You might also like

- Parameters of Monetary Policy in India Y.V. Reddy: ObjectivesDocument14 pagesParameters of Monetary Policy in India Y.V. Reddy: Objectiveslopa_titanNo ratings yet

- Parameters of MPDocument10 pagesParameters of MPJuglaryNo ratings yet

- Monetary Policy Under The Border Between Price Stability and Financial StabilityDocument9 pagesMonetary Policy Under The Border Between Price Stability and Financial StabilityDumitrescu MeedyNo ratings yet

- Central Bank Policy Mix: Key Concepts and Indonesia’s ExperienceDocument30 pagesCentral Bank Policy Mix: Key Concepts and Indonesia’s ExperienceFaishal Ahmad FarrosiNo ratings yet

- Perry Warjiyo, Indonesia, Stabilizing The Exchange Rate Along Its FundamentalDocument11 pagesPerry Warjiyo, Indonesia, Stabilizing The Exchange Rate Along Its FundamentalQarinaNo ratings yet

- Can Vietnam Move To in Flation Targeting?Document10 pagesCan Vietnam Move To in Flation Targeting?NA NANo ratings yet

- Abstract:: Why Focus On Price Stability?Document11 pagesAbstract:: Why Focus On Price Stability?Farooq SiddiquiNo ratings yet

- Monetary Policy and Inflation in Zambia: JEL Classification: C50, E52 Cointegrated Vector Autoregressive Model, VECXDocument37 pagesMonetary Policy and Inflation in Zambia: JEL Classification: C50, E52 Cointegrated Vector Autoregressive Model, VECXWilliam FedoungNo ratings yet

- Monetary policy lessons from financial turmoilDocument8 pagesMonetary policy lessons from financial turmoilfanfaniNo ratings yet

- Macroeconomic and Financial Sector Policies in EMDEs Before and After the Global RecessionDocument43 pagesMacroeconomic and Financial Sector Policies in EMDEs Before and After the Global RecessionGfi ConexionNo ratings yet

- Monetary PolicyDocument9 pagesMonetary Policyfatemah zahidNo ratings yet

- Monetary Policy Dynamics in IndiaDocument73 pagesMonetary Policy Dynamics in IndiaMangala Ghosh100% (2)

- MacroDocument34 pagesMacroPratik LawanaNo ratings yet

- Effectiveness of Monetary PolicyDocument8 pagesEffectiveness of Monetary PolicyMiguel SmithNo ratings yet

- Managing Mon-Finstab Policy Mix 2016Document37 pagesManaging Mon-Finstab Policy Mix 2016desta yolandaNo ratings yet

- Considerations Regarding Monetary and Fiscal Exit Strategies From The CrisisDocument5 pagesConsiderations Regarding Monetary and Fiscal Exit Strategies From The CrisisDănutsa BănişorNo ratings yet

- Lars E O Svensson Discusses Monetary Policy Lessons from Financial CrisisDocument6 pagesLars E O Svensson Discusses Monetary Policy Lessons from Financial CrisisDamien PuyNo ratings yet

- Effect of monetary policies on insurance sector growth in NigeriaDocument10 pagesEffect of monetary policies on insurance sector growth in NigeriaEverpeeNo ratings yet

- Monetary Policy and Central Banking PDFDocument2 pagesMonetary Policy and Central Banking PDFTrisia Corinne JaringNo ratings yet

- 2b. Bauran Kebijakan Bank SentralDocument25 pages2b. Bauran Kebijakan Bank SentralVicky Achmad MNo ratings yet

- INFLATION TARGETING STRATEGYDocument8 pagesINFLATION TARGETING STRATEGYUsman HassanNo ratings yet

- Ec4303 Group 1 AssignmentDocument8 pagesEc4303 Group 1 AssignmentLekhutla TFNo ratings yet

- Global Financial Crisis Reveals Need for Robust Financial Stability FrameworksDocument6 pagesGlobal Financial Crisis Reveals Need for Robust Financial Stability FrameworksGoutam GhoshNo ratings yet

- Relationship Between Central Bank and The TreasuryDocument4 pagesRelationship Between Central Bank and The TreasuryGurleen KaurNo ratings yet

- Monetary and Fiscal Policy: Smoothing The Operation of The MarketDocument15 pagesMonetary and Fiscal Policy: Smoothing The Operation of The Marketasiacup105No ratings yet

- Chapter One: General IntroductionDocument20 pagesChapter One: General IntroductionCool ManNo ratings yet

- Felcser - Inflation TargetingDocument64 pagesFelcser - Inflation Targetingdebreceni.sandor.770712No ratings yet

- Monetary Policy in New ZealandDocument3 pagesMonetary Policy in New ZealandRoshNo ratings yet

- Rethinking Monetary Policy After the CrisisDocument23 pagesRethinking Monetary Policy After the CrisisAlexDuarteVelasquezNo ratings yet

- Effects of Monetary Policy On The Banking System Stability in NigDocument19 pagesEffects of Monetary Policy On The Banking System Stability in NigElijah OmoboriowoNo ratings yet

- Monetary and Fiscal PolicyDocument18 pagesMonetary and Fiscal PolicyEmuyeNo ratings yet

- Financial Innovation and Monetary Policy Transmission in KenyaDocument14 pagesFinancial Innovation and Monetary Policy Transmission in KenyaArif Ali SyedNo ratings yet

- Efficiency of Monetary Policy in Price InstabilityDocument11 pagesEfficiency of Monetary Policy in Price InstabilityHussainul Islam SajibNo ratings yet

- General Assessment of The Macroeconomic Situation: The Recovery Is Strengthening Albeit Slowly and UnevenlyDocument82 pagesGeneral Assessment of The Macroeconomic Situation: The Recovery Is Strengthening Albeit Slowly and UnevenlygbbajajNo ratings yet

- OECD 2010 paper examines counter-cyclical economic policiesDocument9 pagesOECD 2010 paper examines counter-cyclical economic policiesAdnan KamalNo ratings yet

- 022216b PDFDocument38 pages022216b PDFkhushal kumarNo ratings yet

- 10 11648 J Ijfbr 20190504 14Document14 pages10 11648 J Ijfbr 20190504 14Minh NguyễnNo ratings yet

- Jing - Relative Effectiveness of Fiscal and Monetary Policy Shocks On The Ethiopian Economic Growth A Structural Vector Autoregressive ModelDocument19 pagesJing - Relative Effectiveness of Fiscal and Monetary Policy Shocks On The Ethiopian Economic Growth A Structural Vector Autoregressive ModelNova TambunanNo ratings yet

- Thesis Monetary PolicyDocument6 pagesThesis Monetary Policycgvmxrief100% (2)

- 285 PetriaDocument6 pages285 PetriaEne Emanuel-StefanNo ratings yet

- Monetary Policy in JamaicaDocument37 pagesMonetary Policy in JamaicaMarie NelsonNo ratings yet

- Role of Macroprudential Policy in Asia's Financial StabilityDocument3 pagesRole of Macroprudential Policy in Asia's Financial StabilityAndy SugiantoNo ratings yet

- Transmission Mechanism of MPDocument19 pagesTransmission Mechanism of MPDeni Wahyudi19No ratings yet

- Economics Research PaperDocument11 pagesEconomics Research PaperSomya GulatiNo ratings yet

- Contours Monetary PolicyDocument16 pagesContours Monetary PolicyRajiv DayaramaniNo ratings yet

- 10 Sample Vietnam Ir LiberalizationDocument28 pages10 Sample Vietnam Ir LiberalizationNgọc Vinh NgôNo ratings yet

- IMPACT OF FISCAL POLICY AND MONETARY POLICY ON THE ECONOMIC GROWTH OF NIGERIA (1980 – 2016)Document22 pagesIMPACT OF FISCAL POLICY AND MONETARY POLICY ON THE ECONOMIC GROWTH OF NIGERIA (1980 – 2016)AJHSSR JournalNo ratings yet

- Managing Development - Globalization, Economic Restructuring and Social PolicyDocument14 pagesManaging Development - Globalization, Economic Restructuring and Social PolicysheenaNo ratings yet

- Impact of Monetary Policies On Inflation in NigeriaDocument10 pagesImpact of Monetary Policies On Inflation in NigeriaAina Oluwasanmi100% (1)

- Macroeconomic Analysis in MalaysiaDocument7 pagesMacroeconomic Analysis in MalaysiaCaroline MartinNo ratings yet

- U Iii: M P: NIT Onetary OlicyDocument27 pagesU Iii: M P: NIT Onetary OlicyNithyananda PatelNo ratings yet

- Impact of Monetary Policy On Economic Growth - A Case Study of South AfricaDocument9 pagesImpact of Monetary Policy On Economic Growth - A Case Study of South AfricaAbdulkabirNo ratings yet

- Monetary Policy of BangladeshDocument26 pagesMonetary Policy of Bangladeshsuza054No ratings yet

- Monetary vs Fiscal Policies: What Does a Long-Run SVAR Model Tell UsDocument24 pagesMonetary vs Fiscal Policies: What Does a Long-Run SVAR Model Tell UsAlain DirzuNo ratings yet

- Enspecial Series On Covid19monetary and Financial Policy Responses For Emerging Market and DevelopinDocument5 pagesEnspecial Series On Covid19monetary and Financial Policy Responses For Emerging Market and DevelopinAlip FajarNo ratings yet

- Global InflationDocument7 pagesGlobal InflationJeremiah AnjorinNo ratings yet

- Macroeconomic policies more effective in closed vs open economiesDocument18 pagesMacroeconomic policies more effective in closed vs open economiesSimran GopalNo ratings yet

- Inflation Targeting in AfricaDocument7 pagesInflation Targeting in AfricaAhmad AtandaNo ratings yet

- Chipping Away at Public Debt: Sources of Failure and Keys to Success in Fiscal AdjustmentFrom EverandChipping Away at Public Debt: Sources of Failure and Keys to Success in Fiscal AdjustmentRating: 1 out of 5 stars1/5 (1)

- Jakarta Is Shinking CaseDocument2 pagesJakarta Is Shinking CaseHABIBUL WAHID HARMADANNo ratings yet

- Transaction CostDocument1 pageTransaction CostHABIBUL WAHID HARMADANNo ratings yet

- When Old Is New and New Is OldDocument13 pagesWhen Old Is New and New Is OldHABIBUL WAHID HARMADANNo ratings yet

- Civics EducationDocument2 pagesCivics EducationHABIBUL WAHID HARMADANNo ratings yet

- Completing The Accounting Cycle: Financial Accounting, IRFS Weygandt Kimmel KiesoDocument55 pagesCompleting The Accounting Cycle: Financial Accounting, IRFS Weygandt Kimmel KiesoMaria jecikaNo ratings yet

- Bank IndonesiaDocument7 pagesBank IndonesiaHABIBUL WAHID HARMADANNo ratings yet

- Haty Store - Stock Grand OpeningDocument8 pagesHaty Store - Stock Grand OpeningHABIBUL WAHID HARMADANNo ratings yet

- 30 4eDocument40 pages30 4ekhamisalkaabiNo ratings yet

- Hurricane KatrinaDocument11 pagesHurricane KatrinaHABIBUL WAHID HARMADANNo ratings yet

- ACTIVITY 2 - Semester 2Document1 pageACTIVITY 2 - Semester 2HABIBUL WAHID HARMADANNo ratings yet

- Low Reading Literacy Index in IndonesiaDocument3 pagesLow Reading Literacy Index in IndonesiaHABIBUL WAHID HARMADANNo ratings yet

- BRAINSTORMINGDocument2 pagesBRAINSTORMINGHABIBUL WAHID HARMADANNo ratings yet

- =Document2 pages=HABIBUL WAHID HARMADANNo ratings yet

- Activity 4Document1 pageActivity 4HABIBUL WAHID HARMADANNo ratings yet

- Pak Awan Final ExamDocument2 pagesPak Awan Final ExamHABIBUL WAHID HARMADANNo ratings yet

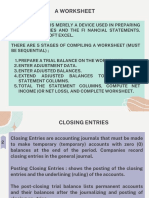

- A WorksheetDocument6 pagesA WorksheetHABIBUL WAHID HARMADANNo ratings yet

- 365 BDocument766 pages365 BThis is BusinessNo ratings yet

- معايير Ch 2 InventoriesDocument11 pagesمعايير Ch 2 InventoriesHamza MahmoudNo ratings yet

- Payterm and payer detailsDocument1 pagePayterm and payer detailsEngels Garcia67% (9)

- Spring 2024 EFIN 403 (01) Syllabus 09 12 2023Document3 pagesSpring 2024 EFIN 403 (01) Syllabus 09 12 2023EDA SEYDINo ratings yet

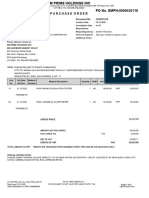

- Po 1200791578Document2 pagesPo 1200791578john.valbuenaNo ratings yet

- Review of COGS and CGMDocument4 pagesReview of COGS and CGMChloe Ann CabayloNo ratings yet

- Public Finance MCQDocument23 pagesPublic Finance MCQHarshit TripathiNo ratings yet

- Department of Mba Ba5031 - International Trade Finance Part ADocument5 pagesDepartment of Mba Ba5031 - International Trade Finance Part AHarihara PuthiranNo ratings yet

- Project Cost Management April 2021Document189 pagesProject Cost Management April 2021bharathiNo ratings yet

- Cesses and SurchargesDocument80 pagesCesses and SurchargesAnkit KumarNo ratings yet

- RSM - 1 IntroDocument18 pagesRSM - 1 IntroPrayesh ShahNo ratings yet

- Pep - Monetary Policy (Final Term Report)Document21 pagesPep - Monetary Policy (Final Term Report)Fiza Abdul HameedNo ratings yet

- Road Freight Transport Sector and Emerging Competitive Dynamics FinalDocument38 pagesRoad Freight Transport Sector and Emerging Competitive Dynamics FinalZain IqbalNo ratings yet

- Info Forex World - UkDocument13 pagesInfo Forex World - Ukambabaji456No ratings yet

- CBIC Civil List As On 01.01.2022Document568 pagesCBIC Civil List As On 01.01.2022रुद्र प्रताप सिंह ८२No ratings yet

- Billing and Shipping Address Details for OrderDocument1 pageBilling and Shipping Address Details for OrderrezolfNo ratings yet

- Trading in Derivatives Introduction To Futures - GBDocument58 pagesTrading in Derivatives Introduction To Futures - GBNOR IZZATI BINTI SAZALINo ratings yet

- Danika Cristoal 18aDocument4 pagesDanika Cristoal 18aapi-462148990No ratings yet

- RBI and Its Control Over BanksDocument10 pagesRBI and Its Control Over BanksHarshad PatilNo ratings yet

- Chapter 18Document9 pagesChapter 18Regita AuliaNo ratings yet

- Op Transaction HistoryDocument2 pagesOp Transaction HistorySappy SoniNo ratings yet

- AMB Crypto Assignment - VidhathriMatetyDocument4 pagesAMB Crypto Assignment - VidhathriMatetyVidhathri MatetyNo ratings yet

- A Case Study On Time Value of Money.: Sakshi Bezalwar-09 MMS 1 (Div-A)Document10 pagesA Case Study On Time Value of Money.: Sakshi Bezalwar-09 MMS 1 (Div-A)Sakshi BezalwarNo ratings yet

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)kishanprasadNo ratings yet

- Product Stock Exchange Learn BookDocument1 pageProduct Stock Exchange Learn BookSujit MauryaNo ratings yet

- BP Banana (Draft) (2) 12.6.17Document93 pagesBP Banana (Draft) (2) 12.6.17Derwin DomiderNo ratings yet

- Ch-1 Indian Economy in The Eve of Independance (Choice Based Questions)Document9 pagesCh-1 Indian Economy in The Eve of Independance (Choice Based Questions)social sitesNo ratings yet

- Risk Surcharge: Mode: AIRDocument9 pagesRisk Surcharge: Mode: AIRYasar SyedNo ratings yet

- Service Sector of PakistanDocument2 pagesService Sector of PakistanDaniyalHaiderNo ratings yet

- 617B - Logistics and Supply Chain ManagementDocument21 pages617B - Logistics and Supply Chain Managementactivity_xtraNo ratings yet