You might also like

- File by Mail Instructions For Your Federal Amended Tax ReturnDocument14 pagesFile by Mail Instructions For Your Federal Amended Tax ReturnRyan MayleNo ratings yet

- Project Finance Solar PV ModelDocument81 pagesProject Finance Solar PV ModelSaurabh SharmaNo ratings yet

- Corporation TRAIN and CREATE LawDocument8 pagesCorporation TRAIN and CREATE LawdgdeguzmanNo ratings yet

- INCOME TAX UpdatedDocument94 pagesINCOME TAX UpdatedTrishNo ratings yet

- RR 5-2021Document22 pagesRR 5-2021zelayneNo ratings yet

- Claim Child Benefit - GOV - UkDocument6 pagesClaim Child Benefit - GOV - UkMaya Julieta Catacutan-EstabilloNo ratings yet

- MAS 12 Working Capital Management MAS 12 Working Capital ManagementDocument11 pagesMAS 12 Working Capital Management MAS 12 Working Capital ManagementiBEAYNo ratings yet

- CPAR Income Tax of Corporations (Batch 93) - HandoutDocument41 pagesCPAR Income Tax of Corporations (Batch 93) - HandoutJuan Miguel UngsodNo ratings yet

- 3rd VidDocument27 pages3rd VidStephanie LeeNo ratings yet

- Income and Business TaxationDocument1 pageIncome and Business TaxationTomo Euryl San JuanNo ratings yet

- 2 Create RR 5-2021 - IT - FullDocument51 pages2 Create RR 5-2021 - IT - FullTreb LemNo ratings yet

- Corporate Income TaxationDocument43 pagesCorporate Income TaxationRose May AdanNo ratings yet

- Applied Econ2 Exam 2019Document4 pagesApplied Econ2 Exam 2019Ernalyn PelpinosasNo ratings yet

- Tax 304 - Vat Compliance RequirementsDocument5 pagesTax 304 - Vat Compliance RequirementsiBEAYNo ratings yet

- Reviewer in Taxation LawDocument20 pagesReviewer in Taxation LawDred OpleNo ratings yet

- Module 4 .1 - Schedule of Withholding TaxesDocument2 pagesModule 4 .1 - Schedule of Withholding Taxeskrisha milloNo ratings yet

- Summary of The Important Provisions of CREATE Act in The PhilippinesDocument10 pagesSummary of The Important Provisions of CREATE Act in The Philippinesrichard emersonNo ratings yet

- Manila Cavite Laguna Cebu Cagayan de Oro DavaoDocument3 pagesManila Cavite Laguna Cebu Cagayan de Oro DavaoTatianaNo ratings yet

- RR No. 5 - 2021 - MANA, Karen Mariz B.Document4 pagesRR No. 5 - 2021 - MANA, Karen Mariz B.karen mariz manaNo ratings yet

- Taxes in A Nutshell 2021: For Estonia, Latvia, Lithuania and BelarusDocument19 pagesTaxes in A Nutshell 2021: For Estonia, Latvia, Lithuania and BelarusRegita Kusumaning PutriNo ratings yet

- CPAR Tax On Corporations (Batch 89) - HandoutDocument28 pagesCPAR Tax On Corporations (Batch 89) - HandoutMark LapidNo ratings yet

- TCS Rate Chart For AY 2020-21 and AY 2021-22Document9 pagesTCS Rate Chart For AY 2020-21 and AY 2021-22maksuhailNo ratings yet

- (Year) : Amendments Vide Finance Act, 2010 On "Direct Tax"Document16 pages(Year) : Amendments Vide Finance Act, 2010 On "Direct Tax"peyala_sudhirNo ratings yet

- Nepal Income Tax Slab Rates For FY 2077-78 B.S. (2020-21)Document7 pagesNepal Income Tax Slab Rates For FY 2077-78 B.S. (2020-21)Sajjal GhimireNo ratings yet

- Manila Cavite Laguna Cebu Cagayan de Oro DavaoDocument2 pagesManila Cavite Laguna Cebu Cagayan de Oro DavaoRaymond RosalesNo ratings yet

- Bangladesh Budget Review FY23Document12 pagesBangladesh Budget Review FY23Tariq HussainNo ratings yet

- Tax Updates Under CREATE LawDocument4 pagesTax Updates Under CREATE LawSandy ArticaNo ratings yet

- Group 1 Create LawDocument38 pagesGroup 1 Create LawKrizah Marie CaballeroNo ratings yet

- TX VNM Tax Rates 2023 - 230507 - 072553Document4 pagesTX VNM Tax Rates 2023 - 230507 - 072553Nguyễn Hồng NgọcNo ratings yet

- Tax TableDocument3 pagesTax TablePhán Tiêu TiềnNo ratings yet

- CREATE ManualDocument98 pagesCREATE ManualGenny JovellanosNo ratings yet

- 23 q3 Presentation Deck American TowerDocument23 pages23 q3 Presentation Deck American TowerDaniel KwanNo ratings yet

- Schedule of Withholding TaxDocument2 pagesSchedule of Withholding TaxLance MontealtoNo ratings yet

- WithholdingRatesCards 2022-2023Document17 pagesWithholdingRatesCards 2022-2023ausafhaider5345No ratings yet

- Create RatesDocument1 pageCreate RatesRen Mar CruzNo ratings yet

- Botswana Budget 2023 24Document12 pagesBotswana Budget 2023 24PHENYONo ratings yet

- Corporate Income TaxDocument34 pagesCorporate Income TaxKimberly ToraldeNo ratings yet

- Debt ProposalsDocument17 pagesDebt ProposalsRoberto DistrilonNo ratings yet

- O Uco Bank: Rnictj/Date: 19.08.2019Document3 pagesO Uco Bank: Rnictj/Date: 19.08.2019Satya KarNo ratings yet

- RR No. 5-2021Document7 pagesRR No. 5-2021Scion RaguindinNo ratings yet

- Getco IncDocument1 pageGetco IncDhruv ShahNo ratings yet

- TAX-702 (Tax Rates For Corporations)Document7 pagesTAX-702 (Tax Rates For Corporations)MABI ESPENIDONo ratings yet

- Salient Proposed Changes To Tax Regulations in Bangladesh For FY 2021-22Document19 pagesSalient Proposed Changes To Tax Regulations in Bangladesh For FY 2021-22ahme farNo ratings yet

- Summary of Changes Under The RA 11534 (CREATE ACT) Atty. Mark Anthony P. TamayoDocument6 pagesSummary of Changes Under The RA 11534 (CREATE ACT) Atty. Mark Anthony P. TamayoNievelita OdasanNo ratings yet

- CRISIL Fund Insights Feb2020Document4 pagesCRISIL Fund Insights Feb2020Rahul SharmaNo ratings yet

- Indonesia: The Delta Variant and Lagging Vaccination Have Set Back The RecoveryDocument4 pagesIndonesia: The Delta Variant and Lagging Vaccination Have Set Back The RecoveryTopan ArdiansyahNo ratings yet

- TAX 702 - Income Tax Rates CorporationsDocument6 pagesTAX 702 - Income Tax Rates CorporationsJuan Miguel UngsodNo ratings yet

- Regular Business/Corporate Tax: DC RFC NRFCDocument2 pagesRegular Business/Corporate Tax: DC RFC NRFCGrace Angelie C. Asio-SalihNo ratings yet

- Taxation-2 2Document5 pagesTaxation-2 2Yeshua Liebt PhoenixNo ratings yet

- PWC Proposed Changes - Inland Revenue (Amendment) BillDocument12 pagesPWC Proposed Changes - Inland Revenue (Amendment) BillThiruNo ratings yet

- TX ZWE Examinable Documents 2021Document3 pagesTX ZWE Examinable Documents 2021Tawanda Tatenda HerbertNo ratings yet

- Union BudgetDocument9 pagesUnion BudgetUnicorn SpiderNo ratings yet

- Nepal Income Tax Slab Rates 2077-78 (2020-21), Provisions and Concessions For IndividualsDocument7 pagesNepal Income Tax Slab Rates 2077-78 (2020-21), Provisions and Concessions For IndividualsSajjal GhimireNo ratings yet

- Final Taxes RatesDocument2 pagesFinal Taxes RatesPanda CocoNo ratings yet

- Union Budget FY 12Document36 pagesUnion Budget FY 12Yahya AzharNo ratings yet

- 2020 Consolidated Audit Report On ODA Programs and ProjectsDocument76 pages2020 Consolidated Audit Report On ODA Programs and Projectsjohn uyNo ratings yet

- CREATE LAW - Short IntroDocument3 pagesCREATE LAW - Short IntroBenjie DavilaNo ratings yet

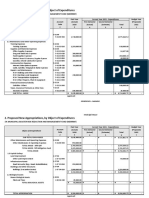

- Proposed New Appropriations, by Object of ExpendituresDocument2 pagesProposed New Appropriations, by Object of ExpendituresVIRGILIO OCOY III100% (1)

- De La Sol - Sales Program - 01.04.2023. ENGDocument2 pagesDe La Sol - Sales Program - 01.04.2023. ENGQuang Hưng VũNo ratings yet

- CREATE Features 26nov20Document14 pagesCREATE Features 26nov20Denzel Edward CariagaNo ratings yet

- Ultratech Cement Limited: Outlook Remains ChallengingDocument5 pagesUltratech Cement Limited: Outlook Remains ChallengingamitNo ratings yet

- 94-03 Corporate Income Tax - HandoutDocument43 pages94-03 Corporate Income Tax - HandoutSilver LilyNo ratings yet

- Trabaho CTRP Package 2Document48 pagesTrabaho CTRP Package 2ttunacaoNo ratings yet

- Trabaho CTRP Package 2Document48 pagesTrabaho CTRP Package 2ttunacaoNo ratings yet

- 2023-24 - Indirect Tax DossierDocument3 pages2023-24 - Indirect Tax DossierCA Manish BasnetNo ratings yet

- Overcoming COVID-19 in Bhutan: Lessons from Coping with the Pandemic in a Tourism-Dependent EconomyFrom EverandOvercoming COVID-19 in Bhutan: Lessons from Coping with the Pandemic in a Tourism-Dependent EconomyNo ratings yet

- Budget Rigidity in Latin America and the Caribbean: Causes, Consequences, and Policy ImplicationsFrom EverandBudget Rigidity in Latin America and the Caribbean: Causes, Consequences, and Policy ImplicationsNo ratings yet

- A New Dawn for Global Value Chain Participation in the PhilippinesFrom EverandA New Dawn for Global Value Chain Participation in the PhilippinesNo ratings yet

- VAT NotesDocument21 pagesVAT NotesiBEAYNo ratings yet

- Tax 302 - Vat-Exempt TransactionsDocument6 pagesTax 302 - Vat-Exempt TransactionsiBEAYNo ratings yet

- Tax 303 - Input VatDocument7 pagesTax 303 - Input VatiBEAYNo ratings yet

- B.A. II Year Economics Sem - III & IV Syllabus PDFDocument15 pagesB.A. II Year Economics Sem - III & IV Syllabus PDFAnkit s50% (2)

- RD 108Document4 pagesRD 108evboatNo ratings yet

- How To Complete The Tax Declaration With The French Tax Office (Officials)Document5 pagesHow To Complete The Tax Declaration With The French Tax Office (Officials)ChrisNo ratings yet

- 2022 BIR Form 2316 - 2013650Document1 page2022 BIR Form 2316 - 2013650erik skiNo ratings yet

- GSTR3B 09humps0863q1zf 072023Document3 pagesGSTR3B 09humps0863q1zf 072023mahtab begNo ratings yet

- Taxation in Fiscal Ad and Other IssuesDocument20 pagesTaxation in Fiscal Ad and Other IssuesJessica Villanueva GrifaldoNo ratings yet

- ACC497 Ltweek 4 AssignmentDocument4 pagesACC497 Ltweek 4 AssignmentRobbie WolfNo ratings yet

- PWC Worldwide Tax Summaries Corporate Taxes 2017 18 PDFDocument2,725 pagesPWC Worldwide Tax Summaries Corporate Taxes 2017 18 PDFErika delos SantosNo ratings yet

- NJ 165Document1 pageNJ 165Vikram rajputNo ratings yet

- Situs of TaxationDocument1 pageSitus of TaxationDanica Christele AlfaroNo ratings yet

- Tax-planning-And-management Solved MCQs (Set-3)Document8 pagesTax-planning-And-management Solved MCQs (Set-3)Umair VirkNo ratings yet

- PKF WWTG 2020 2021 OnlineDocument1,207 pagesPKF WWTG 2020 2021 OnlineHussain MunshiNo ratings yet

- DELOS SANTOS Quiz 002 Classification of TaxpayersDocument2 pagesDELOS SANTOS Quiz 002 Classification of TaxpayersCarl Emerson GalaboNo ratings yet

- Quiz 4 6 CompilationDocument8 pagesQuiz 4 6 CompilationShelleyNo ratings yet

- Train 2 or Trabaho Bill: (Tax Reform For Attracting Better and High-Quality Opportunities) House Bill No. 8083Document30 pagesTrain 2 or Trabaho Bill: (Tax Reform For Attracting Better and High-Quality Opportunities) House Bill No. 8083Azaria MatiasNo ratings yet

- Tax 56 Activity 2Document2 pagesTax 56 Activity 2Hannah Alvarado BandolaNo ratings yet

- Lahore Cantt Property TAX FORMULADocument7 pagesLahore Cantt Property TAX FORMULAMusa pak ShaheedNo ratings yet

- Xi Wei Answer SheetDocument3 pagesXi Wei Answer Sheetapi-415645328No ratings yet

- Pajak Internasional Seminar PerpajakanDocument35 pagesPajak Internasional Seminar Perpajakantoton akNo ratings yet

- Hassan KAsi-1-1Document1 pageHassan KAsi-1-1afzalkasisimliNo ratings yet

- 2018 Tax CalculatorDocument45 pages2018 Tax Calculatoracctg2012No ratings yet

- Tax On Individuals: Non-Resident Individual CitizenDocument3 pagesTax On Individuals: Non-Resident Individual CitizenJan Aguilar EstefaniNo ratings yet

- Accounting TaxationDocument2 pagesAccounting TaxationAia Sophia SindacNo ratings yet

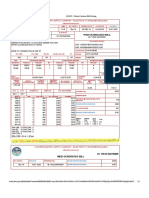

- LESCO - Online Customer Bill Printing PDFDocument1 pageLESCO - Online Customer Bill Printing PDFGulshion Malik100% (1)