You might also like

- Documento InglesDocument9 pagesDocumento InglesDiana Mamani BahozNo ratings yet

- Mexico Foreign Currency and Local Currency Ratings Affirmed Outlook Remains PositiveDocument7 pagesMexico Foreign Currency and Local Currency Ratings Affirmed Outlook Remains Positiveapi-227433089No ratings yet

- Moody's Afirmó La Calificación B2 de Argentina y Bajó Su Perspectiva A NegativaDocument6 pagesMoody's Afirmó La Calificación B2 de Argentina y Bajó Su Perspectiva A NegativaCronista.comNo ratings yet

- Fitch Affirms Uruguay's Rating at 'BBB-' Outlook NegativeDocument6 pagesFitch Affirms Uruguay's Rating at 'BBB-' Outlook NegativeYamid MuñozNo ratings yet

- 2:36 AM GMT+7: Listen To This Article Share This ArticleDocument11 pages2:36 AM GMT+7: Listen To This Article Share This ArticleNguyễn ĐạtNo ratings yet

- Fitch - KOR - Affirmed at AA-, Outlook Stable - 28sep2022Document9 pagesFitch - KOR - Affirmed at AA-, Outlook Stable - 28sep2022jatulanellamaeNo ratings yet

- DBRS Morningstar Changes Trend On Uruguay To Positive, Confirms at BBB (Low)Document11 pagesDBRS Morningstar Changes Trend On Uruguay To Positive, Confirms at BBB (Low)SubrayadoHDNo ratings yet

- Moodys - Affirms - Mexicos - at - Baa1 - Negative - Outlook - 210429Document7 pagesMoodys - Affirms - Mexicos - at - Baa1 - Negative - Outlook - 210429Harvey NoblesNo ratings yet

- Moodys - Argentina - Affirmed at Ca, Outlook Maintained at Stable - 27sep2022Document6 pagesMoodys - Argentina - Affirmed at Ca, Outlook Maintained at Stable - 27sep2022jatulanellamaeNo ratings yet

- Fitch Affirms El Salvador at 'CC'Document11 pagesFitch Affirms El Salvador at 'CC'Carolina ArteagaNo ratings yet

- Enacted Budget Report 2020-21Document22 pagesEnacted Budget Report 2020-21Luke ParsnowNo ratings yet

- Brazil Country OverviewDocument1 pageBrazil Country OverviewjearodriguesNo ratings yet

- Colorado September 2020 Economic and Revenue ForecastDocument81 pagesColorado September 2020 Economic and Revenue Forecastbobjones3296No ratings yet

- Fitch Downgrades IllinoisDocument4 pagesFitch Downgrades IllinoisAnn WeilerNo ratings yet

- Analysis of The Presidents Fiscal Year 2015 BudgetDocument7 pagesAnalysis of The Presidents Fiscal Year 2015 BudgetShirley FarraceNo ratings yet

- Informe MoodysDocument9 pagesInforme MoodysMontevideo PortalNo ratings yet

- 09.07.12 JPM Fiscal Cliff White PaperDocument16 pages09.07.12 JPM Fiscal Cliff White PaperRishi ShahNo ratings yet

- Press Release Fich BrasilDocument7 pagesPress Release Fich BrasilBruno Enrique Silva AndradeNo ratings yet

- Hidden Spending: The Politics of Federal Credit ProgramsFrom EverandHidden Spending: The Politics of Federal Credit ProgramsNo ratings yet

- Fitch Ratings ReportDocument3 pagesFitch Ratings ReportMaineHouseGOP2No ratings yet

- HIM2016Q1Document7 pagesHIM2016Q1Puru SaxenaNo ratings yet

- FitchDocument9 pagesFitchTiso Blackstar Group100% (1)

- New Jersey's GO Rating Lowered To A+' On Continuing Structural Imbalance Outlook StableDocument6 pagesNew Jersey's GO Rating Lowered To A+' On Continuing Structural Imbalance Outlook Stableapi-227433089No ratings yet

- Central Bank of Nigeria Communiqué No. 146 of The Monetary Policy Committee Meeting Held On Monday 23 and Tuesday 24 JANUARY 2023Document70 pagesCentral Bank of Nigeria Communiqué No. 146 of The Monetary Policy Committee Meeting Held On Monday 23 and Tuesday 24 JANUARY 2023QS OH OladosuNo ratings yet

- Fitch - BAN - Affirmed at BB-, Outlook Stable - 29sep2022Document9 pagesFitch - BAN - Affirmed at BB-, Outlook Stable - 29sep2022jatulanellamaeNo ratings yet

- Budget of the U.S. Government: A New Foundation for American Greatness: Fiscal Year 2018From EverandBudget of the U.S. Government: A New Foundation for American Greatness: Fiscal Year 2018No ratings yet

- Fitch Bolivia - 2019-07-02Document12 pagesFitch Bolivia - 2019-07-02Mauricio Jerez QuirogaNo ratings yet

- Rep Paul Ryan On Obamas 2012 Budget and BeyondDocument19 pagesRep Paul Ryan On Obamas 2012 Budget and BeyondKim HedumNo ratings yet

- Holtzeakin Testimony 4oct2011Document12 pagesHoltzeakin Testimony 4oct2011Committee For a Responsible Federal BudgetNo ratings yet

- PR 15 May 20 PDFDocument3 pagesPR 15 May 20 PDFHira RasheedNo ratings yet

- South African Reserve Bank: MPC Statement 21 May 2020Document6 pagesSouth African Reserve Bank: MPC Statement 21 May 2020BusinessTechNo ratings yet

- Is QE Returning by Stealth - Financial TimesDocument4 pagesIs QE Returning by Stealth - Financial TimesLow chee weiNo ratings yet

- HIM2016Q1NPDocument9 pagesHIM2016Q1NPlovehonor0519No ratings yet

- Proyecciones Perú 2022 - 2030Document70 pagesProyecciones Perú 2022 - 2030Javier RiverosNo ratings yet

- UntitledDocument8 pagesUntitledapi-227433089No ratings yet

- Country Analysis Report Canada InDepth PESTLE InsightsDocument103 pagesCountry Analysis Report Canada InDepth PESTLE InsightsAudréanne LangloisNo ratings yet

- Rating - Action Moodys Upgrades Côte Divoire 01mar20 - 240304 - 094127Document9 pagesRating - Action Moodys Upgrades Côte Divoire 01mar20 - 240304 - 094127mamadou.toure.ciNo ratings yet

- The Fed Is TrappedDocument25 pagesThe Fed Is TrappedYog MehtaNo ratings yet

- Sovereigns: U.S. Public Finances - Overview and OutlookDocument15 pagesSovereigns: U.S. Public Finances - Overview and OutlookchanduNo ratings yet

- Aa 2Document2 pagesAa 2Startup AcademyNo ratings yet

- Testimony On The 2013 Long-Term Budget OutlookDocument8 pagesTestimony On The 2013 Long-Term Budget OutlookSteven HansenNo ratings yet

- F F y Y: Ear Uls MmetrDocument4 pagesF F y Y: Ear Uls MmetrChrisBeckerNo ratings yet

- Moody's On ChinaDocument9 pagesMoody's On ChinaTim MooreNo ratings yet

- Financial Stability Report December 2023 Lyst3567Document13 pagesFinancial Stability Report December 2023 Lyst3567tgtk8xgdx9No ratings yet

- Pakistan Economy Face ChallengesDocument2 pagesPakistan Economy Face ChallengesTariq BashirNo ratings yet

- Financial Stability Report June 2023Document10 pagesFinancial Stability Report June 2023asdfNo ratings yet

- A Chapter 2 Assignment Question Sp13Document3 pagesA Chapter 2 Assignment Question Sp13shomy02No ratings yet

- Santander Bahamas 20 SetDocument2 pagesSantander Bahamas 20 SetVitor HenriqueNo ratings yet

- Time Has Come To Rein in Spiralling Public Debt Cape Times The Cape Town South Africa September 18 2023 p1Document2 pagesTime Has Come To Rein in Spiralling Public Debt Cape Times The Cape Town South Africa September 18 2023 p1elihlefass0No ratings yet

- July 2022 CRE ComptrollerDocument32 pagesJuly 2022 CRE ComptrollerThe TexanNo ratings yet

- 2012 Outlook - Us StatesDocument7 pages2012 Outlook - Us Statesm_zhangNo ratings yet

- 2020 10 09 FitchRatings Communication LetterDocument2 pages2020 10 09 FitchRatings Communication LetterErika EsquivelNo ratings yet

- Emerging Markets Economics Daily: Latin AmericaDocument7 pagesEmerging Markets Economics Daily: Latin AmericaBetteDavisEyes00No ratings yet

- CBOmemo Jan 04Document2 pagesCBOmemo Jan 04Committee For a Responsible Federal BudgetNo ratings yet

- Rating Action - Moodys-affirms-Vietnams-Ba3-rating-changes-outlook-to-positive - 18mar21Document7 pagesRating Action - Moodys-affirms-Vietnams-Ba3-rating-changes-outlook-to-positive - 18mar21phatNo ratings yet

- BrazilDocument2 pagesBrazilhana_kimi_91No ratings yet

- Rentekoers - 14 April 2020Document6 pagesRentekoers - 14 April 2020ElviraNo ratings yet

- Rating Action - Moodys-downgrades-Perus-rating-to-Baa1-changes-outlook-to-stable - 01sep21Document6 pagesRating Action - Moodys-downgrades-Perus-rating-to-Baa1-changes-outlook-to-stable - 01sep21jimmygerman333No ratings yet

- 2b) Blockchain Technology & It's Impact On The World - Shri. Narendranath NairDocument32 pages2b) Blockchain Technology & It's Impact On The World - Shri. Narendranath NairL N Murthy KapavarapuNo ratings yet

- Substantive Test of Intangible Assets, Prepaid Expenses (Autosaved)Document38 pagesSubstantive Test of Intangible Assets, Prepaid Expenses (Autosaved)Mej AgaoNo ratings yet

- Po PCitesDocument17 pagesPo PCitesjohn doeNo ratings yet

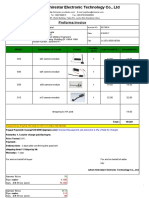

- Shenzhen Shirestar Electronic Technology Co., LTD: Proforma InvoiceDocument3 pagesShenzhen Shirestar Electronic Technology Co., LTD: Proforma InvoicepintoNo ratings yet

- Chapter 5 Marginal CostingDocument36 pagesChapter 5 Marginal CostingSuku Thomas SamuelNo ratings yet

- Padma Multipurpose BridgeDocument10 pagesPadma Multipurpose BridgeMD. Mahamudul HasanNo ratings yet

- Molisteel - PowerPointDocument35 pagesMolisteel - PowerPointPatel Ki BahuNo ratings yet

- Lansing (MI) City Council Meeting Info Packet For June 28 MeetingDocument213 pagesLansing (MI) City Council Meeting Info Packet For June 28 MeetingwesthorpNo ratings yet

- Unit2TimeandMoneyB - Lavarias - Lorenz JayDocument4 pagesUnit2TimeandMoneyB - Lavarias - Lorenz JayCarmelo Janiza LavareyNo ratings yet

- Wood Group ESP CatalogueDocument359 pagesWood Group ESP Cataloguehermit44535100% (11)

- Simulation 9 - Bookkeeping TemplateDocument3 pagesSimulation 9 - Bookkeeping Templateapi-520325493No ratings yet

- Resume TKTI Modul 1 Cobit 2019 - Framework MethodologyDocument23 pagesResume TKTI Modul 1 Cobit 2019 - Framework MethodologyShiryu XavierNo ratings yet

- SwitchDocument2 pagesSwitchvasuNo ratings yet

- MTN FinancialsDocument200 pagesMTN FinancialsIshaan SharmaNo ratings yet

- Caribbean 2021 E&p Summit Program Book - 13september2021Document10 pagesCaribbean 2021 E&p Summit Program Book - 13september2021Renato LongoNo ratings yet

- FACTS: Francisco de Guzman Was Hired by San MiguelDocument1 pageFACTS: Francisco de Guzman Was Hired by San MiguelGabriel LiteralNo ratings yet

- Flinn (ISA 315 + ISA 240 + ISA 570)Document2 pagesFlinn (ISA 315 + ISA 240 + ISA 570)Zareen AbbasNo ratings yet

- Oberoi HotelsDocument4 pagesOberoi HotelsRaju PatelNo ratings yet

- LeanIX - Poster - Best Practices To Define Business Capability Maps - DE - OcredDocument1 pageLeanIX - Poster - Best Practices To Define Business Capability Maps - DE - OcredAlbert MutelNo ratings yet

- Account Statement From 1 Jul 2021 To 15 Jul 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument5 pagesAccount Statement From 1 Jul 2021 To 15 Jul 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceVicky GunaNo ratings yet

- Constitutional Law Primer Bernas-1-258-276Document19 pagesConstitutional Law Primer Bernas-1-258-276Shaira Jean SollanoNo ratings yet

- Research Proposal PowerpointDocument9 pagesResearch Proposal PowerpointMusasa TinasheNo ratings yet

- IMS 01 ManualDocument70 pagesIMS 01 Manualsahiy100% (2)

- Presentation GroupeDocument12 pagesPresentation GroupeJawad BasraNo ratings yet

- Terms Loans, Primary& Collateral Security, Cash Credit FacilityDocument17 pagesTerms Loans, Primary& Collateral Security, Cash Credit FacilityJessica Marilyn VazNo ratings yet

- Chapter 1 5 Income Tax MCDocument14 pagesChapter 1 5 Income Tax MCNoella Marie BaronNo ratings yet

- ATP catalogoOR Ita Def WEBDocument15 pagesATP catalogoOR Ita Def WEBSebastian QuespeNo ratings yet

- Hazard Analysis Critical Control Point (HACCP)Document3 pagesHazard Analysis Critical Control Point (HACCP)Waqar IbrahimNo ratings yet

- Bastida vs. Menzi & Co., 58 Phil. 188, March 31, 1933Document29 pagesBastida vs. Menzi & Co., 58 Phil. 188, March 31, 1933VoxDeiVoxNo ratings yet

- Risk Assessment - Cutting and Chipping of Concrete StructureDocument7 pagesRisk Assessment - Cutting and Chipping of Concrete StructureHasham KhanNo ratings yet