanNo ratings yet

- J Spa 2008 03 006Document29 pagesJ Spa 2008 03 006romuald ouaboNo ratings yet

- Heuristic stability theory for finite-difference equationsDocument17 pagesHeuristic stability theory for finite-difference equationsKaustubhNo ratings yet

- A Convenient Way of Generating Normal Random Variables Using Generalized Exponential DistributionDocument11 pagesA Convenient Way of Generating Normal Random Variables Using Generalized Exponential DistributionvsalaiselvamNo ratings yet

- V A Atanasov Et Al - Fordy-Kulish Model and Spinor Bose-Einstein CondensateDocument8 pagesV A Atanasov Et Al - Fordy-Kulish Model and Spinor Bose-Einstein CondensatePomac232No ratings yet

- Nataf ModelDocument8 pagesNataf ModelLaura ManolacheNo ratings yet

- Royal Statistical Society, Wiley Journal of The Royal Statistical Society. Series B (Methodological)Document10 pagesRoyal Statistical Society, Wiley Journal of The Royal Statistical Society. Series B (Methodological)Ong Van HoangNo ratings yet

- The Review of Economic Studies, LTD.: Oxford University PressDocument16 pagesThe Review of Economic Studies, LTD.: Oxford University PressHoussem Eddine FayalaNo ratings yet

- Statistical Papers 47, 471-479 (2006)Document9 pagesStatistical Papers 47, 471-479 (2006)أبن الرماديNo ratings yet

- SilveyDocument20 pagesSilveyEzy VoNo ratings yet

- Computational Aspects of Maximum Likelihood Estimation of Autoregressive Fractionally Integratedmoving Average ModelsDocument16 pagesComputational Aspects of Maximum Likelihood Estimation of Autoregressive Fractionally Integratedmoving Average ModelsSuci Schima WulandariNo ratings yet

- AutocorrelationDocument38 pagesAutocorrelationHoàng TuấnNo ratings yet

- Differential Equations : A Uniqueness Theorem For OrdinaryDocument4 pagesDifferential Equations : A Uniqueness Theorem For OrdinarySon HoangNo ratings yet

- Landau Lifshtz PDFDocument4 pagesLandau Lifshtz PDFyacinephysiqueNo ratings yet

- Asymptotic properties of solutions to hyperbolic equationsDocument10 pagesAsymptotic properties of solutions to hyperbolic equationsDandi BachtiarNo ratings yet

- Modal Analysis Approximate MethodsDocument9 pagesModal Analysis Approximate MethodsRafaAlmeidaNo ratings yet

- Depmix S4Document17 pagesDepmix S4mateusfmpetryNo ratings yet

- Notes On ARIMA Modelling: Brian Borchers November 22, 2002Document19 pagesNotes On ARIMA Modelling: Brian Borchers November 22, 2002Daryl ChinNo ratings yet

- Van Staden and Loots 2009 ASEARCDocument4 pagesVan Staden and Loots 2009 ASEARCjcaceresalNo ratings yet

- SODEHigjhamDocument23 pagesSODEHigjham小半No ratings yet

- Basic Concepts of StatisticsDocument24 pagesBasic Concepts of StatisticstimobechgerNo ratings yet

- Distribuição AmplitudeDocument10 pagesDistribuição AmplitudeTItoNo ratings yet

- Quantum Theory of Femtosecond Soliton Propagation in Single-Mode Optical FibersDocument6 pagesQuantum Theory of Femtosecond Soliton Propagation in Single-Mode Optical FibershackerofxpNo ratings yet

- CooksDocument5 pagesCooksPatricia Calvo PérezNo ratings yet

- Maximum Likelihood Estimation of Stationary Multivariate ARFIMA Processes TSayDocument17 pagesMaximum Likelihood Estimation of Stationary Multivariate ARFIMA Processes TSayAdis SalkicNo ratings yet

- Testing Dynamic Econometric ModelsDocument6 pagesTesting Dynamic Econometric ModelsMaria RoaNo ratings yet

- A Generalized Jarque-Bera Test for Conditional NormalityDocument12 pagesA Generalized Jarque-Bera Test for Conditional NormalitytomrescoNo ratings yet

- Ijaret: ©iaemeDocument8 pagesIjaret: ©iaemeIAEME PublicationNo ratings yet

- Tibs Jrssb96Document23 pagesTibs Jrssb96sunbenNo ratings yet

- Lecture Notes GLSDocument5 pagesLecture Notes GLSKasem AhmedNo ratings yet

- 2.1972 Generalized Linear Models Nelder WedderburnDocument16 pages2.1972 Generalized Linear Models Nelder WedderburnsssNo ratings yet

- The Rate of Expansion of Spherical FlamesDocument18 pagesThe Rate of Expansion of Spherical Flamesv_karlinNo ratings yet

- Strang (1968) - On The Construction and Comparison of Difference SchemesDocument13 pagesStrang (1968) - On The Construction and Comparison of Difference SchemeslanwatchNo ratings yet

- Differential Quadrature MethodDocument13 pagesDifferential Quadrature MethodShannon HarrisNo ratings yet

- Numerical Methods and Software For Sensitivity Analysis of Differential-Algebraic SystemsDocument23 pagesNumerical Methods and Software For Sensitivity Analysis of Differential-Algebraic SystemsFCNo ratings yet

- ASGDDocument18 pagesASGDRogério MainardesNo ratings yet

- Effective Action and Renormalization Group Flow of Anisotropic SuperconductorsDocument19 pagesEffective Action and Renormalization Group Flow of Anisotropic SuperconductorssatyabashaNo ratings yet

- 1982 - Algorithm 583 LSQR Sparse LinearDocument15 pages1982 - Algorithm 583 LSQR Sparse LinearluongxuandanNo ratings yet

- American Statistical Association American Society For QualityDocument8 pagesAmerican Statistical Association American Society For QualityAlbanita MendesNo ratings yet

- Regression Models With Unknown Singular Covariance Matrix: Muni S. Srivastava, Dietrich Von RosenDocument19 pagesRegression Models With Unknown Singular Covariance Matrix: Muni S. Srivastava, Dietrich Von RosenAnonymous rQ57WOmNo ratings yet

- 08 Aos674Document30 pages08 Aos674siti hayatiNo ratings yet

- VECM JMultiDocument40 pagesVECM JMultijota de copasNo ratings yet

- Proper Orthogonal DecompositionDocument10 pagesProper Orthogonal DecompositionKenry Xu ChiNo ratings yet

- Dynamical Equations For Optimal Nonlinear Filtering: DX F (X, T) DT + W2 (X, T) DZDocument12 pagesDynamical Equations For Optimal Nonlinear Filtering: DX F (X, T) DT + W2 (X, T) DZhenrydclNo ratings yet

- Nonlinear Least SQ: Queensland 4001, AustraliaDocument17 pagesNonlinear Least SQ: Queensland 4001, AustraliaAbdul AzizNo ratings yet

- On The Generalized Differential Transform Method: Application To Fractional Integro-Differential EquationsDocument9 pagesOn The Generalized Differential Transform Method: Application To Fractional Integro-Differential EquationsKanthavel ThillaiNo ratings yet

- Ambrosio e Gangbo Hamilton Ian ODEDocument35 pagesAmbrosio e Gangbo Hamilton Ian ODEelismar01No ratings yet

- Additivity and Multiplicativity Properties of Some Gaussian Channels For Gaussian InputsDocument9 pagesAdditivity and Multiplicativity Properties of Some Gaussian Channels For Gaussian InputsgejikeijiNo ratings yet

- An Adaptive Nonlinear Least-Squares AlgorithmDocument21 pagesAn Adaptive Nonlinear Least-Squares AlgorithmOleg ShirokobrodNo ratings yet

- Mathematics: Least-Squares Estimators of Drift Parameter For Discretely Observed Fractional Ornstein-Uhlenbeck ProcessesDocument20 pagesMathematics: Least-Squares Estimators of Drift Parameter For Discretely Observed Fractional Ornstein-Uhlenbeck ProcessesthyagosmesmeNo ratings yet

- Complex Analysis of The Lossy-Transmission Line Theory: A Generalized Smith ChartDocument22 pagesComplex Analysis of The Lossy-Transmission Line Theory: A Generalized Smith ChartRabah ZaimeddineNo ratings yet

- 1 s2.0 S1474667016428351 MainDocument6 pages1 s2.0 S1474667016428351 MainhassanNo ratings yet

- The Econometric SocietyDocument16 pagesThe Econometric SocietyAdriana SenaNo ratings yet

- Research StatementDocument5 pagesResearch StatementEmad AbdurasulNo ratings yet

- Difference Equations in Normed Spaces: Stability and OscillationsFrom EverandDifference Equations in Normed Spaces: Stability and OscillationsNo ratings yet

- The Plasma Dispersion Function: The Hilbert Transform of the GaussianFrom EverandThe Plasma Dispersion Function: The Hilbert Transform of the GaussianRating: 5 out of 5 stars5/5 (1)

- Testing For Unconditional Predictive Ability (Clark y McCraken)Document32 pagesTesting For Unconditional Predictive Ability (Clark y McCraken)Andrés JiménezNo ratings yet

- Not All Oil Price Shocks Are Alike - Disentangling Demand and Supply Shocks in The Crude Oil Market (Lutz Kilian)Document22 pagesNot All Oil Price Shocks Are Alike - Disentangling Demand and Supply Shocks in The Crude Oil Market (Lutz Kilian)Andrés JiménezNo ratings yet

- Optimal Monetary Policy in Open Versus Closed Economies - An Integrated Approach (Clarida, Galí y Gertler)Document6 pagesOptimal Monetary Policy in Open Versus Closed Economies - An Integrated Approach (Clarida, Galí y Gertler)Andrés JiménezNo ratings yet

- Testing The Order of Differencing in ARIMA Models (Jansson)Document28 pagesTesting The Order of Differencing in ARIMA Models (Jansson)Andrés JiménezNo ratings yet

- Tests For Specification Errors in Classical Linear Least-Squares Regression Analysis (Ramsey)Document23 pagesTests For Specification Errors in Classical Linear Least-Squares Regression Analysis (Ramsey)Andrés JiménezNo ratings yet

- The New Econometrics of Structural Change - Dating Breaks in U.S. Labor Productivity (Bruce Hansen)Document13 pagesThe New Econometrics of Structural Change - Dating Breaks in U.S. Labor Productivity (Bruce Hansen)Andrés JiménezNo ratings yet

- The Lagrange Multiplier Test and Its Applications To Model Specification in Econometrics (Breusch y Pagan)Document16 pagesThe Lagrange Multiplier Test and Its Applications To Model Specification in Econometrics (Breusch y Pagan)Andrés JiménezNo ratings yet

- The Science of Monetary Policy - A New Keynesian Perspective (Clarida, Galí y Gertler)Document48 pagesThe Science of Monetary Policy - A New Keynesian Perspective (Clarida, Galí y Gertler)Andrés JiménezNo ratings yet

- Using The Generalized Schur Form To Solve A Multivariate Linear Rational Expectations Model (Paul Klein)Document19 pagesUsing The Generalized Schur Form To Solve A Multivariate Linear Rational Expectations Model (Paul Klein)Andrés JiménezNo ratings yet

- Back To Square One - Identification Issues in DSGE Models (Canova y Sala)Document48 pagesBack To Square One - Identification Issues in DSGE Models (Canova y Sala)Andrés JiménezNo ratings yet

- Formulating Wald Tests of Nonlinear Restrictions (Gregory y Veall)Document5 pagesFormulating Wald Tests of Nonlinear Restrictions (Gregory y Veall)Andrés JiménezNo ratings yet

- Comparing Dynamic Equilibrium Models To Data - A Bayesian Approach (Fernández-Villaverde y Rubio-Ramírez)Document35 pagesComparing Dynamic Equilibrium Models To Data - A Bayesian Approach (Fernández-Villaverde y Rubio-Ramírez)Andrés JiménezNo ratings yet

- An Empirical Characterization of The Dynamic Effects of Changes in Government Spending and Taxes On Output (Blanchard y Perotti)Document41 pagesAn Empirical Characterization of The Dynamic Effects of Changes in Government Spending and Taxes On Output (Blanchard y Perotti)Andrés JiménezNo ratings yet

- Inglés Técnico 01Document23 pagesInglés Técnico 01Stefany DulkaNo ratings yet

- Catalogo VPFT 4535Document91 pagesCatalogo VPFT 4535PRISCILA FAGUNDESNo ratings yet

- 2) N5, N6 and N7 (NPS2 - 300#) PDFDocument20 pages2) N5, N6 and N7 (NPS2 - 300#) PDFpraffulNo ratings yet

- Scientific Publishing in Biomedicine How To Choose A JournalDocument9 pagesScientific Publishing in Biomedicine How To Choose A JournalJuan Carlos Marcos EnriquezNo ratings yet

- PC400 8 1Document549 pagesPC400 8 1Eka Anwar100% (1)

- Histograms Answers MMEDocument5 pagesHistograms Answers MMEEffNo ratings yet

- LP Math 7 (4) (Integers-Division)Document2 pagesLP Math 7 (4) (Integers-Division)Rookie LoraNo ratings yet

- SPG/SSG Election Report: Attachment 1Document4 pagesSPG/SSG Election Report: Attachment 1Nexus BallesterosNo ratings yet

- Computer Practical (C++ Programs) For CBSE XII Practical ExamsDocument74 pagesComputer Practical (C++ Programs) For CBSE XII Practical ExamsShiladitya67% (89)

- Evaluating Pipeline Ovality Acceptability Criteria For Straight Pipe SectionsDocument7 pagesEvaluating Pipeline Ovality Acceptability Criteria For Straight Pipe Sectionsravikr95No ratings yet

- Tez PortalDocument1 pageTez Portalkiran BawadkarNo ratings yet

- Ac6905a DatasheepDocument10 pagesAc6905a DatasheepMUSIC ELECNo ratings yet

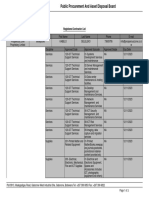

- Registered Contractor List PPADBDocument3 pagesRegistered Contractor List PPADBGaone Lydia SetlhodiNo ratings yet

- PartnerDocument14 pagesPartnerLeo van GorkumNo ratings yet

- Advanced Construction TechnologyDocument6 pagesAdvanced Construction TechnologyNik SoniNo ratings yet

- Digital Fluency Module 2Document3 pagesDigital Fluency Module 2vinayNo ratings yet

- Sri Lanka water network flow calculationsDocument2 pagesSri Lanka water network flow calculationsNiroshan SridharanNo ratings yet

- Cat - IDocument2 pagesCat - IGanesh KumarNo ratings yet

- Rainvue SeriesDocument50 pagesRainvue Seriesradicall8No ratings yet

- MANOVA SPSS TablesDocument5 pagesMANOVA SPSS Tabless_m_u_yousafNo ratings yet

- IRJET Online Student PortalDocument6 pagesIRJET Online Student PortalEmmanuel FerolinoNo ratings yet

- FMM Directory2013 - Extract - 140120Document1,436 pagesFMM Directory2013 - Extract - 140120Fadzilah MohamadNo ratings yet

- 24 Territory Brochure enDocument12 pages24 Territory Brochure enmohammed sameer100% (1)

- Notes:: Brisbane City Council Standard DrawingDocument1 pageNotes:: Brisbane City Council Standard DrawingShaunitchi El GrecoNo ratings yet

- The Ultimate Guide To WaterjetDocument9 pagesThe Ultimate Guide To WaterjetNsidibe Michael EtimNo ratings yet

- Armstrong Retail Ceiling Guide With Product Comparison To USG and TeedDocument36 pagesArmstrong Retail Ceiling Guide With Product Comparison To USG and TeedAdam WernerNo ratings yet

- Guia de Configuracion de Firewall Basico en GWN7000 Grandstream PDFDocument16 pagesGuia de Configuracion de Firewall Basico en GWN7000 Grandstream PDFmiguel pcNo ratings yet

- Kandi. Sai Pavan Kumar: Career ObjectiveDocument2 pagesKandi. Sai Pavan Kumar: Career ObjectiveSai PavanNo ratings yet