You might also like

- Manage Cash Flow & Optimize Business FinancesDocument125 pagesManage Cash Flow & Optimize Business FinancesJeam Endoma-ClzNo ratings yet

- Controlling Payroll Cost - Critical Disciplines for Club ProfitabilityFrom EverandControlling Payroll Cost - Critical Disciplines for Club ProfitabilityNo ratings yet

- 1 Module 1 Working Within The Private Security Industry StudentDocument32 pages1 Module 1 Working Within The Private Security Industry StudentCelebrul DanNo ratings yet

- Value Chain Management Capability A Complete Guide - 2020 EditionFrom EverandValue Chain Management Capability A Complete Guide - 2020 EditionNo ratings yet

- M&E One and A Half ModuleDocument197 pagesM&E One and A Half ModuleAnanya GowdaNo ratings yet

- Primary Role of Company AuditorDocument5 pagesPrimary Role of Company AuditorAshutosh GoelNo ratings yet

- Pricing Policies: B) External FactorsDocument10 pagesPricing Policies: B) External FactorspRiNcE DuDhAtRaNo ratings yet

- Code of Ethics for AFP MembersDocument32 pagesCode of Ethics for AFP Membersאנג' ליקהNo ratings yet

- COA Audit Finds Deficiencies in Collections of Bongabon Liga ng mga Barangay FundsDocument6 pagesCOA Audit Finds Deficiencies in Collections of Bongabon Liga ng mga Barangay FundsJonson PalmaresNo ratings yet

- Cash FlowDocument12 pagesCash FlowDivesh BabariaNo ratings yet

- Lesson 1213 FinaleDocument89 pagesLesson 1213 FinaleMelitte BalitaNo ratings yet

- Cash Budget Definition GuideDocument4 pagesCash Budget Definition GuideSaloni JainNo ratings yet

- Cashbook SampleDocument15 pagesCashbook Samplemaneesh_nayak3No ratings yet

- TOPIC 3d - Audit PlanningDocument29 pagesTOPIC 3d - Audit PlanningLANGITBIRUNo ratings yet

- As-1 Disclosure of Accounting PoliciesDocument7 pagesAs-1 Disclosure of Accounting PoliciesPrakash_Tandon_583No ratings yet

- Week 1 Conceptual Framework For Financial ReportingDocument17 pagesWeek 1 Conceptual Framework For Financial ReportingSHANE NAVARRONo ratings yet

- Cash and Marketable Securities ManagementDocument17 pagesCash and Marketable Securities Managementshrutimathur14891802100% (13)

- Accounting basicsDocument24 pagesAccounting basicsRoshan JhaNo ratings yet

- Note 08Document6 pagesNote 08Tharaka IndunilNo ratings yet

- Fundamentals OF Accounting: Accounting by Meigs, Williams, Haka, BettnerDocument64 pagesFundamentals OF Accounting: Accounting by Meigs, Williams, Haka, BettnerAliya SaeedNo ratings yet

- Module 1Document18 pagesModule 1Rizwana BaigNo ratings yet

- Basics of Accounting and BusinessDocument13 pagesBasics of Accounting and Businessayitenew temesgenNo ratings yet

- Development of Credit and Collection Policy PDFDocument35 pagesDevelopment of Credit and Collection Policy PDFJimuel Faigao100% (1)

- Underwriting of SecuritiesDocument20 pagesUnderwriting of Securitiesrahul0105100% (1)

- Financial Management PDFDocument132 pagesFinancial Management PDFsumit mishraNo ratings yet

- How To Invest in Philippine Stock Market PDFDocument8 pagesHow To Invest in Philippine Stock Market PDFEduardo SantosNo ratings yet

- Debt management ratios analysisDocument4 pagesDebt management ratios analysisJohn MuemaNo ratings yet

- Nigeria Sas 10 and New Prudential Guidelines PDFDocument21 pagesNigeria Sas 10 and New Prudential Guidelines PDFiranadeNo ratings yet

- JBC Travel and ToursDocument15 pagesJBC Travel and ToursArshier Ching0% (1)

- Consolidated Financial Statements ExplainedDocument77 pagesConsolidated Financial Statements ExplainedMisganaw DebasNo ratings yet

- CBM Guideline On Risk Management Practices of Banks Website EngDocument53 pagesCBM Guideline On Risk Management Practices of Banks Website EngRoger100% (1)

- Financial Planning Guide for Small BusinessesDocument23 pagesFinancial Planning Guide for Small BusinessesHassan JulkipliNo ratings yet

- FINANCIAL PLANNING & FORECASTINGDocument25 pagesFINANCIAL PLANNING & FORECASTINGCathy TumbaliNo ratings yet

- G&A Expenses ExamplesDocument6 pagesG&A Expenses ExamplesmaresNo ratings yet

- New Edited Cash ManagementDocument59 pagesNew Edited Cash Managementdominic wurdaNo ratings yet

- Financial Accounting and Reporting 02Document6 pagesFinancial Accounting and Reporting 02Nuah SilvestreNo ratings yet

- Chapter 3 Financial Statement Taxes and CashflowDocument33 pagesChapter 3 Financial Statement Taxes and CashflowlovejkbsNo ratings yet

- The Balanced Scorecard: A Tool To Implement StrategyDocument39 pagesThe Balanced Scorecard: A Tool To Implement StrategyAilene QuintoNo ratings yet

- Answer To Chapter 5 - Introduction To Ethics PDFDocument1 pageAnswer To Chapter 5 - Introduction To Ethics PDFFaith MarasiganNo ratings yet

- Banking Diploma Bangladesh Law Short NotesDocument19 pagesBanking Diploma Bangladesh Law Short NotesNiladri HasanNo ratings yet

- Central Bank Functions and ResponsibilitiesDocument16 pagesCentral Bank Functions and ResponsibilitiesAyesha Parvin RubyNo ratings yet

- Comp Audit Lesson 1 Ethics Fraud and Internal ControlDocument62 pagesComp Audit Lesson 1 Ethics Fraud and Internal ControlAnthony FloresNo ratings yet

- Governance Standards For SACCOsDocument16 pagesGovernance Standards For SACCOsKivumbi William100% (1)

- CH 03Document29 pagesCH 03S M Saad SaleemNo ratings yet

- Ch-5 Cash Flow AnalysisDocument9 pagesCh-5 Cash Flow AnalysisQiqi GenshinNo ratings yet

- Financial Management Lesson No. 1Document4 pagesFinancial Management Lesson No. 1Geraldine MayoNo ratings yet

- Accounting For Public Sector and Civil Society 2022 LatestDocument170 pagesAccounting For Public Sector and Civil Society 2022 LatestZerai Hagos HailemariamNo ratings yet

- Raising Capital: A Survey of Non-Bank Sources of CapitalDocument34 pagesRaising Capital: A Survey of Non-Bank Sources of CapitalRoy Joshua100% (1)

- Report of Independent AuditorDocument3 pagesReport of Independent Auditorben yiNo ratings yet

- Audit of Forex TransactionsDocument4 pagesAudit of Forex Transactionsnamcheang100% (2)

- Fund ManagementDocument47 pagesFund Managementjanine mujeNo ratings yet

- Working CapitalDocument39 pagesWorking CapitalHema LathaNo ratings yet

- Financial Statement Analysis MethodsDocument5 pagesFinancial Statement Analysis MethodsShaheen MahmudNo ratings yet

- Public Sector Accounting Homework SolutionsDocument6 pagesPublic Sector Accounting Homework SolutionsLoganPearcyNo ratings yet

- Financial Statements and Performance Analysis: DR Leslie Mitchell Financial ControlDocument31 pagesFinancial Statements and Performance Analysis: DR Leslie Mitchell Financial Controlosaleemi100% (1)

- Accounting adjustments and financial statementsDocument12 pagesAccounting adjustments and financial statementsKwaku DanielNo ratings yet

- Sources and Utilization of Funds of OSCBDocument12 pagesSources and Utilization of Funds of OSCBpapa1988No ratings yet

- Marcelo Transport Services Income Statement and Balance SheetDocument3 pagesMarcelo Transport Services Income Statement and Balance SheetPaulene Abegail MatiasNo ratings yet

- Marketing PricingDocument38 pagesMarketing Pricingrishabh jainNo ratings yet

- 013 - Forex & NPO-1-39Document153 pages013 - Forex & NPO-1-39Mae Flor Cuya GabasNo ratings yet

- AnswerQuiz - Module 10Document4 pagesAnswerQuiz - Module 10Alyanna Alcantara100% (1)

- Acctg 9a Midterm Exam CH 9 15 CabreraDocument4 pagesAcctg 9a Midterm Exam CH 9 15 CabreraDonalyn BannagaoNo ratings yet

- Additional Solved Problems Vit 2011Document104 pagesAdditional Solved Problems Vit 2011Vinait ThoratNo ratings yet

- Model Paper, Accountancy, XIDocument13 pagesModel Paper, Accountancy, XIanyaNo ratings yet

- Businessfinance12 q3 Mod1.1 Introduction To Financial ManagementDocument20 pagesBusinessfinance12 q3 Mod1.1 Introduction To Financial ManagementAsset Dy92% (13)

- Refund of Franking Credits Instructions and Application For IndividualsDocument16 pagesRefund of Franking Credits Instructions and Application For Individualsuly01 cubillaNo ratings yet

- Financial Management Assignment BreakdownDocument22 pagesFinancial Management Assignment BreakdownSimran VirmaniNo ratings yet

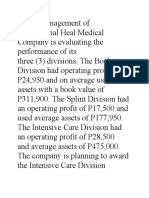

- International Heal Medical evaluates divisions' performanceDocument6 pagesInternational Heal Medical evaluates divisions' performanceGillai Marie IbardolazaNo ratings yet

- Exercise 7 (Finding Unknown Balances)Document13 pagesExercise 7 (Finding Unknown Balances)Jane VillanuevaNo ratings yet

- 19Document50 pages19Ahmed El KhateebNo ratings yet

- Capital Budget - Summary Notes and QuestionsDocument22 pagesCapital Budget - Summary Notes and QuestionsClaudine ReidNo ratings yet

- The Cpa Licensure Examination SyllabusDocument46 pagesThe Cpa Licensure Examination Syllabusi hate youtubersNo ratings yet

- Allied Food Products' 2015 Statement of Comprehensive Income and Financial PositionDocument4 pagesAllied Food Products' 2015 Statement of Comprehensive Income and Financial PositionGlizette SamaniegoNo ratings yet

- Ind AS 105Document28 pagesInd AS 105stephanie baliwerti0% (1)

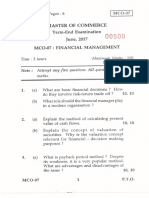

- MCO-7 June17Document6 pagesMCO-7 June17BinayKPNo ratings yet

- Dividend: Week 11 Company LawDocument11 pagesDividend: Week 11 Company Lawbazil khanNo ratings yet

- Mfa Test 1Document4 pagesMfa Test 1Shantanu PorelNo ratings yet

- Mobile:: Indranil Ghosh (Pan: Afupg6596C) DSP BLACKROCK - EQUITY REG FUND (D) - Folio No: 2182999/55Document6 pagesMobile:: Indranil Ghosh (Pan: Afupg6596C) DSP BLACKROCK - EQUITY REG FUND (D) - Folio No: 2182999/55IndranilGhoshNo ratings yet

- 5 Year Financial PlanDocument26 pages5 Year Financial PlanNaimul KaderNo ratings yet

- Intacc 3Document102 pagesIntacc 3sofiaNo ratings yet

- Capital Structure DecisionDocument10 pagesCapital Structure DecisionMunni FoyshalNo ratings yet

- Texto en Ingles Finanzas CorporativasDocument2 pagesTexto en Ingles Finanzas CorporativasyercaNo ratings yet

- Chapter-4 Business Acquisition & FranchaisingDocument35 pagesChapter-4 Business Acquisition & FranchaisingLowzil Rayan AranhaNo ratings yet

- Ifrs Edition: Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeDocument29 pagesIfrs Edition: Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeBafesh RoyNo ratings yet

- Introduction to financial managementDocument37 pagesIntroduction to financial managementBritney BowersNo ratings yet

- Webinar Manajemen Keuangan PerusahaanDocument69 pagesWebinar Manajemen Keuangan PerusahaanDias CandrikaNo ratings yet

- Literature Review On Ratio AnalysisDocument8 pagesLiterature Review On Ratio Analysisgw2wr9ss100% (1)

- A. Intax NotesDocument13 pagesA. Intax NotesIssy BNo ratings yet

- Chapter 14 - Cash Flow Statement MCQDocument2 pagesChapter 14 - Cash Flow Statement MCQfrieda20093835100% (3)