You might also like

- Special Audit ReportDocument4 pagesSpecial Audit ReportConrad Briones0% (1)

- Summary: Financial Intelligence: Review and Analysis of Berman and Knight's BookFrom EverandSummary: Financial Intelligence: Review and Analysis of Berman and Knight's BookNo ratings yet

- International Precious Metals Legislation The Patriot Act I and Act Ii PDFDocument6 pagesInternational Precious Metals Legislation The Patriot Act I and Act Ii PDFGeron100% (2)

- The Business Owner's Guide to Reading and Understanding Financial Statements: How to Budget, Forecast, and Monitor Cash Flow for Better Decision MakingFrom EverandThe Business Owner's Guide to Reading and Understanding Financial Statements: How to Budget, Forecast, and Monitor Cash Flow for Better Decision MakingRating: 4 out of 5 stars4/5 (4)

- T CodesDocument43 pagesT CodesSuresh KrishnanNo ratings yet

- Agreement On Delivery of Cash Funds For Investments Via Ipip Special Transfer Swift Message Transmission N°Document13 pagesAgreement On Delivery of Cash Funds For Investments Via Ipip Special Transfer Swift Message Transmission N°Miguel Goncalves100% (1)

- PSCAI Lecture 1Document39 pagesPSCAI Lecture 1Ritashree DasguptaNo ratings yet

- Understanding The Basics of Accounting, Finance, and Financial ManagementDocument17 pagesUnderstanding The Basics of Accounting, Finance, and Financial Managementfrickzy ibanezNo ratings yet

- Assignment: Principles of AccountingDocument11 pagesAssignment: Principles of Accountingmudassar saeedNo ratings yet

- ACCT 504 MART Perfect EducationDocument68 pagesACCT 504 MART Perfect EducationdavidwarNo ratings yet

- WWW Diligent Com R...Document8 pagesWWW Diligent Com R...Unanimous ClientNo ratings yet

- TOPIC 7 Financial-Statement-Preparation-and-AnalysisDocument8 pagesTOPIC 7 Financial-Statement-Preparation-and-Analysiskenl69784No ratings yet

- 1 Ch.1 Fundamentals of Financial Accounting: PIDP 3240 Assignment 4 (Textbook Chapter)Document7 pages1 Ch.1 Fundamentals of Financial Accounting: PIDP 3240 Assignment 4 (Textbook Chapter)Jaspal SinghNo ratings yet

- Financial and Managerial Accounting: Seven Key DifferencesDocument39 pagesFinancial and Managerial Accounting: Seven Key DifferencesrNo ratings yet

- Cost AccountingDocument4 pagesCost AccountingAretha Joi Domingo PrezaNo ratings yet

- Leac 205Document47 pagesLeac 205Jyoti SinghNo ratings yet

- Accounting Ratios: Inancial Statements Aim at Providing FDocument53 pagesAccounting Ratios: Inancial Statements Aim at Providing FPathan Kausar100% (1)

- Group 7Document28 pagesGroup 7Luis Nguyen HaNo ratings yet

- Key Performance Indicators: Strategy Directors' BriefingDocument4 pagesKey Performance Indicators: Strategy Directors' BriefingMarcel e Andrea BonfimNo ratings yet

- 1 - Intro To CostDocument7 pages1 - Intro To CostALLYSON BURAGANo ratings yet

- Management Account Sem 1Document28 pagesManagement Account Sem 1Darshan VadherNo ratings yet

- Accounting RatiosDocument42 pagesAccounting RatiosApollo Institute of Hospital AdministrationNo ratings yet

- Dwnload Full Horngrens Cost Accounting A Managerial Emphasis Canadian 8th Edition Datar Solutions Manual PDFDocument18 pagesDwnload Full Horngrens Cost Accounting A Managerial Emphasis Canadian 8th Edition Datar Solutions Manual PDFaffluencevillanzn0qkr100% (8)

- Leac 205Document47 pagesLeac 205Harish Singh NegiNo ratings yet

- ISO 9001 Quality Gap AnalysisDocument48 pagesISO 9001 Quality Gap Analysistracey.gartonNo ratings yet

- ACC 124 - Week 1-3 QuizDocument14 pagesACC 124 - Week 1-3 QuizJaneth BarreteNo ratings yet

- S4. Accounting AnalysisDocument22 pagesS4. Accounting AnalysisJoão Maria VigárioNo ratings yet

- ACC223 - Strategic AnalysisDocument16 pagesACC223 - Strategic Analysiswil markNo ratings yet

- FandI Best Practices and Performance MetricsDocument8 pagesFandI Best Practices and Performance MetricsJawad JadNo ratings yet

- Accounting Notes XIIDocument47 pagesAccounting Notes XIIAdarshNo ratings yet

- SGX Investor's Guide To Reading Annual ReportsDocument12 pagesSGX Investor's Guide To Reading Annual Reportsjilbo604No ratings yet

- 1 - Introduction To AccountingDocument54 pages1 - Introduction To AccountingNazmul Ahshan SawonNo ratings yet

- DocxDocument5 pagesDocxMandil BhandariNo ratings yet

- Cost and MGMT Accti Chapter 1 Introduction and Cost ClassificationDocument17 pagesCost and MGMT Accti Chapter 1 Introduction and Cost ClassificationMahlet AbrahaNo ratings yet

- Chapter 1 and 2Document13 pagesChapter 1 and 2limenihNo ratings yet

- 01 - Lec - Conceptual FrameworkDocument5 pages01 - Lec - Conceptual FrameworkYoung MetroNo ratings yet

- End TermDocument141 pagesEnd TermTangirala AshwiniNo ratings yet

- Chapter 1Document14 pagesChapter 1narrNo ratings yet

- Service Outputs inDocument2 pagesService Outputs inIsfandiyer SmithNo ratings yet

- BA-224-FM-Activity-No-2 - DELA CRUZ, TRISHA T.Document5 pagesBA-224-FM-Activity-No-2 - DELA CRUZ, TRISHA T.Trisha Dela CruzNo ratings yet

- Accounting Ratios: Inancial Statements Aim at Providing FDocument45 pagesAccounting Ratios: Inancial Statements Aim at Providing FNIKK KICKNo ratings yet

- s1 Accounting InformationDocument4 pagess1 Accounting InformationmartinNo ratings yet

- BBAW2103 Topic 1Document30 pagesBBAW2103 Topic 1MOHD SYUKRI BIN ABDUL WAHAB STUDENTNo ratings yet

- Finance ControllersDocument21 pagesFinance Controllersyashkanthaliya5No ratings yet

- Financial Accounting: Theory AnalysisDocument34 pagesFinancial Accounting: Theory AnalysisYESSICA CHANDRANo ratings yet

- CH 05Document34 pagesCH 05YESSICA CHANDRANo ratings yet

- Guide To Reading Annual ReportsDocument12 pagesGuide To Reading Annual ReportsChin Pu MaNo ratings yet

- 12 (12-00) Understand The Accounting System - Sales and Accounts ReceivableDocument3 pages12 (12-00) Understand The Accounting System - Sales and Accounts ReceivableTran AnhNo ratings yet

- Dwnload Full Auditing and Assurance Services 17th Edition Arens Solutions Manual PDFDocument36 pagesDwnload Full Auditing and Assurance Services 17th Edition Arens Solutions Manual PDFmutevssarahm100% (15)

- Chapter 1 - IntroductionDocument19 pagesChapter 1 - IntroductionGiang TrầnNo ratings yet

- Lecture 5Document34 pagesLecture 5Maham AhsanNo ratings yet

- Cost Acc 1 Module Chapter 1Document56 pagesCost Acc 1 Module Chapter 1Khalid MuhammadNo ratings yet

- Internal Auditing at Shan FoodsDocument6 pagesInternal Auditing at Shan FoodsmubeenNo ratings yet

- Retail AuditDocument44 pagesRetail AuditNivethitha Narayanasamy50% (2)

- Basic Accounting Module 1Document6 pagesBasic Accounting Module 1rima riveraNo ratings yet

- HRM HBL PakistanDocument13 pagesHRM HBL PakistanNabeel RazzaqNo ratings yet

- ACCT 321-Managerial Accounting-1Document106 pagesACCT 321-Managerial Accounting-1Fabio NyagemiNo ratings yet

- Amr Abdeen's CV-Financial AccountantDocument2 pagesAmr Abdeen's CV-Financial AccountantBassam AhmedNo ratings yet

- Week 4Document25 pagesWeek 4Jason wibisonoNo ratings yet

- Conceptual and Regulatory FrameworkDocument10 pagesConceptual and Regulatory FrameworkMohamed Yada AlghaliNo ratings yet

- Auditing: Concept of MaterialityDocument43 pagesAuditing: Concept of MaterialityZead MahmoodNo ratings yet

- KPMG Ifrs18Document15 pagesKPMG Ifrs18Rubens SaraivaNo ratings yet

- NCERT Class 12 Accountancy Accounting RatiosDocument47 pagesNCERT Class 12 Accountancy Accounting RatiosKrish Pagani100% (1)

- CH - 5 Accounting RatiosDocument47 pagesCH - 5 Accounting RatiosAaditi V100% (1)

- Financial Department Review ReportDocument34 pagesFinancial Department Review Reportche.serenoNo ratings yet

- 4b - Exhibit A - Internal Audit ActivtyDocument15 pages4b - Exhibit A - Internal Audit ActivtyMaria Rona SilvestreNo ratings yet

- 4A's-Guidelines For Digital Media AuditsDocument30 pages4A's-Guidelines For Digital Media AuditsMaria Rona SilvestreNo ratings yet

- QAIP InternalDocument12 pagesQAIP InternalMaria Rona Silvestre100% (2)

- QAIP ExternalDocument4 pagesQAIP ExternalMaria Rona SilvestreNo ratings yet

- Enterprise Security Key Performance Indicators (KPIs)Document7 pagesEnterprise Security Key Performance Indicators (KPIs)Maria Rona SilvestreNo ratings yet

- Account Reconciliation PolicyDocument12 pagesAccount Reconciliation PolicyMaria Rona SilvestreNo ratings yet

- Service-Level Controls Audit Work ProgramDocument14 pagesService-Level Controls Audit Work ProgramRahila ShahNo ratings yet

- Month End Closing ProceduresDocument8 pagesMonth End Closing ProceduresAniruddha ChakrabortyNo ratings yet

- SOX ProcessDocument6 pagesSOX ProcessMaria Rona SilvestreNo ratings yet

- Google Ocr DataDocument18 pagesGoogle Ocr DataAshis RajNo ratings yet

- Theory & Practice of Auditing Bcom Part-3Document78 pagesTheory & Practice of Auditing Bcom Part-3Srinivasarao SettyNo ratings yet

- Gifts Item SOP: InputsDocument8 pagesGifts Item SOP: InputsAnujkr KumarNo ratings yet

- Venkata RamanaDocument1 pageVenkata RamanaVenkata vadaNo ratings yet

- Bruhat Bengaluru Mahanagara Palike - Revenue Department: Xjdœ LXD - /HZ Eud/ Eĺ Lbx¡E (6 E LDocument1 pageBruhat Bengaluru Mahanagara Palike - Revenue Department: Xjdœ LXD - /HZ Eud/ Eĺ Lbx¡E (6 E LamitthemalNo ratings yet

- 尼日利亚机械零件Document2 pages尼日利亚机械零件lucy61c5No ratings yet

- IntercompanyDocument48 pagesIntercompanyPritesh Mogane0% (2)

- 4 Revenue 10 QuestionsDocument2 pages4 Revenue 10 QuestionsEzer Cruz BarrantesNo ratings yet

- Business CorrespondentDocument22 pagesBusiness CorrespondentdivyangNo ratings yet

- nx5400 02 Operation ManualDocument90 pagesnx5400 02 Operation ManualEnter_69100% (4)

- Commissioner of Internal Revenue vs. Mirant Pagbilao CorporationDocument23 pagesCommissioner of Internal Revenue vs. Mirant Pagbilao CorporationToni LorescaNo ratings yet

- Policy On Accounts ReceivableDocument8 pagesPolicy On Accounts ReceivableMazhar Hussain Ch.No ratings yet

- Ddo ChecklistDocument14 pagesDdo ChecklistJuan David MateusNo ratings yet

- Business Document (Acc)Document21 pagesBusiness Document (Acc)Aaradhana AnnaduraiNo ratings yet

- Camilla Stryker 660Z ServicioDocument104 pagesCamilla Stryker 660Z Serviciobiomedico internationalNo ratings yet

- First Name: Last Name: Mailing Address: City: State: Email Address: Fold HereDocument1 pageFirst Name: Last Name: Mailing Address: City: State: Email Address: Fold HereBrad BrophyNo ratings yet

- Order LettersDocument10 pagesOrder LettersGhita SafitriNo ratings yet

- Latin American Energy and Infrastructure Finance Forum: 5 AnnualDocument4 pagesLatin American Energy and Infrastructure Finance Forum: 5 AnnualShimon AbouzagloNo ratings yet

- The SOP For Disposal of Cargo Lying in The Port Premises Is As UnderDocument5 pagesThe SOP For Disposal of Cargo Lying in The Port Premises Is As Underanjan.debnathNo ratings yet

- Flowchart Plane BookingDocument1 pageFlowchart Plane BookingdeboleenakunarNo ratings yet

- Application For Registration: Republic of The Philippines BIR Form NoDocument6 pagesApplication For Registration: Republic of The Philippines BIR Form Nomarlon anzanoNo ratings yet

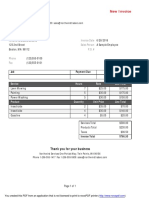

- Northwind Services: Customer Invoice DateDocument1 pageNorthwind Services: Customer Invoice DateJonah ScottNo ratings yet

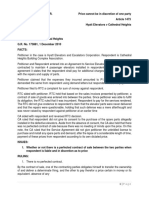

- Hyatt Elevators V Cathedral Heights 11Document2 pagesHyatt Elevators V Cathedral Heights 11Michael MartinNo ratings yet

- 9642 Ireceivables Aahmed PPT 1Document34 pages9642 Ireceivables Aahmed PPT 1Ajaz Ahmed100% (1)

- Sco RusoilDocument3 pagesSco RusoilMusuhan Sama CacingNo ratings yet

- Rayquaza Centralized Billing ApplicationDocument3 pagesRayquaza Centralized Billing ApplicationWARSE JournalsNo ratings yet