You might also like

- History and Functions of the Reserve Bank of IndiaDocument5 pagesHistory and Functions of the Reserve Bank of IndiaJay Ram100% (1)

- Regulatory Framework of Financial ServicesDocument47 pagesRegulatory Framework of Financial ServicesUrvashi Tody100% (3)

- DLL ENTREP Week 9Document6 pagesDLL ENTREP Week 9KATHERINE JOY ZARANo ratings yet

- Account Statement: Parikshit YadavDocument19 pagesAccount Statement: Parikshit YadavParikshit YadavNo ratings yet

- Republic of The PhilippinesDocument7 pagesRepublic of The Philippinesvita feliceNo ratings yet

- Project On NBFCDocument67 pagesProject On NBFCAnu Pandey77% (44)

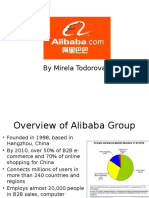

- 3 AlibabaDocument24 pages3 AlibabaADAM LOW0% (1)

- MCI Communications CorporationDocument6 pagesMCI Communications Corporationnipun9143No ratings yet

- Various Quantitative Tools Applied by RBI As Controller of Credit and Regulator of Money SupplyDocument4 pagesVarious Quantitative Tools Applied by RBI As Controller of Credit and Regulator of Money SupplyShadab HasanNo ratings yet

- Indian Banking Industry: What Is A Bank?Document7 pagesIndian Banking Industry: What Is A Bank?Taru SrivastavaNo ratings yet

- RBI - VI sem B&F all functionsDocument10 pagesRBI - VI sem B&F all functionsvinushriyuNo ratings yet

- Reserve Bank of India - Prathyusha PDFDocument5 pagesReserve Bank of India - Prathyusha PDFPolamada PrathyushaNo ratings yet

- RBI's Role in Regulating India's Banking & Financial SystemDocument20 pagesRBI's Role in Regulating India's Banking & Financial SystemSophiya KhanamNo ratings yet

- Avik Static Final Gradeup12.PDF-94Document58 pagesAvik Static Final Gradeup12.PDF-94Jagannath JagguNo ratings yet

- RBI and Its FunctionDocument5 pagesRBI and Its FunctionSweta PandeyNo ratings yet

- Roles & Functions of Reserve Bank of India: Useful LinksDocument7 pagesRoles & Functions of Reserve Bank of India: Useful LinksJaldeep MangawaNo ratings yet

- Overview of Indian Financial SystemDocument6 pagesOverview of Indian Financial Systemhitesh prithianiNo ratings yet

- Rbi PDFDocument6 pagesRbi PDFYamuna ViswamNo ratings yet

- RBI's key roles in the Indian economyDocument2 pagesRBI's key roles in the Indian economynikitasharma88_49144No ratings yet

- Role and Functions of Reserve Bank of IndiaDocument5 pagesRole and Functions of Reserve Bank of Indiaanusaya1988No ratings yet

- RBI and Its FunctionsDocument14 pagesRBI and Its FunctionsSuchandra SarkarNo ratings yet

- Role of RBI Under Banking Regulation Act, 1949Document11 pagesRole of RBI Under Banking Regulation Act, 1949Jay Ram100% (1)

- Reserve Bank of India: HistoryDocument4 pagesReserve Bank of India: HistoryEku Nahoi HoilepeNo ratings yet

- Kiran Gundaye (2029)Document55 pagesKiran Gundaye (2029)Kiran GundayeNo ratings yet

- 18MBAFM301: Mr. Varun K Assistant Professor Department of Business Administration MITE, MoodbidriDocument36 pages18MBAFM301: Mr. Varun K Assistant Professor Department of Business Administration MITE, MoodbidriHariprasad bhatNo ratings yet

- Reserve Bank of India Act, 1934: EstablishmentDocument4 pagesReserve Bank of India Act, 1934: Establishmentagrawalvaibhav729No ratings yet

- Reserve Bank of India Act, 1934: Repo Rate: 7.25%Document10 pagesReserve Bank of India Act, 1934: Repo Rate: 7.25%Anjulika SinghNo ratings yet

- 5 & 6. Money & BankingDocument5 pages5 & 6. Money & BankingManav Ji manvNo ratings yet

- Index On BoxesDocument76 pagesIndex On BoxesAmritNo ratings yet

- Banking & FIsDocument12 pagesBanking & FIsAmbalika SmitiNo ratings yet

- Monetary PolicyDocument5 pagesMonetary PolicyKuthubudeen T MNo ratings yet

- Central Bank of India & Its Functions (RBIDocument7 pagesCentral Bank of India & Its Functions (RBIPriyam PrakashNo ratings yet

- Rbi PDFDocument4 pagesRbi PDFUmar AbdullahNo ratings yet

- RBI Functions List: Traditional, Developmental, SupervisoryDocument25 pagesRBI Functions List: Traditional, Developmental, Supervisorygeethark12100% (1)

- RESERVE BANK OF INDIA (Shivam)Document6 pagesRESERVE BANK OF INDIA (Shivam)nishantarya283No ratings yet

- Central Banking: Chapter-5Document15 pagesCentral Banking: Chapter-5Ruthvik RevanthNo ratings yet

- A Brief History of the Evolution of Indian BankingDocument11 pagesA Brief History of the Evolution of Indian BankingMidnyt PrinceNo ratings yet

- Banking NotesDocument12 pagesBanking NotesChiranjive Ravindra JagadalNo ratings yet

- Role TPDocument3 pagesRole TPKunal Patil.22No ratings yet

- Unit - II - Banking RegulationDocument14 pagesUnit - II - Banking RegulationShreya PushkarnaNo ratings yet

- Digital Assignment-1 Subject Code-Bmt1013 Subject Name - Banking and InsuranceDocument9 pagesDigital Assignment-1 Subject Code-Bmt1013 Subject Name - Banking and InsuranceSwethaNo ratings yet

- Rbi and Its Monetary PolicyDocument5 pagesRbi and Its Monetary PolicyPravin NisharNo ratings yet

- TEAM 3 - Assg 3 - Functions of RBIDocument11 pagesTEAM 3 - Assg 3 - Functions of RBIVISHAL MNo ratings yet

- Role of Reserve Bank of India - 084809 WORDDocument4 pagesRole of Reserve Bank of India - 084809 WORDAniket ShigwanNo ratings yet

- Functions of RbiDocument4 pagesFunctions of RbiMunish PathaniaNo ratings yet

- BANKINGDocument13 pagesBANKINGMaharajascollege KottayamNo ratings yet

- FIM-Module II-Banking InstitutionsDocument11 pagesFIM-Module II-Banking InstitutionsAmarendra PattnaikNo ratings yet

- IIBFDocument106 pagesIIBFRajan NandolaNo ratings yet

- Banking Law Qestion Paper AnswersDocument101 pagesBanking Law Qestion Paper AnswersThrishul MaheshNo ratings yet

- Financial Sector Reforms in IndiaDocument14 pagesFinancial Sector Reforms in IndiaRimple Abhishek Delisha ViraajvirNo ratings yet

- Functions of RBIDocument3 pagesFunctions of RBITarun BhatejaNo ratings yet

- India's 5 Key Financial RegulatorsDocument6 pagesIndia's 5 Key Financial RegulatorsRaman SrivastavaNo ratings yet

- Features and Objectives of Money MarketsDocument23 pagesFeatures and Objectives of Money MarketsYashaswini Gowda100% (1)

- A Presentation On: Role of Reserve Bank of India in Indian EconomyDocument25 pagesA Presentation On: Role of Reserve Bank of India in Indian EconomyVimal SinghNo ratings yet

- RBI Monetary PolicyDocument13 pagesRBI Monetary PolicyramixudinNo ratings yet

- 2.FIM-Module II-Banking InstitutionsDocument11 pages2.FIM-Module II-Banking InstitutionsAmarendra PattnaikNo ratings yet

- Good MorningDocument24 pagesGood MorningManoj KumarNo ratings yet

- INDIAN BANKING SYSTEM: KEY CONSTITUENTSDocument25 pagesINDIAN BANKING SYSTEM: KEY CONSTITUENTSTajinder JassalNo ratings yet

- Banking India: Accepting Deposits for the Purpose of LendingFrom EverandBanking India: Accepting Deposits for the Purpose of LendingNo ratings yet

- T R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)From EverandT R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)No ratings yet

- Banks and Bank ManagementDocument6 pagesBanks and Bank ManagementyjgjbhhbNo ratings yet

- An Overview of Financial SystemsDocument10 pagesAn Overview of Financial SystemsyjgjbhhbNo ratings yet

- Stock MarketDocument9 pagesStock MarketyjgjbhhbNo ratings yet

- DERIVATIVES IncompleteDocument9 pagesDERIVATIVES IncompleteyjgjbhhbNo ratings yet

- NitroDocument7 pagesNitroyjgjbhhbNo ratings yet

- PCT/US2020/059893 - Preparation of API Mavacamten via IntermediatesDocument6 pagesPCT/US2020/059893 - Preparation of API Mavacamten via IntermediatesyjgjbhhbNo ratings yet

- Snake LTD - Class WorkingsDocument2 pagesSnake LTD - Class Workingsmusa morinNo ratings yet

- CV - Tim SonmezDocument1 pageCV - Tim Sonmezapi-356802988No ratings yet

- Child Labor: A Global View: Cathryne L. Schmitz Elizabeth Kimjin Traver Desi Larson EditorsDocument230 pagesChild Labor: A Global View: Cathryne L. Schmitz Elizabeth Kimjin Traver Desi Larson EditorsRamiroNo ratings yet

- Balance Sheet: 07 - Standalone Financial - 28-06-2019.indd 206 7/5/2019 6:36:18 PMDocument1 pageBalance Sheet: 07 - Standalone Financial - 28-06-2019.indd 206 7/5/2019 6:36:18 PMharshit abrolNo ratings yet

- Human Resource Accounting Practices in Indian Companies: Bottorof$ ( - Tlosiop P CommerceDocument305 pagesHuman Resource Accounting Practices in Indian Companies: Bottorof$ ( - Tlosiop P CommerceSanaullah M SultanpurNo ratings yet

- Appointment Letter: Teamlease Services Limited., Cin No. L74140Ka2000Plc118395Document4 pagesAppointment Letter: Teamlease Services Limited., Cin No. L74140Ka2000Plc118395amrit barmanNo ratings yet

- ProspectusDocument2 pagesProspectusJuliana Mae FradesNo ratings yet

- Corporate Social Responsibility MainDocument2 pagesCorporate Social Responsibility MainhagdincloobleNo ratings yet

- La Performance Des Fusions Et Acquisitions Bancaires - BCM at AwbDocument11 pagesLa Performance Des Fusions Et Acquisitions Bancaires - BCM at AwbyousseffNo ratings yet

- ECONOMIC APPLICATIONS HANDS-ON EXPERIENCEDocument6 pagesECONOMIC APPLICATIONS HANDS-ON EXPERIENCEPankaj KumarNo ratings yet

- Bangladesh Steel Industry - December 2019 PDFDocument19 pagesBangladesh Steel Industry - December 2019 PDFMahmudul Hasan SajibNo ratings yet

- IFRS 1 Technical SummaryDocument2 pagesIFRS 1 Technical SummaryShashank GuptaNo ratings yet

- Sivagnanam PDFDocument213 pagesSivagnanam PDFjohn100% (1)

- Presentation On Internship Program Done at The Enq: Subhankar BhattacharjeeDocument28 pagesPresentation On Internship Program Done at The Enq: Subhankar BhattacharjeeSubhankar BhattacharjeeNo ratings yet

- ASEAN - Economic Integration and Development of SMEsDocument6 pagesASEAN - Economic Integration and Development of SMEssreypichNo ratings yet

- Original Aucm Accounting For Decision Making 4E Wiley E Text For Deakin Full ChapterDocument41 pagesOriginal Aucm Accounting For Decision Making 4E Wiley E Text For Deakin Full Chapterbetty.neverson777100% (26)

- Accounting For Income Taxes: About This Chapter!Document9 pagesAccounting For Income Taxes: About This Chapter!sabithpaulNo ratings yet

- Suport Curs 13Document11 pagesSuport Curs 13Sorin GabrielNo ratings yet

- Manish Gupta: Presented byDocument20 pagesManish Gupta: Presented byManish GuptaNo ratings yet

- Swot Analysis - IKEADocument7 pagesSwot Analysis - IKEAAaltu FaltuNo ratings yet

- Financing Your Franchised BusinessDocument17 pagesFinancing Your Franchised BusinessDanna Marie BanayNo ratings yet

- Group II - June 2010 Cost and Management Accounting: The Figures in The Margin On The Right Side Indicate Full MarksDocument23 pagesGroup II - June 2010 Cost and Management Accounting: The Figures in The Margin On The Right Side Indicate Full MarksMahesh BabuNo ratings yet

- JBIMS M.SC - Finance Placement Report 2019 20Document10 pagesJBIMS M.SC - Finance Placement Report 2019 205vipinappuNo ratings yet

- Unit 10 - Assignment 2 (LO3&LO4) (Essam Hamad) (19011285)Document11 pagesUnit 10 - Assignment 2 (LO3&LO4) (Essam Hamad) (19011285)Essam HamadNo ratings yet

- (Terms and Conditions of Contract For Position of General Manager) Hanoi 22 January, 2021Document4 pages(Terms and Conditions of Contract For Position of General Manager) Hanoi 22 January, 2021Angel Beluso DumotNo ratings yet