You might also like

- Accounting Standard 26 - Intangible Assets Issuing Authority: Status: Effective DateDocument6 pagesAccounting Standard 26 - Intangible Assets Issuing Authority: Status: Effective DatePiyush AgarwalNo ratings yet

- Chapter 21 INTANGIBLE ASSSETSDocument38 pagesChapter 21 INTANGIBLE ASSSETSmarj ponceNo ratings yet

- Ind As 38Document14 pagesInd As 38Juthika Bora100% (1)

- Advance AccountsDocument6 pagesAdvance Accountsashish.jhaa756No ratings yet

- AP.1205B Intangible-Assets-W HIGHLIGHTSDocument16 pagesAP.1205B Intangible-Assets-W HIGHLIGHTSdave excelleNo ratings yet

- Class Note 6 - Intangible AssetsDocument5 pagesClass Note 6 - Intangible AssetsMarlon SmithNo ratings yet

- Accounting Research Memo Proj Acct 540Document9 pagesAccounting Research Memo Proj Acct 540Carolyn Robinson WhitlockNo ratings yet

- IAS 38 Intangible AssetsDocument29 pagesIAS 38 Intangible Assetsdương nguyễn vũ thùyNo ratings yet

- Accounting Standard 6Document208 pagesAccounting Standard 6aanu1234No ratings yet

- Farap 4505Document7 pagesFarap 4505Marya NvlzNo ratings yet

- Philippine Accounting Standards 38 (Intangible Assets2)Document72 pagesPhilippine Accounting Standards 38 (Intangible Assets2)Princess Edreah NuñalNo ratings yet

- 19 - Intangible AssetsDocument10 pages19 - Intangible AssetsYudna YuNo ratings yet

- Accounting GuidanceDocument5 pagesAccounting GuidanceVibha MittalNo ratings yet

- Module 14 PAS 38Document5 pagesModule 14 PAS 38Jan JanNo ratings yet

- Ias 38Document7 pagesIas 38Researcher BrianNo ratings yet

- Module 4 - INTACC2 Intangible AssetsDocument20 pagesModule 4 - INTACC2 Intangible AssetsKhan TanNo ratings yet

- TOPIC 26 IAS 38 Intangible AssetsDocument7 pagesTOPIC 26 IAS 38 Intangible AssetsNameNo ratings yet

- 10.11 AS 26 Intangible AssetsDocument5 pages10.11 AS 26 Intangible AssetsAnakin SkywalkerNo ratings yet

- Fixed AssetsDocument46 pagesFixed AssetsSprancenatu Lavinia0% (1)

- Accounting PoliciesDocument3 pagesAccounting PoliciesSatish Ranjan PradhanNo ratings yet

- Ias 16 PropertyDocument11 pagesIas 16 PropertyFolarin EmmanuelNo ratings yet

- Ias 38Document33 pagesIas 38Reever River100% (1)

- Accounting For Property, Plant and Equipment, Intangibles and Impairment of Assets Week 12-13 AssessmentsDocument13 pagesAccounting For Property, Plant and Equipment, Intangibles and Impairment of Assets Week 12-13 AssessmentsAllia LandigNo ratings yet

- Chapter 11 Intagible AssetsDocument5 pagesChapter 11 Intagible Assetsmaria isabellaNo ratings yet

- Week 5 C35 - MFRS 138 IntangiblesDocument26 pagesWeek 5 C35 - MFRS 138 IntangiblesYong Arifin0% (1)

- AS 26 - 123 To 138Document16 pagesAS 26 - 123 To 138love chawlaNo ratings yet

- IND As SummaryDocument41 pagesIND As SummaryAishwarya RajeshNo ratings yet

- Accounting Policy As Per FSDocument17 pagesAccounting Policy As Per FSShubham TiwariNo ratings yet

- ASSIGNMENTDocument7 pagesASSIGNMENTRahulNo ratings yet

- Chapter 20Document25 pagesChapter 20Crysta LeeNo ratings yet

- Ias16, 23, 36, 38, 40 and Ifrs 3Document71 pagesIas16, 23, 36, 38, 40 and Ifrs 3mulualemNo ratings yet

- Accounting StandardsDocument26 pagesAccounting StandardsAbhishek Chaturvedi100% (1)

- Accounting Standard of Mahindra and Mahindra LTDDocument9 pagesAccounting Standard of Mahindra and Mahindra LTDDheeraj shettyNo ratings yet

- Lect 08TVDocument29 pagesLect 08TVsalman siddiquiNo ratings yet

- Name:-Akash Jaiswal ROLL NO.:-0645 ROOM NO.:-045 SESSION:-2014-2017 Topic:-Accounting For FixedDocument6 pagesName:-Akash Jaiswal ROLL NO.:-0645 ROOM NO.:-045 SESSION:-2014-2017 Topic:-Accounting For FixedAKASH JAISWALNo ratings yet

- LESSON3Document19 pagesLESSON3Ira Charisse BurlaosNo ratings yet

- As-26 Intangible AssetsDocument14 pagesAs-26 Intangible AssetssaikrishnaNo ratings yet

- Accounting Standaed FinalDocument6 pagesAccounting Standaed FinalPrachee MulyeNo ratings yet

- Pas 38 - Intangible AssetsDocument6 pagesPas 38 - Intangible AssetsJessie ForpublicuseNo ratings yet

- Module 7 IntangiblesDocument14 pagesModule 7 IntangiblesEarl ENo ratings yet

- The Use of OutDocument21 pagesThe Use of OutLerato MagoroNo ratings yet

- Vistaland Intl Notes2021Document11 pagesVistaland Intl Notes2021Myda RafaelNo ratings yet

- Power Point Accounting For Patents Proj Acct 540Document24 pagesPower Point Accounting For Patents Proj Acct 540Carolyn Robinson WhitlockNo ratings yet

- PPEDocument5 pagesPPERodelia MalacastaNo ratings yet

- F7 Summary Dec 2011Document30 pagesF7 Summary Dec 2011artkodis100% (1)

- Ias 16Document9 pagesIas 16ADEYANJU AKEEMNo ratings yet

- Company Business PlanDocument24 pagesCompany Business PlanDaud Farook IINo ratings yet

- Intangible AssetsDocument6 pagesIntangible Assetsmark fernandezNo ratings yet

- Accounting Standard 26Document16 pagesAccounting Standard 26Melissa ArnoldNo ratings yet

- IAS 16 Property, Plant and EquipmentDocument4 pagesIAS 16 Property, Plant and EquipmentSelva Bavani SelwaduraiNo ratings yet

- Micro and Other Legal Entities Code of Practice: 0. Taxpayers According To The Accounting ActDocument19 pagesMicro and Other Legal Entities Code of Practice: 0. Taxpayers According To The Accounting ActIvana MatovićNo ratings yet

- Accounting StandardDocument9 pagesAccounting StandardVanshika GaneriwalNo ratings yet

- IAS 38 Intangible Assets: Technical SummaryDocument5 pagesIAS 38 Intangible Assets: Technical Summaryanon-553693100% (2)

- Ipsas 31-Intangable Assets IpsasDocument6 pagesIpsas 31-Intangable Assets IpsasSolomon MollaNo ratings yet

- Lesson 4Document23 pagesLesson 4shadowlord468No ratings yet

- Note Buổi 7Document3 pagesNote Buổi 7Long Chế Vũ BảoNo ratings yet

- Summary PpeDocument8 pagesSummary PpeJenilyn CalaraNo ratings yet

- Intangible Assets1Document22 pagesIntangible Assets1hamarshi2010No ratings yet

- Accounting Standard 10Document31 pagesAccounting Standard 10Yesha ShahNo ratings yet

- As 29 - 230219 - 160829Document2 pagesAs 29 - 230219 - 160829Prasad IngoleNo ratings yet

- As 19Document6 pagesAs 19Prasad IngoleNo ratings yet

- UntitledDocument8 pagesUntitledPrasad IngoleNo ratings yet

- Components of IFS NotesDocument6 pagesComponents of IFS NotesPrasad IngoleNo ratings yet

- Unit 1 - Indian Financial SystemDocument31 pagesUnit 1 - Indian Financial SystemPrasad IngoleNo ratings yet

- Securities MarketDocument32 pagesSecurities MarketPrasad IngoleNo ratings yet

- Great ManDocument2 pagesGreat ManPrasad IngoleNo ratings yet

- Types of Leadership StylesDocument2 pagesTypes of Leadership StylesPrasad IngoleNo ratings yet

- HistoryDocument1 pageHistoryPrasad IngoleNo ratings yet

- An ISO 9001Document3 pagesAn ISO 9001Prasad IngoleNo ratings yet

- Mall Management Is Defined As An Overall Operation and Maintenance of The Entire Building InfrastructureDocument3 pagesMall Management Is Defined As An Overall Operation and Maintenance of The Entire Building InfrastructurePrasad IngoleNo ratings yet

- Steps in Decision Making ProcessDocument2 pagesSteps in Decision Making ProcessPrasad IngoleNo ratings yet

- What Are Employee Motivation StrategiesDocument3 pagesWhat Are Employee Motivation StrategiesPrasad IngoleNo ratings yet

- Eco Apple Project 1Document4 pagesEco Apple Project 1Prasad IngoleNo ratings yet

- Satkar Auto: Spares Description SN. Spares Name Part Number Qty. Rate AmountDocument1 pageSatkar Auto: Spares Description SN. Spares Name Part Number Qty. Rate AmountSonali kambleNo ratings yet

- Consolidated Financial Statements by MR - Abdullatif EssajeeDocument37 pagesConsolidated Financial Statements by MR - Abdullatif EssajeeSantoshNo ratings yet

- Faq Economics 2019Document35 pagesFaq Economics 2019Aejaz MohamedNo ratings yet

- Test Bank - Chapter 9 Profit PlanningDocument34 pagesTest Bank - Chapter 9 Profit PlanningAiko E. Lara67% (3)

- AxiataDocument21 pagesAxiatasalihin 4646No ratings yet

- Manufacturing of Detergent Powder & CakeDocument2 pagesManufacturing of Detergent Powder & Cakeramu_uppadaNo ratings yet

- Chapter 21 Latihan SoalDocument10 pagesChapter 21 Latihan SoalJulyaniNo ratings yet

- Do The Math WorkbookDocument38 pagesDo The Math WorkbookJustin CoNo ratings yet

- Postal Manual Volume - 4.1Document72 pagesPostal Manual Volume - 4.1K V Sridharan General Secretary P3 NFPE100% (3)

- 2012 WPA by R.r.ocampo - Check FiguresDocument23 pages2012 WPA by R.r.ocampo - Check FiguresjaseyNo ratings yet

- Partnership Accounting Practical Accounting 2Document13 pagesPartnership Accounting Practical Accounting 2random17341No ratings yet

- 1857 KiDocument2 pages1857 KiAntim Arya100% (1)

- ECON1101 Summary NotesDocument31 pagesECON1101 Summary NotesPhill NamaraNo ratings yet

- Business ValuationDocument6 pagesBusiness ValuationlenoraNo ratings yet

- Business Plan Sample Pharmacy PDFDocument26 pagesBusiness Plan Sample Pharmacy PDFBeverly Caaya100% (1)

- Too Yumm 1Document2 pagesToo Yumm 1Talha KhanNo ratings yet

- Practice Class2Document1 pagePractice Class2Mutahher MuzzammilNo ratings yet

- Coca-Cola and Pepsi Economic Analysis ReportDocument39 pagesCoca-Cola and Pepsi Economic Analysis ReportJing Xiong67% (3)

- How Well Do You CompareDocument17 pagesHow Well Do You Comparerwmortell3580No ratings yet

- Worldwide Capital and Fixed Assets Guide 2016Document152 pagesWorldwide Capital and Fixed Assets Guide 2016Victor TucoNo ratings yet

- Bhartiya Post Jan 2007Document32 pagesBhartiya Post Jan 2007K V Sridharan General Secretary P3 NFPENo ratings yet

- Chapter 3 - Financial AnalysisDocument39 pagesChapter 3 - Financial AnalysisHeatstroke0% (1)

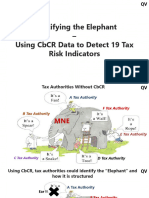

- 19 Tax Risk Indicators in CBCRDocument22 pages19 Tax Risk Indicators in CBCRidan28No ratings yet

- Arguelles Medical ClinicDocument3 pagesArguelles Medical ClinicPJ PoliranNo ratings yet

- 01 Chapter 1 Joint Venture and Public EnterpriseDocument11 pages01 Chapter 1 Joint Venture and Public EnterpriseTemesgen LealemNo ratings yet

- Macroeconomics - Mankew - Chapter 8 - Economic GrowthDocument49 pagesMacroeconomics - Mankew - Chapter 8 - Economic GrowthElis Wadi100% (1)

- J.R.a. Philippines, Inc. vs. Commissioner of Internal RevenueDocument5 pagesJ.R.a. Philippines, Inc. vs. Commissioner of Internal Revenuevince005No ratings yet

- ParcOR ReveiwerDocument23 pagesParcOR ReveiwerMon Christian VasquezNo ratings yet

- 2004 Act Blue BookDocument345 pages2004 Act Blue BookparooneyNo ratings yet

- Marketing Strategies of Kotak Life Insurance: BY: MR. Nikhil Kumar Ibs - 2567Document36 pagesMarketing Strategies of Kotak Life Insurance: BY: MR. Nikhil Kumar Ibs - 2567minnigoelNo ratings yet