You might also like

- Chapter 2Document12 pagesChapter 2Alyssa BerangberangNo ratings yet

- Transaction Processing and Enterprise Resource Planning SystemsDocument12 pagesTransaction Processing and Enterprise Resource Planning SystemsGundamSeedNo ratings yet

- 3141 ConceptDocument10 pages3141 ConceptDiane LockhartNo ratings yet

- ACCTING 2503 Accounting Information Systems Exam Notes PDocument5 pagesACCTING 2503 Accounting Information Systems Exam Notes PHerbert AmbesiNo ratings yet

- Ais ReviewerDocument11 pagesAis Reviewersheryllescoto10No ratings yet

- Chapter 1: Introduction To AISDocument29 pagesChapter 1: Introduction To AISFatiha YusofNo ratings yet

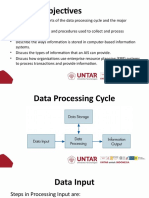

- Data Processing CycleDocument11 pagesData Processing CycleGundamSeedNo ratings yet

- Chapter 2-Introduction To Transaction ProcessingDocument2 pagesChapter 2-Introduction To Transaction ProcessingI Am Not DeterredNo ratings yet

- Overview of Transaction Processing and Enterprise Resource Planning SystemsDocument34 pagesOverview of Transaction Processing and Enterprise Resource Planning SystemsShe RCNo ratings yet

- A20 PrelimDocument3 pagesA20 Prelimdre thegreatNo ratings yet

- CHPTR 2 AisDocument6 pagesCHPTR 2 AisJames Ryan AlzonaNo ratings yet

- Chapter 1 (The Information Environment)Document13 pagesChapter 1 (The Information Environment)Alyssa BerangberangNo ratings yet

- AIS ReviewerDocument4 pagesAIS ReviewerJaeNo ratings yet

- CH 2 Overview of Transaction Processing and ERP SystemsDocument5 pagesCH 2 Overview of Transaction Processing and ERP SystemsAnita Eva Erdina0% (1)

- Overview of Transaction Processing and Enterprise Resource Planning SystemsDocument34 pagesOverview of Transaction Processing and Enterprise Resource Planning SystemsJulius JasisNo ratings yet

- Ais Notes Chap2Document7 pagesAis Notes Chap2mejaneisip479No ratings yet

- Ais (Module)Document6 pagesAis (Module)justinnNo ratings yet

- Ais ReviewerDocument5 pagesAis ReviewerJohn Ford E. MejiaNo ratings yet

- Rps Bahan Ajar EA63015 126 2Document15 pagesRps Bahan Ajar EA63015 126 2GundamSeedNo ratings yet

- Record-A Set of Logically Related Data Items That Describe Specific AttributesDocument1 pageRecord-A Set of Logically Related Data Items That Describe Specific AttributesClarisse AlimotNo ratings yet

- CHAPTER 2: Overview of Business Processes: Management by Exception Is AnDocument1 pageCHAPTER 2: Overview of Business Processes: Management by Exception Is Ansamsam9095No ratings yet

- Overview of Transaction Processing and Enterprise Resource Planning SystemsDocument21 pagesOverview of Transaction Processing and Enterprise Resource Planning SystemsHibaaq AxmedNo ratings yet

- TÓM TẮT HTTTKDDocument36 pagesTÓM TẮT HTTTKDNhi Phạm Thị ÁiNo ratings yet

- Chapter 1 The Information System An Accountant's PerspectiveDocument40 pagesChapter 1 The Information System An Accountant's PerspectiveFarah Byun100% (1)

- Accounting Information System ReviewerDocument16 pagesAccounting Information System RevieweralabwalaNo ratings yet

- Ais Chapter 1 and 2 QuizletDocument63 pagesAis Chapter 1 and 2 QuizletVenice Espinoza100% (1)

- Chapter Two: An Introduction To Data ProcessingDocument7 pagesChapter Two: An Introduction To Data ProcessingmohammedNo ratings yet

- Information Systems: Computer System Hardware SoftwareDocument33 pagesInformation Systems: Computer System Hardware SoftwareCA Subodh AgarwalNo ratings yet

- Lecture 5Document52 pagesLecture 5Rana GaballahNo ratings yet

- Unit 02-Business ProcessesDocument20 pagesUnit 02-Business Processeshiranya939509No ratings yet

- Liu Ais CH 2Document36 pagesLiu Ais CH 2hassan nassereddineNo ratings yet

- Overview of Transaction Processing and Enterprise Resource Planning SystemsDocument15 pagesOverview of Transaction Processing and Enterprise Resource Planning SystemsKim Raven CoNo ratings yet

- Information Systems Within The OrganizationDocument11 pagesInformation Systems Within The OrganizationbernadetteNo ratings yet

- Chapter 2 Transaction ProcessingDocument11 pagesChapter 2 Transaction ProcessingABStract001No ratings yet

- Chapter One Introduction To AISDocument5 pagesChapter One Introduction To AISTHOTslayer 420No ratings yet

- Information System Activities and Its TypesDocument19 pagesInformation System Activities and Its TypesNarender KumarNo ratings yet

- c2 Introduction To Transaction ProcessingDocument14 pagesc2 Introduction To Transaction ProcessingLee SuarezNo ratings yet

- Enterprise Systems - Integrates Business Process Functionality and Information From All of AnDocument12 pagesEnterprise Systems - Integrates Business Process Functionality and Information From All of AnShaina ObreroNo ratings yet

- Resumo Apostilas - Academia HR - InglesDocument93 pagesResumo Apostilas - Academia HR - InglessevegnaniNo ratings yet

- Concept of Data and Information, Information SystemsDocument8 pagesConcept of Data and Information, Information SystemsAshish DixitNo ratings yet

- Data Warehouse Concepts With Dimensional ModelingDocument36 pagesData Warehouse Concepts With Dimensional Modelingpushpinder.7979No ratings yet

- AACS1304 01 - Introduction To Is 202005Document49 pagesAACS1304 01 - Introduction To Is 202005WIN YE KUANNo ratings yet

- Chapter Ii - AisDocument29 pagesChapter Ii - AisMarc Jason LanzarroteNo ratings yet

- Ais Hall 7e Chap1Document41 pagesAis Hall 7e Chap1tipo_de_incognitoNo ratings yet

- Accounting Information System - Chapter 1Document41 pagesAccounting Information System - Chapter 1Lizette OlivaNo ratings yet

- Structure of Management Information System (Mis)Document18 pagesStructure of Management Information System (Mis)Apoorva MishraNo ratings yet

- Data Mart - Mining.warehouseDocument1 pageData Mart - Mining.warehouseChen Hung YangNo ratings yet

- Sap (TSCM60)Document12 pagesSap (TSCM60)Raj Kumar0% (1)

- Overview of Transaction Processing and Enterprise Resource Planning SystemsDocument23 pagesOverview of Transaction Processing and Enterprise Resource Planning SystemsrresaNo ratings yet

- Cpa Business Data Analytics Syllabus Provisional VersionDocument4 pagesCpa Business Data Analytics Syllabus Provisional VersionEvans KiplagatNo ratings yet

- Ais ReviewerDocument3 pagesAis Reviewerinkai1485No ratings yet

- IT FOR MANAGERS Digi 2Document10 pagesIT FOR MANAGERS Digi 2Naveen RavichandranNo ratings yet

- AIS Chapter 2Document28 pagesAIS Chapter 2Shopno ChuraNo ratings yet

- Internal Flows of InformationDocument3 pagesInternal Flows of InformationKrisshaNo ratings yet

- Management Information SystemDocument14 pagesManagement Information SystemJhonnelyn AlvesorNo ratings yet

- CH2: Overview of TPS and ERP SystemsDocument11 pagesCH2: Overview of TPS and ERP SystemsNigussie BerhanuNo ratings yet

- Full Course AISDocument121 pagesFull Course AISAHMED ABDALLAHNo ratings yet

- 3.4 Notes Easy NotesDocument91 pages3.4 Notes Easy Notesapi-3813392No ratings yet

- SAPDocument18 pagesSAPRaj KumarNo ratings yet

- Zero To Mastery In Cybersecurity- Become Zero To Hero In Cybersecurity, This Cybersecurity Book Covers A-Z Cybersecurity Concepts, 2022 Latest EditionFrom EverandZero To Mastery In Cybersecurity- Become Zero To Hero In Cybersecurity, This Cybersecurity Book Covers A-Z Cybersecurity Concepts, 2022 Latest EditionNo ratings yet

- Knowledge PDFDocument2 pagesKnowledge PDFthrisawan bunsiritawesupNo ratings yet

- EDP Summary PDFDocument6 pagesEDP Summary PDFthrisawan bunsiritawesupNo ratings yet

- Seminar Assignment PDFDocument2 pagesSeminar Assignment PDFthrisawan bunsiritawesupNo ratings yet

- Audit Report Case 5 - Group1 PDFDocument3 pagesAudit Report Case 5 - Group1 PDFthrisawan bunsiritawesupNo ratings yet

- FCMDocument9 pagesFCMCrissa SamsamanNo ratings yet

- Supply Chain Inventory Production Planning Exam Prep OralDocument53 pagesSupply Chain Inventory Production Planning Exam Prep OralCorinaCiobanuNo ratings yet

- Integrated Review May 2020 Batch Second Monthly Exams AfarDocument94 pagesIntegrated Review May 2020 Batch Second Monthly Exams AfarKriztle Kate Gelogo100% (5)

- Vidhey Patel ResumeDocument2 pagesVidhey Patel ResumeadelaideglxNo ratings yet

- Group Assignment Supply Chain Management. Nabeel Munir, Muhammad Amin, Faizan Mustaq, Arslan AliDocument7 pagesGroup Assignment Supply Chain Management. Nabeel Munir, Muhammad Amin, Faizan Mustaq, Arslan AliNabil MuneerNo ratings yet

- MS 3406 Short-Term Budgeting Additional Financing Needed and ForecastingDocument7 pagesMS 3406 Short-Term Budgeting Additional Financing Needed and ForecastingMonica GarciaNo ratings yet

- Business Intelligence and Inventory A Case Study of Dicks Sporting Goods 29-06-2007Document17 pagesBusiness Intelligence and Inventory A Case Study of Dicks Sporting Goods 29-06-2007posnirohaNo ratings yet

- Intercompany Profit Transactions - 02.20.18Document36 pagesIntercompany Profit Transactions - 02.20.18Venz LacreNo ratings yet

- Qualifying Exam Reviewer 2017 - CostDocument12 pagesQualifying Exam Reviewer 2017 - CostAdrian Francis100% (1)

- Ch01 Managerial Accounting and The Business EnvironmentDocument8 pagesCh01 Managerial Accounting and The Business Environmentsat satwNo ratings yet

- Sd4 Sales Order ProcessingDocument110 pagesSd4 Sales Order Processingdbedada100% (1)

- AP Review MateiralDocument15 pagesAP Review MateiralAntonette Eve CelomineNo ratings yet

- PDF DocumentDocument2 pagesPDF DocumentlxNo ratings yet

- Case of Parathe Wala V2.3Document5 pagesCase of Parathe Wala V2.3sourav singhNo ratings yet

- Final Project Report - AIS - Group 5 - Payroll Udh RevisiDocument32 pagesFinal Project Report - AIS - Group 5 - Payroll Udh RevisiZakyaNo ratings yet

- Inventory Valuation Practices by Ceramics Companies in BangladeshDocument12 pagesInventory Valuation Practices by Ceramics Companies in BangladeshNahid Hasan TusharNo ratings yet

- SD QuestDocument30 pagesSD Questhermessag79No ratings yet

- AP 2001 - Students PDFDocument15 pagesAP 2001 - Students PDFdave excelleNo ratings yet

- Revenue RecognitionDocument23 pagesRevenue Recognitiongst.newofficecaNo ratings yet

- A Case Study of Just-In-Time System in Service IndustryDocument5 pagesA Case Study of Just-In-Time System in Service IndustrylalsinghNo ratings yet

- FIN202 Individual Assignment Pham Van Phung IB1501Document9 pagesFIN202 Individual Assignment Pham Van Phung IB1501Pham Van Phung - K15 FUG CTNo ratings yet

- Manage-Working Capital Management of Paper Mills-K MadhaviDocument10 pagesManage-Working Capital Management of Paper Mills-K MadhaviImpact JournalsNo ratings yet

- Supply Chain Analytics Using Data To Optimise SuppDocument47 pagesSupply Chain Analytics Using Data To Optimise Suppgoutam1235No ratings yet

- Inventory Fundamentals. CH 4pptxDocument30 pagesInventory Fundamentals. CH 4pptxRdon KhalidNo ratings yet

- Data Migration Strategy DocumentDocument18 pagesData Migration Strategy DocumentGurram SrihariNo ratings yet

- Dell Case AnalysisDocument5 pagesDell Case Analysismanindra1kondaNo ratings yet

- 2 3 2017 InventoriesDocument3 pages2 3 2017 InventoriesMr. CopernicusNo ratings yet

- Financial and Managerial Accounting 10th Edition Needles Test BankDocument39 pagesFinancial and Managerial Accounting 10th Edition Needles Test Bankindocileexothecawtoy100% (14)

- MaintenanceTechnology Mtseptember2016Document93 pagesMaintenanceTechnology Mtseptember2016Cristian Javier SierraNo ratings yet

- USAID ADS 303mavDocument17 pagesUSAID ADS 303mavJaps HattaNo ratings yet