You might also like

- BlackBook Moin Roll No 39 Review of Literature 1Document18 pagesBlackBook Moin Roll No 39 Review of Literature 1Pokemongo helpingspooferNo ratings yet

- Impact of Gst on Hotel Industry - Vedanti PedamkarDocument71 pagesImpact of Gst on Hotel Industry - Vedanti Pedamkargoswamiharish666No ratings yet

- How to Handle Goods and Service Tax (GST)From EverandHow to Handle Goods and Service Tax (GST)Rating: 4.5 out of 5 stars4.5/5 (4)

- Mba ProjectDocument401 pagesMba Projectgani829670No ratings yet

- UPSC Exam Preparation: Gist of Yojana August - Goods and Services TaxDocument11 pagesUPSC Exam Preparation: Gist of Yojana August - Goods and Services TaxAbhijai RajNo ratings yet

- Goods and Services Tax Act and Its Impact On GDPDocument28 pagesGoods and Services Tax Act and Its Impact On GDPArshi Asif100% (3)

- Goods and Services Tax Act and Its Impact On GDPDocument28 pagesGoods and Services Tax Act and Its Impact On GDPArshi Asif50% (2)

- Christ RespondentDocument8 pagesChrist RespondentShekharNo ratings yet

- GST as a major source of indirect tax revenue for the Indian governmentDocument7 pagesGST as a major source of indirect tax revenue for the Indian governmentStudy AllyNo ratings yet

- GST VS VatDocument62 pagesGST VS VatMohit AgarwalNo ratings yet

- Ashish TaxDocument20 pagesAshish TaxAshish RajNo ratings yet

- GST Questions & Answers PDF | Latest Banking AwarenessDocument6 pagesGST Questions & Answers PDF | Latest Banking AwarenessAnkita GhogaleNo ratings yet

- GST vs VAT: Key differences between the two indirect tax systemsDocument5 pagesGST vs VAT: Key differences between the two indirect tax systemsSkArbazNo ratings yet

- Vat + GSTDocument6 pagesVat + GSTDisha DahiyaNo ratings yet

- A Short Case Study On The Ten Principles of EconomicsDocument8 pagesA Short Case Study On The Ten Principles of EconomicsRaunak ThakerNo ratings yet

- Insight EconomicsDocument50 pagesInsight EconomicsMohit GautamNo ratings yet

- INCOME TAX AND GST. JURAZ-Module 3Document11 pagesINCOME TAX AND GST. JURAZ-Module 3hisanashanutty2004100% (1)

- GST (Goods & Service Tax: Submitted by Nikita Sawant 44 Aditya Kadam 22Document19 pagesGST (Goods & Service Tax: Submitted by Nikita Sawant 44 Aditya Kadam 22Balkrushna ShingareNo ratings yet

- GST Final IDUDocument10 pagesGST Final IDUmandeep kaurNo ratings yet

- Introduction To GSTDocument14 pagesIntroduction To GSTAadil KakarNo ratings yet

- A Study On Implementation and Impact of GSTDocument15 pagesA Study On Implementation and Impact of GSTAmirtha RathinaveluNo ratings yet

- GST-1Document26 pagesGST-1pranaynagrale876No ratings yet

- CTP AssignmentDocument10 pagesCTP AssignmentANIL KUMARNo ratings yet

- DraftDocument36 pagesDraftAbhinand SadhanandanNo ratings yet

- Compendium On GSTDocument5 pagesCompendium On GSTSumit KumarNo ratings yet

- Tax System - 1st - CH - EcoDocument6 pagesTax System - 1st - CH - EcoRaju RaviNo ratings yet

- Title:Gst: TH TH NDDocument5 pagesTitle:Gst: TH TH NDNAMRATA BHATIANo ratings yet

- GST to Improve E-Commerce in IndiaDocument5 pagesGST to Improve E-Commerce in IndiaNAMRATA BHATIANo ratings yet

- Title:Gst: TH TH NDDocument5 pagesTitle:Gst: TH TH NDNAMRATA BHATIANo ratings yet

- GST Challenges and ImpactDocument5 pagesGST Challenges and ImpactSarika Chaturvedi100% (1)

- GST AssgmntDocument16 pagesGST AssgmntMuhammed Samil MusthafaNo ratings yet

- Sitanshu_1182190038-Tax Laws RPDocument12 pagesSitanshu_1182190038-Tax Laws RPSitanshu SrivastavaNo ratings yet

- Constitutional Basis of GSTDocument10 pagesConstitutional Basis of GSTNANDINI RAJ N RNo ratings yet

- The Goods and Services Tax and Its Likely Impact On Indian EconomyDocument8 pagesThe Goods and Services Tax and Its Likely Impact On Indian Economyaryaa_statNo ratings yet

- GST or Goods and Services Tax Can Be Rightfully Called The Largest IndirectDocument26 pagesGST or Goods and Services Tax Can Be Rightfully Called The Largest IndirectDevesh SharmaNo ratings yet

- GST IntroductionDocument103 pagesGST IntroductionAnonymous MhCdtwxQINo ratings yet

- GST ProjectDocument42 pagesGST Projectharmisha narshanaNo ratings yet

- GST PDFDocument7 pagesGST PDFShekhar singhNo ratings yet

- A Review On GST Execution and Its Effect PDFDocument9 pagesA Review On GST Execution and Its Effect PDFAsma KhanNo ratings yet

- Goods Service TaxDocument3 pagesGoods Service TaxBrunoCruizeNo ratings yet

- Understanding India's GST: Impact and AnalysisDocument13 pagesUnderstanding India's GST: Impact and Analysispj04No ratings yet

- Tax Law - 7th SemDocument16 pagesTax Law - 7th SemIzaan RizviNo ratings yet

- Indirect Taxes: Assignment-2Document27 pagesIndirect Taxes: Assignment-2Arpita ArtaniNo ratings yet

- Project 3Document17 pagesProject 3Hemant MandalNo ratings yet

- GST NotesDocument2 pagesGST NotesVinayak UmraniNo ratings yet

- Understanding India's Indirect Tax StructureDocument73 pagesUnderstanding India's Indirect Tax StructureKautilya VithobaNo ratings yet

- Impact of GST on Small Businesses in DamanDocument33 pagesImpact of GST on Small Businesses in DamanSawan PatelNo ratings yet

- Concept Of: Goods & Service TaxDocument23 pagesConcept Of: Goods & Service Taxraginikumarithakur45No ratings yet

- GST Impact on MSMEs with Case Study of Vinayaka EnterpriseDocument42 pagesGST Impact on MSMEs with Case Study of Vinayaka EnterpriseMegha R57% (7)

- GST The Game Changer: GST Will Be A Game Changing Reform For Indian Economy byDocument6 pagesGST The Game Changer: GST Will Be A Game Changing Reform For Indian Economy bySiddiqui AdamNo ratings yet

- GST Introduction and List of Taxes It SubsumedDocument16 pagesGST Introduction and List of Taxes It SubsumedTrippy MindNo ratings yet

- Lect02 - GST Theroy and NumericalsDocument11 pagesLect02 - GST Theroy and Numericalsabdulraqeeb alareqiNo ratings yet

- Goods and Service TaxDocument3 pagesGoods and Service TaxJuhi BansalNo ratings yet

- 2.1 Method of Collecting Data Primary DataDocument8 pages2.1 Method of Collecting Data Primary Datadeepak sipaniNo ratings yet

- Types of Taxes Under GSTDocument4 pagesTypes of Taxes Under GSTDiya SharmaNo ratings yet

- GST What Is GST in India?Document4 pagesGST What Is GST in India?ayushNo ratings yet

- A Report On Goods and Services TaxDocument10 pagesA Report On Goods and Services TaxRashmi SinghNo ratings yet

- Till Now The Date of Implementation Has Been Pushed Beyond From 01/04/2011 To May Be 1st October 2011 or 1st April 2012.Document3 pagesTill Now The Date of Implementation Has Been Pushed Beyond From 01/04/2011 To May Be 1st October 2011 or 1st April 2012.Ankit BagariaNo ratings yet

- GST BillDocument20 pagesGST BillshivenNo ratings yet

- Tax Law IIDocument20 pagesTax Law IIaffan QureshiNo ratings yet

- 0601 Wuefh 97 RDocument30 pages0601 Wuefh 97 RPokemongo helpingspooferNo ratings yet

- Gaming Esports Startup PlanDocument1 pageGaming Esports Startup PlanPokemongo helpingspooferNo ratings yet

- BlackBook Shreyash Shinde Roll No 39 INTRODUCTIONDocument24 pagesBlackBook Shreyash Shinde Roll No 39 INTRODUCTIONPokemongo helpingspooferNo ratings yet

- BlackBook Shreyash Shinde Roll No 39 Review of Literature 1Document21 pagesBlackBook Shreyash Shinde Roll No 39 Review of Literature 1Pokemongo helpingspooferNo ratings yet

- Blackbook Roll No 39 Shreyash Shinde NewDocument25 pagesBlackbook Roll No 39 Shreyash Shinde NewPokemongo helpingspooferNo ratings yet

- Perspective of People About Investment in Real Estate SectorDocument8 pagesPerspective of People About Investment in Real Estate SectorPokemongo helpingspooferNo ratings yet

- BlackBook Shreyash Shinde Roll No 39 Review of LiteratureDocument11 pagesBlackBook Shreyash Shinde Roll No 39 Review of LiteraturePokemongo helpingspooferNo ratings yet

- Faster Construction Development Through ReitsDocument17 pagesFaster Construction Development Through Reitsnaheed samiNo ratings yet

- Volume 8 Issue 2 July - December 2016Document82 pagesVolume 8 Issue 2 July - December 2016Pokemongo helpingspooferNo ratings yet

- Question CMA June 2019Document6 pagesQuestion CMA June 2019rumelrashid_seuNo ratings yet

- Digital Marketing Helps Retail CRMDocument11 pagesDigital Marketing Helps Retail CRMEnjila AnjilNo ratings yet

- Analysis of Global EnvironmentDocument3 pagesAnalysis of Global EnvironmenthanumanthaiahgowdaNo ratings yet

- Unit 2: Marketing EnvironmentDocument22 pagesUnit 2: Marketing Environmentअभिषेक रेग्मीNo ratings yet

- ATP Term PaperDocument12 pagesATP Term PaperCarme Ann S. RollonNo ratings yet

- N5 Economics June 2021Document10 pagesN5 Economics June 2021Honorine Ngum NibaNo ratings yet

- Advertising Process and ParticipantsDocument12 pagesAdvertising Process and ParticipantsV A100% (1)

- ResearchDocument14 pagesResearchJohnBanda100% (1)

- Marketing Cost and Profitability AnalysisDocument39 pagesMarketing Cost and Profitability AnalysisShahid Ashraf100% (3)

- Santos ECO Fin HW04Document6 pagesSantos ECO Fin HW04deanyangg25No ratings yet

- Synopsis - Analytic Study On Customer SatisfactionDocument8 pagesSynopsis - Analytic Study On Customer SatisfactionAnurag Singh50% (2)

- Better Business 5th Edition Solomon Solutions ManualDocument26 pagesBetter Business 5th Edition Solomon Solutions ManualChelseaHernandezbnjf100% (51)

- Singapore City Skyline at Night PowerPoint Template #54219Document20 pagesSingapore City Skyline at Night PowerPoint Template #54219Faaz ZubairNo ratings yet

- Questions Chapter 16 FinanceDocument23 pagesQuestions Chapter 16 FinanceJJNo ratings yet

- Concepts of Quality, Total Quality and Total Quality ManagementDocument3 pagesConcepts of Quality, Total Quality and Total Quality Managementbshm thirdNo ratings yet

- Day Trading Strategies For Stock and Forex Markets Free PDFDocument9 pagesDay Trading Strategies For Stock and Forex Markets Free PDFAmit KumarNo ratings yet

- OfferletterDocument2 pagesOfferletterpakada8460No ratings yet

- ASSIGNMENT BBAW2103 - Financial AccountingDocument13 pagesASSIGNMENT BBAW2103 - Financial AccountingMUHAMMAD NAJIB BIN HAMBALI STUDENTNo ratings yet

- Analisis Saluran Pemasaran Terintegrasi UMKM Badii Farm Purwakarta Dalam Meningkatkan Volume PenjualanDocument7 pagesAnalisis Saluran Pemasaran Terintegrasi UMKM Badii Farm Purwakarta Dalam Meningkatkan Volume PenjualanTaniaNo ratings yet

- Exercise 12-8 Intangible AssetsDocument2 pagesExercise 12-8 Intangible AssetsJay LazaroNo ratings yet

- 112380-237973 20190331 PDFDocument5 pages112380-237973 20190331 PDFKutty KausyNo ratings yet

- HRMP and ToiDocument29 pagesHRMP and ToiMuhammad Tanzeel Qaisar DogarNo ratings yet

- Project Procurement Management - PPTDocument15 pagesProject Procurement Management - PPTHappy100% (2)

- 3.1 Money and Finance New Book: Money and Banking: Igcse /O Level EconomicsDocument17 pages3.1 Money and Finance New Book: Money and Banking: Igcse /O Level EconomicsJoe Amirtham100% (1)

- Venture Capital - PlayersDocument14 pagesVenture Capital - PlayersjNo ratings yet

- ICICI Balanced Advantage Fund - One PagerDocument2 pagesICICI Balanced Advantage Fund - One PagerjoycoolNo ratings yet

- Kaldor'S Growth Theory Nancy J. WulwickDocument19 pagesKaldor'S Growth Theory Nancy J. WulwickTeisu IftiNo ratings yet

- Fundamentals of the Indian Capital MarketDocument37 pagesFundamentals of the Indian Capital MarketBharat TailorNo ratings yet

- Application Form 8170323004780 PDFDocument4 pagesApplication Form 8170323004780 PDFMIS PROCESSNo ratings yet

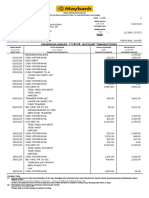

- TransactionSummary 915020007543226 160523031507-q4Document1 pageTransactionSummary 915020007543226 160523031507-q4RAJNo ratings yet