You might also like

- Real Estate License Exam Calculation Workbook: 250 Calculations to Prepare for the Real Estate License Exam (2023 Edition)From EverandReal Estate License Exam Calculation Workbook: 250 Calculations to Prepare for the Real Estate License Exam (2023 Edition)Rating: 5 out of 5 stars5/5 (1)

- CAPITAL GAINS TAXATION RULESDocument21 pagesCAPITAL GAINS TAXATION RULESW-304-Bautista,PreciousNo ratings yet

- Pestel Analysis On Amazon CharanDocument4 pagesPestel Analysis On Amazon Charancharan chamarthiNo ratings yet

- Grant Agreement 101004480 AI4PublicPolicyDocument332 pagesGrant Agreement 101004480 AI4PublicPolicyBoian PopunkiovNo ratings yet

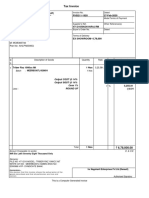

- Tax InvoiceDocument1 pageTax Invoicesourabh choubeyNo ratings yet

- Capital Gains Taxation GuideDocument3 pagesCapital Gains Taxation GuideJustine Paulo EnerlanNo ratings yet

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

- ACI International Concrete PrecastDocument104 pagesACI International Concrete PrecastDaniel Saborío RomanoNo ratings yet

- ESTATE AND DONOR'S TAX GUIDEDocument10 pagesESTATE AND DONOR'S TAX GUIDEJoseph MangahasNo ratings yet

- Noncurrent Asset Held For Sale: Problem 6-1 (IFRS)Document10 pagesNoncurrent Asset Held For Sale: Problem 6-1 (IFRS)Kimberly Claire Atienza71% (7)

- Real Estate Taxation - 12.11.15Document8 pagesReal Estate Taxation - 12.11.15Juan Frivaldo100% (2)

- Capital Gains TaxDocument3 pagesCapital Gains TaxMary Christen Canlas0% (1)

- UK Property Letting: Making Money in the UK Private Rented SectorFrom EverandUK Property Letting: Making Money in the UK Private Rented SectorNo ratings yet

- AUDITING PROBLEMS (CPAR First Preboards 2018) - AnswersDocument10 pagesAUDITING PROBLEMS (CPAR First Preboards 2018) - AnswersVincent Larrie MoldezNo ratings yet

- Investment Properties ComputationDocument4 pagesInvestment Properties ComputationUNKNOWNNNo ratings yet

- Ifrs December 2020 EnglishDocument10 pagesIfrs December 2020 Englishjad NasserNo ratings yet

- ACCA ZWE TAX Multiple Choice Question & Answers 2019Document24 pagesACCA ZWE TAX Multiple Choice Question & Answers 2019Tawanda Tatenda Herbert100% (4)

- EPS QuestionsDocument4 pagesEPS QuestionsJennifer MansourNo ratings yet

- INCTAX Answer and SolutionDocument7 pagesINCTAX Answer and SolutionJonard PasawayNo ratings yet

- CGT AssignementDocument4 pagesCGT AssignementBrandon SibandaNo ratings yet

- Property Income CalculationDocument7 pagesProperty Income CalculationAk AlNo ratings yet

- Quiz 2 CGTDocument2 pagesQuiz 2 CGTHector Quillo Ladua Jr.No ratings yet

- InstructionsDocument2 pagesInstructionsGabriel SNo ratings yet

- Txe-Zwe Exam 2019Document10 pagesTxe-Zwe Exam 2019Gift MoyoNo ratings yet

- P6-Capital Taxes - IHT & CGTDocument9 pagesP6-Capital Taxes - IHT & CGTAnonymous rePT5rCrNo ratings yet

- Fa2 DepreciationDocument4 pagesFa2 Depreciationamna zamanNo ratings yet

- Fadm / Group Case Study/ Joyo IncDocument3 pagesFadm / Group Case Study/ Joyo IncS GuptaNo ratings yet

- Property, Plant and Equipment CostsDocument10 pagesProperty, Plant and Equipment CostsNina MarieNo ratings yet

- HI6028 Taxation Theory, Practice & Law: T2 2018 Individual Assignment (2500 Words)Document3 pagesHI6028 Taxation Theory, Practice & Law: T2 2018 Individual Assignment (2500 Words)Aduda Ruiz BenahNo ratings yet

- Income Taxation - Rules of Income TaxDocument2 pagesIncome Taxation - Rules of Income TaxDrew BanlutaNo ratings yet

- Finals - III. Capital Assets - ProblemsDocument6 pagesFinals - III. Capital Assets - ProblemsJovince Daño DoceNo ratings yet

- Review QuestionsDocument3 pagesReview QuestionsAriaNo ratings yet

- TQ U11 DA Plant Master 2019 PDFDocument4 pagesTQ U11 DA Plant Master 2019 PDFhelenNo ratings yet

- FAC1502 Assignment 4 Semester 2 2023Document192 pagesFAC1502 Assignment 4 Semester 2 2023Haat My LaterNo ratings yet

- 3rd Year BusCom Intercompany TransactionsDocument2 pages3rd Year BusCom Intercompany TransactionsJoshua UmaliNo ratings yet

- Exam For Business TaxDocument3 pagesExam For Business TaxJenyll MabborangNo ratings yet

- Tutorial 3 - RPGT-2022Document4 pagesTutorial 3 - RPGT-2022Keat 98No ratings yet

- CGT Exam With SOlnDocument2 pagesCGT Exam With SOlnMinaykyuttNo ratings yet

- 2019 Exam QuestionDocument6 pages2019 Exam QuestionInsaaf RashidNo ratings yet

- Accumt PDFDocument3 pagesAccumt PDFFatema HossainNo ratings yet

- Canadian Income Taxation 2014 2015 Planning and Decision Making Canadian 17th Edition Buckwold Test Bank 1Document21 pagesCanadian Income Taxation 2014 2015 Planning and Decision Making Canadian 17th Edition Buckwold Test Bank 1jean100% (30)

- Canadian Income Taxation 2014 2015 Planning and Decision Making Canadian 17Th Edition Buckwold Test Bank Full Chapter PDFDocument36 pagesCanadian Income Taxation 2014 2015 Planning and Decision Making Canadian 17Th Edition Buckwold Test Bank Full Chapter PDFkenneth.cappello861100% (12)

- Activity 1b - Current LiabilitiesDocument2 pagesActivity 1b - Current LiabilitiesUchayyaNo ratings yet

- Quiz on LiabilitiesDocument5 pagesQuiz on LiabilitiesDewdrop Mae RafananNo ratings yet

- Taxation Assignment QuestionDocument7 pagesTaxation Assignment QuestionTeeraksha DoorgarpersandNo ratings yet

- 2.2. PPE IAS16 - Practice - EnglishDocument12 pages2.2. PPE IAS16 - Practice - EnglishBích TrâmNo ratings yet

- 1912 Derivatives Investment Property and Other InvestmentDocument5 pages1912 Derivatives Investment Property and Other InvestmentCykee Hanna Quizo LumongsodNo ratings yet

- PPE IllustrationsDocument3 pagesPPE Illustrationsprlu1No ratings yet

- Capital Gains Practice QuestionsDocument5 pagesCapital Gains Practice QuestionsGemeAnbew100% (2)

- Pamantasan NG Lungsod NG Marikina Auditing and Assurance Concepts & Applications On-Line Learning Mr. Nilo N. Iglesias, CPA, MBA, REA Activities For Week 1 and Week 2Document4 pagesPamantasan NG Lungsod NG Marikina Auditing and Assurance Concepts & Applications On-Line Learning Mr. Nilo N. Iglesias, CPA, MBA, REA Activities For Week 1 and Week 2suruth242No ratings yet

- Final Exam Accounting Undergraduate ProgramDocument2 pagesFinal Exam Accounting Undergraduate ProgramPutu Deny WijayaNo ratings yet

- Solution On Taxation Module 1 and 2 PDF FreeDocument9 pagesSolution On Taxation Module 1 and 2 PDF FreePauline EchanoNo ratings yet

- Acctg 205A Quiz NOV. 6,2020Document3 pagesAcctg 205A Quiz NOV. 6,2020Rheu ReyesNo ratings yet

- Solved Marin Company S General Ledger Indicates A Cash Balance of 22 340Document1 pageSolved Marin Company S General Ledger Indicates A Cash Balance of 22 340Anbu jaromiaNo ratings yet

- Homework On Current LiabilitiesDocument3 pagesHomework On Current LiabilitiesalyssaNo ratings yet

- Income Tax S5 Set IDocument5 pagesIncome Tax S5 Set ITitus ClementNo ratings yet

- Quiz Inventories and InvestmentsDocument13 pagesQuiz Inventories and InvestmentsRinconada Benori ReynalynNo ratings yet

- Faculty of Accounting and Informatics D A TDocument6 pagesFaculty of Accounting and Informatics D A TmikeNo ratings yet

- Lecture6 - RPGT Class Exercise QDocument4 pagesLecture6 - RPGT Class Exercise QpremsuwaatiiNo ratings yet

- Winston Company COGS and Accounts Payable CalculationsDocument3 pagesWinston Company COGS and Accounts Payable CalculationsRaushan ZhabaginaNo ratings yet

- Fancy Furniture Company Financial StatementsDocument2 pagesFancy Furniture Company Financial StatementsShashank GuptaNo ratings yet

- FAC1502 Assignment 4 2023Document193 pagesFAC1502 Assignment 4 2023Haat My LaterNo ratings yet

- Sabina Company Quiz #1 Questions and SolutionsDocument6 pagesSabina Company Quiz #1 Questions and SolutionsJames Daniel SwintonNo ratings yet

- Exam 1 8Document9 pagesExam 1 8Kenneth DelacruzNo ratings yet

- DBM Bom2016sdgDocument17 pagesDBM Bom2016sdgFerdie RulonaNo ratings yet

- 1.3.3 Executed Option Agreement 15072014Document97 pages1.3.3 Executed Option Agreement 15072014Jorge De Lama VargasNo ratings yet

- Air Algerie - ReservationDocument7 pagesAir Algerie - Reservationlinux satNo ratings yet

- The List of Adas and Their Respective Addresses, Telephone Numbers and Broker Codes Are As FollowsDocument22 pagesThe List of Adas and Their Respective Addresses, Telephone Numbers and Broker Codes Are As FollowsZakwan ZainalNo ratings yet

- Mobile Financial Services (MFS) Business and Regulations: Evolution in South Asian MarketsDocument26 pagesMobile Financial Services (MFS) Business and Regulations: Evolution in South Asian MarketsNishat ShimaNo ratings yet

- MCQs On BudgetingDocument2 pagesMCQs On BudgetingImtiaz BashirNo ratings yet

- Tenke Mining Corp Annual Report Highlights Exploration SuccessDocument33 pagesTenke Mining Corp Annual Report Highlights Exploration Successdely susantoNo ratings yet

- Taxation Law ProjectDocument15 pagesTaxation Law Projectraj vardhan agarwalNo ratings yet

- JURNAL Anggrenita Aulia (1810412620008) - RevisiDocument11 pagesJURNAL Anggrenita Aulia (1810412620008) - Revisipengetikan normansyahNo ratings yet

- The Role of Mining Sector in Indian EconomyDocument9 pagesThe Role of Mining Sector in Indian EconomyInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- A Simple Get Rich Quick IdeaDocument2 pagesA Simple Get Rich Quick Ideaversalas24No ratings yet

- Problem 7-1: True or False False: Fact PatternDocument23 pagesProblem 7-1: True or False False: Fact PatternMichael Brian TorresNo ratings yet

- InTech Feb2021Document46 pagesInTech Feb2021Fernando KatayamaNo ratings yet

- Risk and Return Theory - Capital MarketDocument19 pagesRisk and Return Theory - Capital Markettreasure ROTYNo ratings yet

- Acc 6 CH 01Document46 pagesAcc 6 CH 01Md. Rubel HasanNo ratings yet

- Government's MSE Development SchemeDocument8 pagesGovernment's MSE Development SchemeSanskriti sahuNo ratings yet

- This Study Resource Was: Vibhava Chemicals: Case AnalysisDocument3 pagesThis Study Resource Was: Vibhava Chemicals: Case AnalysisNidhi JoshiNo ratings yet

- Walmart's Supply Chain SuccessDocument4 pagesWalmart's Supply Chain Successmaximillan njagiNo ratings yet

- Jedec Standard: Arrowhead QADocument32 pagesJedec Standard: Arrowhead QAdaveNo ratings yet

- The Social Irresponsibility of Corporate Tax AvoidDocument9 pagesThe Social Irresponsibility of Corporate Tax Avoiddinda ardiyaniNo ratings yet

- Business Models: Dr. Megha Chauhan Symbiosis Law School, NOIDADocument29 pagesBusiness Models: Dr. Megha Chauhan Symbiosis Law School, NOIDALsen IilkhusxNo ratings yet

- Another Mega Short Squeeze On Deck - ZeroHedgeDocument5 pagesAnother Mega Short Squeeze On Deck - ZeroHedgeJonNo ratings yet

- Class 2 Indexation Module 1 Capital GainsDocument22 pagesClass 2 Indexation Module 1 Capital GainsTomy MathewNo ratings yet

- Chapter 2 Exercises-TheMarketDocument7 pagesChapter 2 Exercises-TheMarketJan Maui VasquezNo ratings yet

- Week 2 Chapter 3Document6 pagesWeek 2 Chapter 3Chipp chipNo ratings yet

- Ch.16 Dilutive Securities and Earnings Per Share: Chapter Learning ObjectivesDocument7 pagesCh.16 Dilutive Securities and Earnings Per Share: Chapter Learning ObjectivesFaishal Alghi FariNo ratings yet