You might also like

- Avoiding and Managing Us Business Litigation Risks: A Comprehensive Guide for Business Owners and the Attorneys Who Advise ThemFrom EverandAvoiding and Managing Us Business Litigation Risks: A Comprehensive Guide for Business Owners and the Attorneys Who Advise ThemNo ratings yet

- Exam 1 Section 1 - AnswersDocument26 pagesExam 1 Section 1 - AnswersChuchai Jittaviroj100% (1)

- Exam 1 Section 2 - AnswersDocument26 pagesExam 1 Section 2 - AnswersChuchai JittavirojNo ratings yet

- Exam 2 Section 2 - AnswersDocument25 pagesExam 2 Section 2 - AnswersChuchai JittavirojNo ratings yet

- SIMU1 L1 PM Jun17 QADocument25 pagesSIMU1 L1 PM Jun17 QAnicolas.nunez.ugarteNo ratings yet

- CFA Level 16 Ans PDFDocument46 pagesCFA Level 16 Ans PDFPunit SharmaNo ratings yet

- Reading 42.3 Standards of Professional Conduct Guidance For Standards III - AnswersDocument41 pagesReading 42.3 Standards of Professional Conduct Guidance For Standards III - Answerstristan.riolsNo ratings yet

- Jun18l1eth-E03 QaDocument2 pagesJun18l1eth-E03 Qarafav10No ratings yet

- 2023 A Morning Session SolutionsDocument41 pages2023 A Morning Session SolutionsЧулуунбаатар ХалиунNo ratings yet

- Mock Test 1Document8 pagesMock Test 1Thị Tường NguyễnNo ratings yet

- R03.3 Standard III Duties To Clients - AnswersDocument50 pagesR03.3 Standard III Duties To Clients - AnswersxssfsdfsfNo ratings yet

- R02.5 Guidance For Standards III (C), III (D), and III (E) - AnswersDocument25 pagesR02.5 Guidance For Standards III (C), III (D), and III (E) - AnswersTruong Dac HuyNo ratings yet

- Test Collections CFA-Level-I Question Bank PDFDocument1,568 pagesTest Collections CFA-Level-I Question Bank PDFsaurabh100% (1)

- 04 Standards of Professional ... Dance - Duties To ClientsDocument22 pages04 Standards of Professional ... Dance - Duties To ClientsIves LeeNo ratings yet

- Brain DumpsDocument2,240 pagesBrain DumpsVeenu RajNo ratings yet

- V1 Exam 2 AM - AnswersDocument55 pagesV1 Exam 2 AM - AnswersHarsh KabraNo ratings yet

- Mock 06 Aug 2022 SolutionDocument4 pagesMock 06 Aug 2022 SolutionCuong LyNo ratings yet

- Reading 42.3 Standards of Professional Conduct Guidance For Standards IIIDocument29 pagesReading 42.3 Standards of Professional Conduct Guidance For Standards IIItristan.riolsNo ratings yet

- R02.4 Standard III (A) - AnswersDocument11 pagesR02.4 Standard III (A) - AnswersShashwat DesaiNo ratings yet

- V2 Exam 1 AM - AnswersDocument52 pagesV2 Exam 1 AM - AnswersNeeraj100% (1)

- AA MA-2022 Suggested AnswersDocument8 pagesAA MA-2022 Suggested AnswersMehedi Hasan TouhidNo ratings yet

- Port Man Quiz Stuff PDFDocument53 pagesPort Man Quiz Stuff PDFHein BreunissenNo ratings yet

- 07 Standards of Professional Conduct & Guidance-Conflicts of Interest PDFDocument11 pages07 Standards of Professional Conduct & Guidance-Conflicts of Interest PDFSardonna FongNo ratings yet

- Reading 91.4 Guidance For Standards III (A) and III (B) - AnswersDocument13 pagesReading 91.4 Guidance For Standards III (A) and III (B) - AnswersTNHNo ratings yet

- Version A Morning Session Merged 9766 Taptin0 1 100 1856 TaptinDocument100 pagesVersion A Morning Session Merged 9766 Taptin0 1 100 1856 Taptinalxalx29119412No ratings yet

- Jun18l1eth-E04 QaDocument3 pagesJun18l1eth-E04 Qarafav10No ratings yet

- Test 0 - AM - ADocument17 pagesTest 0 - AM - ADữ NguyễnNo ratings yet

- Exam 1 AmDocument51 pagesExam 1 AmShanzah SaNo ratings yet

- 04 Standards of Professional Conduct & Guidance-Duties To Clients PDFDocument15 pages04 Standards of Professional Conduct & Guidance-Duties To Clients PDFSardonna FongNo ratings yet

- R03.3 Standard III Duties To ClientsDocument14 pagesR03.3 Standard III Duties To ClientsxczcNo ratings yet

- Reading 71-1 Guidance For Standards I-VIIDocument114 pagesReading 71-1 Guidance For Standards I-VIINeerajNo ratings yet

- Jawaban Case 5.3Document2 pagesJawaban Case 5.3Ajeng TriyanaNo ratings yet

- SIMU1 L1 AM Jun17 QADocument25 pagesSIMU1 L1 AM Jun17 QAnicolas.nunez.ugarteNo ratings yet

- Reading 71.2 Guidance For Standards I (C) and I (D)Document11 pagesReading 71.2 Guidance For Standards I (C) and I (D)AmineNo ratings yet

- CFA L1 SCHWSR FL Test Ques+Ans - NDocument52 pagesCFA L1 SCHWSR FL Test Ques+Ans - NAdamNo ratings yet

- Exam 1 Section 2Document23 pagesExam 1 Section 2Chuchai Jittaviroj100% (1)

- 2-6int 2002 Dec ADocument14 pages2-6int 2002 Dec AJay ChenNo ratings yet

- Starting A Business Los AngelesDocument14 pagesStarting A Business Los AngelesCompany Counsel PCNo ratings yet

- Ethical and Professional Standards - AnswersDocument8 pagesEthical and Professional Standards - AnswersCharu KokraNo ratings yet

- CFA Level I Mock Exam B - February 2022Document109 pagesCFA Level I Mock Exam B - February 2022Hường Trần Thu100% (1)

- Reading 42.1 Standards of Professional Conduct Guidance For Standards I - AnswersDocument25 pagesReading 42.1 Standards of Professional Conduct Guidance For Standards I - Answerstristan.riolsNo ratings yet

- Semester Test 2 MAN308 SolutionDocument8 pagesSemester Test 2 MAN308 SolutionDan Saul KnightNo ratings yet

- R03.4 Guidance For Standards III (A) and III (B)Document14 pagesR03.4 Guidance For Standards III (A) and III (B)Bảo TrâmNo ratings yet

- CFA Level 1 - Test 2 - AMDocument35 pagesCFA Level 1 - Test 2 - AMHongMinhNguyenNo ratings yet

- Ethical and Professional Standards.1677049903020Document25 pagesEthical and Professional Standards.1677049903020Sagar PatroNo ratings yet

- Jun18l1eth-E06 Qa PDFDocument3 pagesJun18l1eth-E06 Qa PDFrafav10No ratings yet

- JUN18L1ETH/E06: Least Likely Violate?Document3 pagesJUN18L1ETH/E06: Least Likely Violate?rafav10No ratings yet

- CFA Level I Revision Day IDocument63 pagesCFA Level I Revision Day IAspanwz SpanwzNo ratings yet

- CFA Level I Mock Exam C Morning SessionDocument67 pagesCFA Level I Mock Exam C Morning SessionSai Swaroop MandalNo ratings yet

- ViolationsDocument2 pagesViolationsont12522No ratings yet

- R03.5 Guidance For Standards III (C), III (D), and III (E)Document12 pagesR03.5 Guidance For Standards III (C), III (D), and III (E)Bảo TrâmNo ratings yet

- R02.6 Standards III (D) and III (E) - AnswersDocument7 pagesR02.6 Standards III (D) and III (E) - AnswersShashwat DesaiNo ratings yet

- Jun18l1eth-C03 QaDocument2 pagesJun18l1eth-C03 Qarafav10No ratings yet

- 2015 CFA Level 3 Mock Exam Afternoon - AnsDocument53 pages2015 CFA Level 3 Mock Exam Afternoon - AnsElsiiieNo ratings yet

- Mock Exam 4 - AnswersDocument78 pagesMock Exam 4 - AnswersAditya MuchhalaNo ratings yet

- Ethics AssignmentDocument16 pagesEthics AssignmentNghĩaTrầnNo ratings yet

- Ethics AssignmentDocument16 pagesEthics AssignmentNghĩaTrầnNo ratings yet

- Mock Exam 1 - AnswersDocument15 pagesMock Exam 1 - AnswersKim QuyênNo ratings yet

- Aaa 5Document3 pagesAaa 5Hamza ZahidNo ratings yet

- Freight CalculatorDocument2 pagesFreight CalculatorOverhauled ArtsNo ratings yet

- Indicated in Syllabus: See Only Footnote #1: (2) Albano V. ReyesDocument1 pageIndicated in Syllabus: See Only Footnote #1: (2) Albano V. ReyesJul A.No ratings yet

- E Commerce QuestionsDocument4 pagesE Commerce Questionsbharani100% (1)

- Vendor DetailDocument4 pagesVendor DetailKamal PashaNo ratings yet

- Chapter 7 Project Termination and Project Management Practices in BDDocument19 pagesChapter 7 Project Termination and Project Management Practices in BDbba19047No ratings yet

- COB 1 History of ManagementDocument18 pagesCOB 1 History of ManagementWhat le fuckNo ratings yet

- CA2 Cost Concepts and ClassificationDocument19 pagesCA2 Cost Concepts and ClassificationhellokittysaranghaeNo ratings yet

- PJSC National Bank Trust and Anor V Boris Mints and OrsDocument33 pagesPJSC National Bank Trust and Anor V Boris Mints and OrshyenadogNo ratings yet

- Print - Udyam Registration CertificateDocument3 pagesPrint - Udyam Registration Certificatemanwanimuki12No ratings yet

- "E20" Surface Mount Productivity Improvement Project - Phase 1Document51 pages"E20" Surface Mount Productivity Improvement Project - Phase 1JAYANT SINGHNo ratings yet

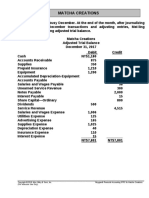

- MC4 Matcha Creations: (For Instructor Use Only)Document2 pagesMC4 Matcha Creations: (For Instructor Use Only)Reza eka PutraNo ratings yet

- CSE4003 - Cyber Security: Digital Assignment IDocument15 pagesCSE4003 - Cyber Security: Digital Assignment IjustadityabistNo ratings yet

- Guide To SQL 9th Edition by Pratt Last Solution ManualDocument13 pagesGuide To SQL 9th Edition by Pratt Last Solution Manualcatherinebergtjkxfanwod100% (25)

- Reflection Paper 2 (MM)Document1 pageReflection Paper 2 (MM)Paul Irineo MontanoNo ratings yet

- Hilton Hotels - Brand Differentiation Through Customer RelationshipDocument11 pagesHilton Hotels - Brand Differentiation Through Customer RelationshipYash Pratap SinghNo ratings yet

- Gender Pay Gap - HSBCDocument17 pagesGender Pay Gap - HSBCruksana khatoonNo ratings yet

- Deed of Absolute Sale Bod OnDocument4 pagesDeed of Absolute Sale Bod OnNeil John FelicianoNo ratings yet

- A Review On Power Plant Maintenance and OperationaDocument5 pagesA Review On Power Plant Maintenance and OperationaWAN MUHAMMAD IKHWANNo ratings yet

- Branding-Bottled WaterDocument29 pagesBranding-Bottled Watern4b33l100% (1)

- AC415 Fixed Variable Costs BreakEven 1 - 11 - 2017Document35 pagesAC415 Fixed Variable Costs BreakEven 1 - 11 - 2017blablaNo ratings yet

- SIP Report Atharva SableDocument68 pagesSIP Report Atharva Sable7s72p3nswtNo ratings yet

- Separate and Consolidated Dayag Part 6Document4 pagesSeparate and Consolidated Dayag Part 6NinaNo ratings yet

- Computation (Worked Examples and Examination Questions)Document7 pagesComputation (Worked Examples and Examination Questions)A.BensonNo ratings yet

- Thesis 2016-Anthony Amoah CORRECTED PDFDocument209 pagesThesis 2016-Anthony Amoah CORRECTED PDFWalamanNo ratings yet

- Inquiry Ali Vasquez The Florida Bar Re UPL Marty Stone MRLPDocument10 pagesInquiry Ali Vasquez The Florida Bar Re UPL Marty Stone MRLPNeil GillespieNo ratings yet

- Bs in Business Administration Marketing Management: St. Nicolas College of Business and TechnologyDocument6 pagesBs in Business Administration Marketing Management: St. Nicolas College of Business and TechnologyMaria Charise TongolNo ratings yet

- The Rise of NFT FundraisingDocument36 pagesThe Rise of NFT FundraisingTrader CatNo ratings yet

- Essentials of College and University AccountingDocument121 pagesEssentials of College and University AccountingLith CloNo ratings yet

- Use Case: From Wikipedia, The Free EncyclopediaDocument6 pagesUse Case: From Wikipedia, The Free EncyclopediaLisset Garcia PerezNo ratings yet

- Working Capital Management (Bhavani)Document86 pagesWorking Capital Management (Bhavani)gangatulasiNo ratings yet