You might also like

- Accounting in ActionDocument31 pagesAccounting in ActionTasim IshraqueNo ratings yet

- Notes - Unit-1Document13 pagesNotes - Unit-1happy lifeNo ratings yet

- Block-1 Accounting FundamentalsDocument130 pagesBlock-1 Accounting Fundamentalssuraj989108No ratings yet

- Acc407 - 406 Chapter 1 Introduction To AccountingDocument17 pagesAcc407 - 406 Chapter 1 Introduction To AccountingNurul Fatimah PajarNo ratings yet

- Funda Chapter 1 Introduction To Accounting - 174e468eDocument15 pagesFunda Chapter 1 Introduction To Accounting - 174e468eRimuruNo ratings yet

- 1. AccountingDocument336 pages1. Accountingsparsh24computerNo ratings yet

- Accounting 101Document4 pagesAccounting 101Cheche AmpoanNo ratings yet

- BASIC ACCOUNTINGDocument36 pagesBASIC ACCOUNTINGKawaii SevennNo ratings yet

- ACCOUNTING KEY CONCEPTS AND CONVENTIONSDocument25 pagesACCOUNTING KEY CONCEPTS AND CONVENTIONSawaezNo ratings yet

- CHAPTER 1 (Lecture Notes)Document20 pagesCHAPTER 1 (Lecture Notes)Nor Farhanah NanaNo ratings yet

- Chapter 1Document15 pagesChapter 1Muqri SyahmiNo ratings yet

- Internal Control of Fixed Assets: A Controller and Auditor's GuideFrom EverandInternal Control of Fixed Assets: A Controller and Auditor's GuideRating: 4 out of 5 stars4/5 (1)

- Accounting NotesDocument22 pagesAccounting NotesSrikanth Vasantada50% (2)

- Primitive Accounting Middle Ages Industrial Revolution & Corporate Organization Information AgeDocument28 pagesPrimitive Accounting Middle Ages Industrial Revolution & Corporate Organization Information AgePhil Cahilig-GariginovichNo ratings yet

- Learning Objctives Basic Concepts in Accounting Journal Ledger Cash Books Trial Balance Preperation of Finan AccountsDocument23 pagesLearning Objctives Basic Concepts in Accounting Journal Ledger Cash Books Trial Balance Preperation of Finan Accounts254452No ratings yet

- Chapter One Accfundmental IDocument70 pagesChapter One Accfundmental IMujib AbdlhadiNo ratings yet

- 01 Introduction To Accounting, Types of Information Users, and Forms of Business OrganizationDocument55 pages01 Introduction To Accounting, Types of Information Users, and Forms of Business Organizationhailee hueNo ratings yet

- Accounting 12 Module 1Document12 pagesAccounting 12 Module 1Kristy Veyna BautistaNo ratings yet

- Mefa Unit 5Document32 pagesMefa Unit 5Saalif RahmanNo ratings yet

- Conceptual Framework and Accounting StandardsDocument142 pagesConceptual Framework and Accounting StandardsAni TubeNo ratings yet

- Accounting Principles (BUS 505)Document71 pagesAccounting Principles (BUS 505)S. M. Fahmidunnabi 2035150660No ratings yet

- BAC 813 - Financial Accounting Premium Notes - Elab Notes LibraryDocument111 pagesBAC 813 - Financial Accounting Premium Notes - Elab Notes LibraryWachirajaneNo ratings yet

- Revised Accounting For LawyersDocument67 pagesRevised Accounting For Lawyersvinay rakshithNo ratings yet

- Book-Keeping & AccountancyDocument70 pagesBook-Keeping & AccountancyIstiaqueNo ratings yet

- Accounting As A Form Of: CommunicationDocument12 pagesAccounting As A Form Of: Communicationnavin9849No ratings yet

- Ac 1&2 Module 1Document11 pagesAc 1&2 Module 1ABM-5 Lance Angelo SuganobNo ratings yet

- Conceptual Framework and Accounting Standards: Freya Wyan Silva-Dela Cruz, Cpa, MbaDocument27 pagesConceptual Framework and Accounting Standards: Freya Wyan Silva-Dela Cruz, Cpa, MbaRegine Alesna AlcoberNo ratings yet

- Lecture 1 - Introduction To AccountingDocument12 pagesLecture 1 - Introduction To AccountingmallarilecarNo ratings yet

- Preparing Financial Stat. Cemba 560Document172 pagesPreparing Financial Stat. Cemba 560nanapet80No ratings yet

- CU DR Balwinder Singh 03112022 PDFDocument64 pagesCU DR Balwinder Singh 03112022 PDFAkshat Sharma Roll no 21No ratings yet

- Questions and AnswersDocument147 pagesQuestions and AnswersNica Joy AsutillaNo ratings yet

- Understand Business Changes and OrganizationsDocument12 pagesUnderstand Business Changes and OrganizationsHeart EuniceNo ratings yet

- Accounting Principles (BUS 505)Document71 pagesAccounting Principles (BUS 505)Md. Saadman Sakib 2115420660No ratings yet

- Introduction To Accounting - UnknownDocument159 pagesIntroduction To Accounting - UnknownArun Soman100% (1)

- Accounting As A SystemDocument20 pagesAccounting As A SystemSovashnie PersaudNo ratings yet

- Introduction to Accounting - Define Accounting, Financial Statements, and Forms of BusinessDocument24 pagesIntroduction to Accounting - Define Accounting, Financial Statements, and Forms of BusinessNasha MatRomNo ratings yet

- Mgt101 Short NotesDocument15 pagesMgt101 Short NotesUsman AliNo ratings yet

- Full Download Cornerstones of Financial Accounting Canadian 2nd Edition Rich Solutions ManualDocument36 pagesFull Download Cornerstones of Financial Accounting Canadian 2nd Edition Rich Solutions Manualcolagiovannibeckah100% (28)

- Lecture - 1 - Accounting - in - Business - NUS ACC1002 2020 Spring PostDocument42 pagesLecture - 1 - Accounting - in - Business - NUS ACC1002 2020 Spring PostZenyui100% (1)

- ACCT 1026 Lesson ONEDocument13 pagesACCT 1026 Lesson ONEAnnie RapanutNo ratings yet

- Introduction To Accounting Learning ObjectivesDocument20 pagesIntroduction To Accounting Learning ObjectivesSABORDO, MA. KRISTINA COLEENNo ratings yet

- Unit 1 - Introduction To Principles of AccountingDocument100 pagesUnit 1 - Introduction To Principles of AccountingNgonga FumbeloNo ratings yet

- Online Accounting Lesson for Financial ReportingDocument52 pagesOnline Accounting Lesson for Financial ReportingAnnie RapanutNo ratings yet

- I Introduction To AccountingDocument9 pagesI Introduction To AccountingDirck VerraNo ratings yet

- 10business Module4 AccountingDocument117 pages10business Module4 Accountingchris100% (1)

- Review On Fundamentals of AccountingDocument18 pagesReview On Fundamentals of AccountingFat AjummaNo ratings yet

- Introduction To AccountingDocument13 pagesIntroduction To AccountingGrow GlutesNo ratings yet

- CHAPTER 1 - Introduction To AccountingDocument15 pagesCHAPTER 1 - Introduction To AccountingMuhammad AdibNo ratings yet

- Presentation1 GovtaccDocument39 pagesPresentation1 GovtaccBorisagar HarshNo ratings yet

- 11ACC1.1 - 2023 - Conceptual Basis of AccountingDocument18 pages11ACC1.1 - 2023 - Conceptual Basis of AccountingJanice BaltorNo ratings yet

- Introduction to Accounting FundamentalsDocument199 pagesIntroduction to Accounting FundamentalsSonakshi Behl61% (69)

- Accounts Volume 1Document503 pagesAccounts Volume 1Utkarsh100% (1)

- FABM 1 Fundamentals of Accountancy, Business and ManagementDocument28 pagesFABM 1 Fundamentals of Accountancy, Business and ManagementLiya Mae SantiagoNo ratings yet

- AccountingDocument339 pagesAccountingShaik Basha100% (3)

- t14 Presentation Koh Kah Fong 1904558Document9 pagest14 Presentation Koh Kah Fong 1904558Jeff KohNo ratings yet

- Part 1 Introduction to AccountingDocument67 pagesPart 1 Introduction to AccountingDONALD GUTIERREZNo ratings yet

- Introduction to Accounting FundamentalsDocument11 pagesIntroduction to Accounting FundamentalsNUR ANIS SYAMIMI BINTI MUSTAFA / UPMNo ratings yet

- Plus One Accountancy With CA Focus Area-2021 Notes & Expected Q&AsDocument140 pagesPlus One Accountancy With CA Focus Area-2021 Notes & Expected Q&Ashadiyxx100% (1)

- Intercompany Transactions ConsolidationDocument1 pageIntercompany Transactions ConsolidationErjohn Papa0% (1)

- Accounting Information: Accounting Information: Users and UsesDocument25 pagesAccounting Information: Accounting Information: Users and UsesBa Quy100% (2)

- Ch04 6e Slutions HoyleDocument44 pagesCh04 6e Slutions HoyleJackie PerezNo ratings yet

- Accounting For Manager Complete NotesDocument105 pagesAccounting For Manager Complete NotesAARTI100% (2)

- HMWK 12Document8 pagesHMWK 12macmac29No ratings yet

- Statement of Cash Flows ExplainedDocument61 pagesStatement of Cash Flows ExplainedMuhammad RezaNo ratings yet

- 20190831041657SLCHIA005FR1 Intro To FRDocument113 pages20190831041657SLCHIA005FR1 Intro To FRNadiaIssabellaNo ratings yet

- Statement of Cash Flow Analysis: Kathmandu University School of Management (KUSOM)Document61 pagesStatement of Cash Flow Analysis: Kathmandu University School of Management (KUSOM)ginish12No ratings yet

- Notes To The Financial Statements: 1. General InformationDocument46 pagesNotes To The Financial Statements: 1. General InformationyasinNo ratings yet

- BPP - Learning - Media - Catalogue - Jan - Jun - 2014 - WEB2 PDFDocument47 pagesBPP - Learning - Media - Catalogue - Jan - Jun - 2014 - WEB2 PDFramprasad268No ratings yet

- ch02 NewDocument4 pagesch02 NewShakoor QaziNo ratings yet

- Solutions To B Exercises: Kieso, (For Instructor Use Only)Document7 pagesSolutions To B Exercises: Kieso, (For Instructor Use Only)Jogja AntiqNo ratings yet

- Government Auditing and Accounting For NPODocument65 pagesGovernment Auditing and Accounting For NPOAljon Fabrigas SalacNo ratings yet

- ACCOUNTS Secret SauseDocument71 pagesACCOUNTS Secret SauseDesi TVNo ratings yet

- Chap6 PDFDocument46 pagesChap6 PDFعبدالله ماجد المطارنهNo ratings yet

- Research Paper On Financial Analysis of BanksDocument5 pagesResearch Paper On Financial Analysis of Banksc9rvcwhf100% (1)

- Auditing Theory MCQsDocument21 pagesAuditing Theory MCQsDawn Caldeira100% (1)

- Financial Planning and Forecasting Brigham SolutionDocument29 pagesFinancial Planning and Forecasting Brigham SolutionShahid Mehmood100% (6)

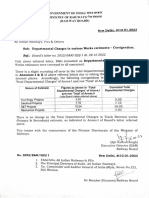

- Corrigendum of Departmental ChargesDocument1 pageCorrigendum of Departmental ChargesADEE G GRCNo ratings yet

- A Compendium of Standards On Internal AuditingDocument2 pagesA Compendium of Standards On Internal AuditingmurthyeNo ratings yet

- Elisa Beauty SalonDocument6 pagesElisa Beauty SalonAnanda DwilestariNo ratings yet

- SAP ERP Financial Manual - 1 During SAP Training at SIEMENS Academy - November-2014Document87 pagesSAP ERP Financial Manual - 1 During SAP Training at SIEMENS Academy - November-2014Krushna SwainNo ratings yet

- Chart of Accounts Assets Liabilities Owner'S Equity Income ExpensesDocument2 pagesChart of Accounts Assets Liabilities Owner'S Equity Income ExpensesErika Bucao100% (1)

- Fourth Year - Collective File FinalDocument27 pagesFourth Year - Collective File FinalAhmed GamalNo ratings yet

- Final SLP Accounting For ReceivablesDocument26 pagesFinal SLP Accounting For ReceivablesLovely Joy SantiagoNo ratings yet

- Lembar Kerja Edit LilisDocument11 pagesLembar Kerja Edit LilisAyu WidyaNo ratings yet

- Scott - Chapter 13 - Standard Setting and Political IssuesDocument8 pagesScott - Chapter 13 - Standard Setting and Political IssuesIvonne WijayaNo ratings yet

- Branch Accounting by Rahul NegiDocument10 pagesBranch Accounting by Rahul NegiGadgetsgramNo ratings yet

- 7 Internal and External Audit RolesDocument10 pages7 Internal and External Audit RolesJOSÉ IGNACIO PARRA VALENZUELANo ratings yet

- MAS Lecture Variable CostingDocument8 pagesMAS Lecture Variable CostingLhoel Delremedios100% (1)