You might also like

- Solar Photovoltaic Technology Production: Potential Environmental Impacts and Implications for GovernanceFrom EverandSolar Photovoltaic Technology Production: Potential Environmental Impacts and Implications for GovernanceNo ratings yet

- 1 s2.0 S0360544219300702 Main PDFDocument19 pages1 s2.0 S0360544219300702 Main PDFnaveedNo ratings yet

- Impact of Optimal Energy Mix On Environmental Quality in NigeriaDocument7 pagesImpact of Optimal Energy Mix On Environmental Quality in NigeriaIJAR JOURNALNo ratings yet

- Science of The Total Environment: Baris Memduh Eren, Nigar Taspinar, Korhan K. GokmenogluDocument9 pagesScience of The Total Environment: Baris Memduh Eren, Nigar Taspinar, Korhan K. GokmenogluIntan Dana LestariNo ratings yet

- Household Energy Conservation Patterns: Evidence From GreeceDocument26 pagesHousehold Energy Conservation Patterns: Evidence From GreeceGiorgos PardalisNo ratings yet

- Energie RegenerabilăDocument18 pagesEnergie RegenerabilăDream highNo ratings yet

- 7 Apergis - N - Payne - E - J - Menyah - K - and - Wolde-Rufael - Y - On - The - Causal - Dynamics - Between - Emissions-With-Cover-Page-V2 APERGISDocument7 pages7 Apergis - N - Payne - E - J - Menyah - K - and - Wolde-Rufael - Y - On - The - Causal - Dynamics - Between - Emissions-With-Cover-Page-V2 APERGISjulio CmNo ratings yet

- Ecological Economics: Nicholas Apergis, James E. Payne, Kojo Menyah, Yemane Wolde-RufaelDocument6 pagesEcological Economics: Nicholas Apergis, James E. Payne, Kojo Menyah, Yemane Wolde-RufaelMuhammed ÇiloğluNo ratings yet

- 18Document13 pages18driftkingfighterNo ratings yet

- 4 Sadorsky-2009-RenewableenergyconsumptionCO2emissionsandoiDocument8 pages4 Sadorsky-2009-RenewableenergyconsumptionCO2emissionsandoijulio CmNo ratings yet

- 3.can Circular Bioeconomy Be Fueled by Waste Biorefineries - A Closer LookDocument11 pages3.can Circular Bioeconomy Be Fueled by Waste Biorefineries - A Closer LookGhochapon MongkhonsiriNo ratings yet

- Energy Vision 2013: Energy Transitions: Past and FutureDocument52 pagesEnergy Vision 2013: Energy Transitions: Past and FutureJesus Black MillmanNo ratings yet

- 1 s2.0 S2405844023060905 MainDocument13 pages1 s2.0 S2405844023060905 MainFahrizal TaufiqqurrachmanNo ratings yet

- Potential Biofuels From 1-4genDocument20 pagesPotential Biofuels From 1-4genjitendra sainiNo ratings yet

- Gyamfi 2021Document12 pagesGyamfi 2021Minh Tiến LêNo ratings yet

- Green EnergiesDocument11 pagesGreen EnergiesLucia VeraNo ratings yet

- Moments-Based Quantile Regression (QRG)Document8 pagesMoments-Based Quantile Regression (QRG)Mushtaq HussainNo ratings yet

- Journal of Environmental ManagementDocument17 pagesJournal of Environmental ManagementSurahmanNo ratings yet

- 1 s2.0 S0301479723004322 MainDocument17 pages1 s2.0 S0301479723004322 MainDiana CortejasNo ratings yet

- ARDLboundtest FormDocument11 pagesARDLboundtest FormCao Nữ Thùy TrangNo ratings yet

- Green EnergyDocument16 pagesGreen EnergyMUHAMMAD MUSTAFANo ratings yet

- Mitigating Emissions in India: Accounting For The Role of Real Income, Renewable Energy Consumption and Investment in EnergyDocument6 pagesMitigating Emissions in India: Accounting For The Role of Real Income, Renewable Energy Consumption and Investment in EnergySyipa YuliaNo ratings yet

- 0908 IEA Bioenergy - Bioenergy - A Sustainable and Reliable Energy Source ExSumDocument12 pages0908 IEA Bioenergy - Bioenergy - A Sustainable and Reliable Energy Source ExSumRahul RaviNo ratings yet

- (Harrie Knoef) Handbook Biomass Gasification PDFDocument12 pages(Harrie Knoef) Handbook Biomass Gasification PDFdfiorilloNo ratings yet

- Fünfgeld - 2018 - Analysen44 - Fossil - Fuels Justice PDFDocument26 pagesFünfgeld - 2018 - Analysen44 - Fossil - Fuels Justice PDFJezaabelleNo ratings yet

- Ecological Economics: Karolina SafarzynskaDocument10 pagesEcological Economics: Karolina SafarzynskaWilliams CastilloNo ratings yet

- Renewable Energy and Macroeconomic Efficiency of OECD and non-OECD EconomiesDocument10 pagesRenewable Energy and Macroeconomic Efficiency of OECD and non-OECD EconomiesStefan GrigoreanNo ratings yet

- Renewable and Nonrenewable Energy Consumption, Economic Growth, and Emissions: International EvidenceDocument21 pagesRenewable and Nonrenewable Energy Consumption, Economic Growth, and Emissions: International EvidenceElin von PostNo ratings yet

- Xiong 2021Document8 pagesXiong 2021NitishNo ratings yet

- MPRA Paper 97369Document19 pagesMPRA Paper 97369Ahmad IluNo ratings yet

- Advances in Green Economy and Sustainability: Introduction: April 2018Document21 pagesAdvances in Green Economy and Sustainability: Introduction: April 2018Alifanda CahyanantoNo ratings yet

- EU Bioeconomy Policy and Market AnalysisDocument32 pagesEU Bioeconomy Policy and Market AnalysisSergio ArangoNo ratings yet

- EthiopianenergyDocument13 pagesEthiopianenergyLeta NegasaNo ratings yet

- The Global Scenario of Biofuel Production and DevelopmentDocument29 pagesThe Global Scenario of Biofuel Production and DevelopmentabhirajNo ratings yet

- SawyerrOkudoh2019 IntJEnergyEconPolicyDocument13 pagesSawyerrOkudoh2019 IntJEnergyEconPolicyHj JayatheerthaNo ratings yet

- Tecnología Verde para La Producción Sostenible de Biohidrógeno (Waste To Energy) Una RevisiónDocument13 pagesTecnología Verde para La Producción Sostenible de Biohidrógeno (Waste To Energy) Una RevisiónKathiza Annais MadueñoNo ratings yet

- Fuel Processing Technology: Priyabrata Pradhan, Sanjay M. Mahajani, Amit Arora TDocument18 pagesFuel Processing Technology: Priyabrata Pradhan, Sanjay M. Mahajani, Amit Arora Titalo mayuber mendoza velezNo ratings yet

- Canada GHG Vs GDPDocument7 pagesCanada GHG Vs GDPMinh Tiến LêNo ratings yet

- IGC Energy and Environment Evidence Paper 3003Document60 pagesIGC Energy and Environment Evidence Paper 3003YaminNo ratings yet

- 01 - Dynamic Correlations and Volatility Spillovers Between Subsectoral - 2023 - CoskunDocument23 pages01 - Dynamic Correlations and Volatility Spillovers Between Subsectoral - 2023 - CoskunSoleiman HashemiNo ratings yet

- Review On Sustainable Energy PotentialDocument10 pagesReview On Sustainable Energy PotentialIOSRjournalNo ratings yet

- Energy Reports: Sher Khan, Zhuangzhuang Peng, Yongdong LiDocument14 pagesEnergy Reports: Sher Khan, Zhuangzhuang Peng, Yongdong LiCristian BarrosNo ratings yet

- Applied Energy: Dilip Khatiwada, Bharadwaj K. Venkata, Semida Silveira, Francis X. JohnsonDocument13 pagesApplied Energy: Dilip Khatiwada, Bharadwaj K. Venkata, Semida Silveira, Francis X. JohnsonAdemar EstradaNo ratings yet

- The Importance of Renewable Energy Consumption and FDI Inflows inDocument15 pagesThe Importance of Renewable Energy Consumption and FDI Inflows intran phankNo ratings yet

- Bio-Engineering For Pollution Prevention Through Development Ofbioenergy ManagementDocument24 pagesBio-Engineering For Pollution Prevention Through Development Ofbioenergy ManagementChief editorNo ratings yet

- Biomass. Incineration, Pyrolysis, Combustion and GasificationDocument13 pagesBiomass. Incineration, Pyrolysis, Combustion and GasificationSaifAdamz's100% (1)

- Scin-100 Current Event Essay Renewable and Non-Renewable Energy SourceDocument11 pagesScin-100 Current Event Essay Renewable and Non-Renewable Energy Sourceapi-525959070No ratings yet

- Renewable Energy Global ChallengesDocument9 pagesRenewable Energy Global ChallengesDanylo NosovNo ratings yet

- Global Energy Crisis: Impact On The Global Economy: SSRN Electronic Journal December 2022Document19 pagesGlobal Energy Crisis: Impact On The Global Economy: SSRN Electronic Journal December 2022Muhammad Adnan KhanNo ratings yet

- Sed Energy Eco Pop FdiDocument10 pagesSed Energy Eco Pop FdinhoctydangtapdiNo ratings yet

- Does Economic Growth Promote Electric Power Consumption - Implications For Electricity Conservation, Expansive, and Security PoliciesDocument14 pagesDoes Economic Growth Promote Electric Power Consumption - Implications For Electricity Conservation, Expansive, and Security PolicieszerolaahmNo ratings yet

- Science of The Total Environment: Chi-Wei Su Muhammad Umar Zeeshan KhanDocument12 pagesScience of The Total Environment: Chi-Wei Su Muhammad Umar Zeeshan KhanAlso FísicaNo ratings yet

- Competitive AdvantageDocument25 pagesCompetitive AdvantageHosamAhmadNo ratings yet

- Energy Conservation Measures in NigeriaDocument13 pagesEnergy Conservation Measures in NigeriaNaMatazuNo ratings yet

- Int. J. Production Economics: David Correll, Yoshinori Suzuki, Bobby MartensDocument8 pagesInt. J. Production Economics: David Correll, Yoshinori Suzuki, Bobby MartensguicqpNo ratings yet

- Opportunities and Challenges of Hydrogen as an Alternative Transport FuelDocument14 pagesOpportunities and Challenges of Hydrogen as an Alternative Transport FuelDavid Fernando Otalvaro ZuletaNo ratings yet

- Temti Ep 01 2015Document14 pagesTemti Ep 01 2015callisto69No ratings yet

- Energy Sustainability With A Focus On Environmentsl PerspectiveDocument14 pagesEnergy Sustainability With A Focus On Environmentsl PerspectiveEbenezer ButarbutarNo ratings yet

- Articulo Sobre Determinantes Co2 ArgentinaDocument14 pagesArticulo Sobre Determinantes Co2 ArgentinaGerman MercadoNo ratings yet

- 2015 Book EnergyEfficiency Introduction SpringerDocument200 pages2015 Book EnergyEfficiency Introduction SpringerManuelCipagautaZ100% (1)

- The Long Run Relationship Between Energy Consumption, Oil Prices, and Carbon Dioxide Emissions in European CountriesDocument14 pagesThe Long Run Relationship Between Energy Consumption, Oil Prices, and Carbon Dioxide Emissions in European CountriesSunil KhoslaNo ratings yet

- Energy Policy: Muhammad Shahbaz, Suleman Sarwar, Wei Chen, Muhammad Nasir MalikDocument15 pagesEnergy Policy: Muhammad Shahbaz, Suleman Sarwar, Wei Chen, Muhammad Nasir MalikSunil KhoslaNo ratings yet

- Cuadernos de Economía: Impact of Oil Prices, Energy Consumption and Economic Growth On The Inflation Rate in MalaysiaDocument8 pagesCuadernos de Economía: Impact of Oil Prices, Energy Consumption and Economic Growth On The Inflation Rate in MalaysiaSunil KhoslaNo ratings yet

- 1 s2.0 S2666154322000382 Main3Document15 pages1 s2.0 S2666154322000382 Main3Sunil KhoslaNo ratings yet

- 2022 Belloetal YIAP VULDocument15 pages2022 Belloetal YIAP VULSunil KhoslaNo ratings yet

- 10 1108 - Jed 10 2022 0199Document21 pages10 1108 - Jed 10 2022 0199Sunil KhoslaNo ratings yet

- JOURNAL OF AGRICULTURE FOOD SCIENCES 229463-ArticleText-557556-1-10-20220809Document12 pagesJOURNAL OF AGRICULTURE FOOD SCIENCES 229463-ArticleText-557556-1-10-20220809Sunil KhoslaNo ratings yet

- One To One MarketingDocument22 pagesOne To One MarketingSamuel HenriqueNo ratings yet

- Busines EthicsDocument8 pagesBusines EthicsjinkyNo ratings yet

- Antoine Resume 52020Document2 pagesAntoine Resume 52020api-512211605No ratings yet

- From Inception of Operations To December 31 2008 Blaise PascalDocument1 pageFrom Inception of Operations To December 31 2008 Blaise PascalM Bilal SaleemNo ratings yet

- UniqloDocument17 pagesUniqloUmar GondalNo ratings yet

- Costing FM Mock Test May 2019Document20 pagesCosting FM Mock Test May 2019Roshinisai VuppalaNo ratings yet

- Bera - A Real World Case StudyDocument2 pagesBera - A Real World Case StudyNasir HussainNo ratings yet

- Quantitative Decision Making and Optimization Models in Logistics & Supply Chain ManagementDocument3 pagesQuantitative Decision Making and Optimization Models in Logistics & Supply Chain ManagementGada NagariNo ratings yet

- Principles of Marketing - Quarter 3 - Module 3 (For Print)Document10 pagesPrinciples of Marketing - Quarter 3 - Module 3 (For Print)Stephanie Minor75% (4)

- Tutorial - 1 - 2 - (06.10.2022, 13.10.22) TOPIC: Basic Cost Terms and Concepts, Cost Classification Ex. 1Document3 pagesTutorial - 1 - 2 - (06.10.2022, 13.10.22) TOPIC: Basic Cost Terms and Concepts, Cost Classification Ex. 1Tomas SanzNo ratings yet

- Dr. Beckett's Dental Office Case AnalysisDocument10 pagesDr. Beckett's Dental Office Case AnalysischnavinkumarNo ratings yet

- Tarea 1 - Ficha Bibliográfica-Hanai KishimotoDocument8 pagesTarea 1 - Ficha Bibliográfica-Hanai KishimotoHanai KishimotoNo ratings yet

- Chapter 1 Business Information Systems in Your CareerDocument23 pagesChapter 1 Business Information Systems in Your CareermeriemNo ratings yet

- B6 - Complete The Text and Reading ComprehensionDocument10 pagesB6 - Complete The Text and Reading ComprehensionAn NgoNo ratings yet

- Cadbury BournvitaDocument11 pagesCadbury Bournvitadiptibhoi0% (1)

- PWC AlertDocument5 pagesPWC AlertAli AyubNo ratings yet

- Strategic Human Resource ManagementDocument59 pagesStrategic Human Resource ManagementFrancisquete BNo ratings yet

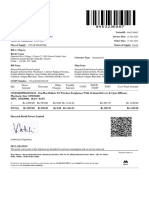

- Tax InvoiceDocument2 pagesTax Invoiceriteshv077777No ratings yet

- SECRETS OF SELLING SUCCESSDocument30 pagesSECRETS OF SELLING SUCCESSventvmNo ratings yet

- 16 - Audit of Financial Market Operations - EngDocument13 pages16 - Audit of Financial Market Operations - EngAraz YagubluNo ratings yet

- Dr. A.K. Sengupta: Former Dean, Indian Institute of Foreign TradeDocument12 pagesDr. A.K. Sengupta: Former Dean, Indian Institute of Foreign TradeimadNo ratings yet

- Push Carts VapeDocument8 pagesPush Carts Vapemuhammad ibrarNo ratings yet

- 2023 January 303 Financial Controls and Audit TaDocument17 pages2023 January 303 Financial Controls and Audit Taimabrar190No ratings yet

- Bulletin EQM 89 - 5SDocument40 pagesBulletin EQM 89 - 5SApurv BhattacharyaNo ratings yet

- Kinsey Institute Working Group ReportDocument19 pagesKinsey Institute Working Group ReportIndiana Public Media NewsNo ratings yet

- Which of The Following Will Not Improve Return On Investment If Other Factors Remain Constant?Document3 pagesWhich of The Following Will Not Improve Return On Investment If Other Factors Remain Constant?Kath LeynesNo ratings yet

- Auditing PresentationDocument54 pagesAuditing PresentationMuzaFarNo ratings yet

- Final Copy of JH Final 08.01.19Document34 pagesFinal Copy of JH Final 08.01.19District Audit Officer DAONo ratings yet

- MCQS Chapter 8 Company Law 2017Document14 pagesMCQS Chapter 8 Company Law 2017BablooNo ratings yet

- Mba 580 Module Five ReportDocument6 pagesMba 580 Module Five ReportShanza qureshiNo ratings yet

- A History of the United States in Five Crashes: Stock Market Meltdowns That Defined a NationFrom EverandA History of the United States in Five Crashes: Stock Market Meltdowns That Defined a NationRating: 4 out of 5 stars4/5 (11)

- Vulture Capitalism: Corporate Crimes, Backdoor Bailouts, and the Death of FreedomFrom EverandVulture Capitalism: Corporate Crimes, Backdoor Bailouts, and the Death of FreedomNo ratings yet

- University of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingFrom EverandUniversity of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingRating: 4.5 out of 5 stars4.5/5 (97)

- The Trillion-Dollar Conspiracy: How the New World Order, Man-Made Diseases, and Zombie Banks Are Destroying AmericaFrom EverandThe Trillion-Dollar Conspiracy: How the New World Order, Man-Made Diseases, and Zombie Banks Are Destroying AmericaNo ratings yet

- The Infinite Machine: How an Army of Crypto-Hackers Is Building the Next Internet with EthereumFrom EverandThe Infinite Machine: How an Army of Crypto-Hackers Is Building the Next Internet with EthereumRating: 3 out of 5 stars3/5 (12)

- The Technology Trap: Capital, Labor, and Power in the Age of AutomationFrom EverandThe Technology Trap: Capital, Labor, and Power in the Age of AutomationRating: 4.5 out of 5 stars4.5/5 (46)

- Narrative Economics: How Stories Go Viral and Drive Major Economic EventsFrom EverandNarrative Economics: How Stories Go Viral and Drive Major Economic EventsRating: 4.5 out of 5 stars4.5/5 (94)

- The War Below: Lithium, Copper, and the Global Battle to Power Our LivesFrom EverandThe War Below: Lithium, Copper, and the Global Battle to Power Our LivesRating: 4.5 out of 5 stars4.5/5 (8)

- Doughnut Economics: Seven Ways to Think Like a 21st-Century EconomistFrom EverandDoughnut Economics: Seven Ways to Think Like a 21st-Century EconomistRating: 4.5 out of 5 stars4.5/5 (37)

- Principles for Dealing with the Changing World Order: Why Nations Succeed or FailFrom EverandPrinciples for Dealing with the Changing World Order: Why Nations Succeed or FailRating: 4.5 out of 5 stars4.5/5 (237)

- Nudge: The Final Edition: Improving Decisions About Money, Health, And The EnvironmentFrom EverandNudge: The Final Edition: Improving Decisions About Money, Health, And The EnvironmentRating: 4.5 out of 5 stars4.5/5 (92)

- The Genius of Israel: The Surprising Resilience of a Divided Nation in a Turbulent WorldFrom EverandThe Genius of Israel: The Surprising Resilience of a Divided Nation in a Turbulent WorldRating: 4 out of 5 stars4/5 (17)

- This Changes Everything: Capitalism vs. The ClimateFrom EverandThis Changes Everything: Capitalism vs. The ClimateRating: 4 out of 5 stars4/5 (349)

- Financial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassFrom EverandFinancial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassNo ratings yet

- The New Elite: Inside the Minds of the Truly WealthyFrom EverandThe New Elite: Inside the Minds of the Truly WealthyRating: 4 out of 5 stars4/5 (10)

- The Lords of Easy Money: How the Federal Reserve Broke the American EconomyFrom EverandThe Lords of Easy Money: How the Federal Reserve Broke the American EconomyRating: 4.5 out of 5 stars4.5/5 (69)

- Look Again: The Power of Noticing What Was Always ThereFrom EverandLook Again: The Power of Noticing What Was Always ThereRating: 5 out of 5 stars5/5 (3)

- Chip War: The Quest to Dominate the World's Most Critical TechnologyFrom EverandChip War: The Quest to Dominate the World's Most Critical TechnologyRating: 4.5 out of 5 stars4.5/5 (227)

- Second Class: How the Elites Betrayed America's Working Men and WomenFrom EverandSecond Class: How the Elites Betrayed America's Working Men and WomenNo ratings yet

- The Myth of the Rational Market: A History of Risk, Reward, and Delusion on Wall StreetFrom EverandThe Myth of the Rational Market: A History of Risk, Reward, and Delusion on Wall StreetNo ratings yet

- The Finance Curse: How Global Finance Is Making Us All PoorerFrom EverandThe Finance Curse: How Global Finance Is Making Us All PoorerRating: 4.5 out of 5 stars4.5/5 (18)

- How an Economy Grows and Why It Crashes: Collector's EditionFrom EverandHow an Economy Grows and Why It Crashes: Collector's EditionRating: 4.5 out of 5 stars4.5/5 (102)