You might also like

- Chapter 20 CompilationDocument41 pagesChapter 20 CompilationMaria Licuanan0% (1)

- Ia Activity 4Document23 pagesIa Activity 4WeStan LegendsNo ratings yet

- IA Chapter 15Document12 pagesIA Chapter 15Blue Sky100% (1)

- Chapter 15 ProblemsDocument7 pagesChapter 15 Problemsmercyvienho50% (2)

- Soledad Company Required1 Date Interest Received Interest Income Discount Amortization Carrying AmountDocument2 pagesSoledad Company Required1 Date Interest Received Interest Income Discount Amortization Carrying AmountAnonnNo ratings yet

- Chapter16 BuenaventuraDocument11 pagesChapter16 BuenaventuraAnonn100% (1)

- Royalty Company Required1 Required5 2020 Required2Document2 pagesRoyalty Company Required1 Required5 2020 Required2AnonnNo ratings yet

- Problem 9-1, 2 & 3Document3 pagesProblem 9-1, 2 & 3Micah April SabularseNo ratings yet

- Financial Asset at Fair ValueDocument4 pagesFinancial Asset at Fair ValueDianna DayawonNo ratings yet

- Chapter 18 CompilationDocument21 pagesChapter 18 CompilationMaria Licuanan0% (1)

- Memo - Received 500 Ordinary Shares From Investee As 10% Share Dividend On 5000 Original Shares. Shares Now Held, 5500 SharesDocument3 pagesMemo - Received 500 Ordinary Shares From Investee As 10% Share Dividend On 5000 Original Shares. Shares Now Held, 5500 SharesRey Joyce AbuelNo ratings yet

- Answer Key Assignment in Equity Investments - VALIX 2017Document3 pagesAnswer Key Assignment in Equity Investments - VALIX 2017Shinny Jewel VingnoNo ratings yet

- Ia Chapter 11-12Document4 pagesIa Chapter 11-12Marinella LosaNo ratings yet

- Intermediate Accounting Volume 1: Accounting for Investments in Equity SecuritiesDocument69 pagesIntermediate Accounting Volume 1: Accounting for Investments in Equity SecuritiesRomuell BanaresNo ratings yet

- IA Activity 3 Chapter 6Document2 pagesIA Activity 3 Chapter 6Sunghoon SsiNo ratings yet

- Problem 12-2 To 6Document3 pagesProblem 12-2 To 6MYCO PONCE PAQUENo ratings yet

- Bleak Company Requirement A Debit Credit Requirement BDocument2 pagesBleak Company Requirement A Debit Credit Requirement BAnonn100% (1)

- Diamond CompanyDocument1 pageDiamond CompanyKillua ZOLDYNo ratings yet

- Neophyte Company Required: Debit CreditDocument2 pagesNeophyte Company Required: Debit CreditAnonn100% (1)

- Problem 3 2 RRHDocument10 pagesProblem 3 2 RRHCarl Jaime Dela CruzNo ratings yet

- Machete Company Requirement: Prepare Journal Entries Debit CreditDocument1 pageMachete Company Requirement: Prepare Journal Entries Debit CreditAnonnNo ratings yet

- Problem 22-1, Page 610 Classic Company: GivenDocument3 pagesProblem 22-1, Page 610 Classic Company: GivenDeanne LumakangNo ratings yet

- Bond Interest Income and Discount AmortizationDocument3 pagesBond Interest Income and Discount AmortizationMaria LicuananNo ratings yet

- Activity in E3 - LiabilitiesDocument9 pagesActivity in E3 - LiabilitiesPaupau100% (1)

- Activity 5 - Chapter 22 Investment Property (Cash Surrender Value) Problem 22-2 (IFRS)Document6 pagesActivity 5 - Chapter 22 Investment Property (Cash Surrender Value) Problem 22-2 (IFRS)WeStan LegendsNo ratings yet

- IA Problem 17 4Document8 pagesIA Problem 17 4nenzzmariaNo ratings yet

- GROUP2 AE105 Chp.11 14Document26 pagesGROUP2 AE105 Chp.11 14Isabelle CandelariaNo ratings yet

- Problem 1-3 and Problem 1-4 CarinoDocument2 pagesProblem 1-3 and Problem 1-4 Carinoschool worksNo ratings yet

- BAICC2X-Solution Supplementary - Week 1docxDocument7 pagesBAICC2X-Solution Supplementary - Week 1docxMitchie FaustinoNo ratings yet

- Problem 4 2Document10 pagesProblem 4 2Carl Jaime Dela CruzNo ratings yet

- Razor Company Required Debit Credit 2020Document14 pagesRazor Company Required Debit Credit 2020AnonnNo ratings yet

- Chapter 18Document34 pagesChapter 18Christine Marie T. RamirezNo ratings yet

- ACC123 InventoryCostFlowDocument3 pagesACC123 InventoryCostFlowkhryzellia lagurinNo ratings yet

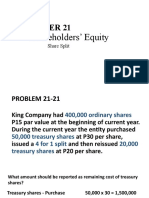

- Prob 21 21Document4 pagesProb 21 21Rhea Jane ParconNo ratings yet

- Loans ReceivableDocument22 pagesLoans ReceivableJendall SisonNo ratings yet

- Account for Liabilities and EquityDocument34 pagesAccount for Liabilities and EquityMitchie Faustino100% (1)

- Walleye Company Requirement: Prepare Journal Entries Debit CreditDocument1 pageWalleye Company Requirement: Prepare Journal Entries Debit CreditAnonnNo ratings yet

- Capital Expenditures on Machinery ProblemsDocument3 pagesCapital Expenditures on Machinery ProblemsZes ONo ratings yet

- Problem 6-5 & 6Document2 pagesProblem 6-5 & 6Micah April SabularseNo ratings yet

- 6-4 Gullible Company Req 1Document2 pages6-4 Gullible Company Req 1mercyvienhoNo ratings yet

- Chapter 19 20Document11 pagesChapter 19 20Kyle Francine BoloNo ratings yet

- Calculate Market Price and Amortization of Bonds Issued at a DiscountDocument5 pagesCalculate Market Price and Amortization of Bonds Issued at a DiscountKris Hazel RentonNo ratings yet

- Vain Company Requirement: Prepare Journal Entries On The Books of Assignor Debit CreditDocument1 pageVain Company Requirement: Prepare Journal Entries On The Books of Assignor Debit CreditAnonnNo ratings yet

- ACCOUNTING 2 - ProblemsDocument6 pagesACCOUNTING 2 - ProblemsJasmin NoblezaNo ratings yet

- Problem 13 - 1 To Problem 13 - 8Document4 pagesProblem 13 - 1 To Problem 13 - 8Jem ColebraNo ratings yet

- Exercise ProblemsDocument6 pagesExercise ProblemsDianna Rose Vico100% (1)

- Zeta Company Required1 Required5 2020 Required2Document2 pagesZeta Company Required1 Required5 2020 Required2AnonnNo ratings yet

- Padernal BSA 1A SW Problem 3 11Document1 pagePadernal BSA 1A SW Problem 3 11Fly ThoughtsNo ratings yet

- CHEER UP Chapter 13 Gross Profit MethodDocument7 pagesCHEER UP Chapter 13 Gross Profit MethodaprilNo ratings yet

- Problem 21-1Document7 pagesProblem 21-1camilleescote562No ratings yet

- Computation:: Freeway Company Requirement1: Books of Motorway Company Debit CreditDocument2 pagesComputation:: Freeway Company Requirement1: Books of Motorway Company Debit CreditAnonn100% (1)

- Pittance Company Requirement: Prepare Journal Entries To Record The Transactions Debit CreditDocument1 pagePittance Company Requirement: Prepare Journal Entries To Record The Transactions Debit CreditAnonnNo ratings yet

- Chapter22 BuenaventuraDocument4 pagesChapter22 BuenaventuraAnonnNo ratings yet

- Final Exam (Page 1 of 10)Document10 pagesFinal Exam (Page 1 of 10)kaeya alberichNo ratings yet

- Cash and Cash Equivalents of Swiss CompanyDocument16 pagesCash and Cash Equivalents of Swiss CompanyLyca Mae CubangbangNo ratings yet

- Chapter 14 AnswersevenDocument4 pagesChapter 14 AnswersevenJulianne Mejia100% (1)

- Basic Finance Major OutputDocument3 pagesBasic Finance Major OutputKazia PerinoNo ratings yet

- Chapter 20 - Effective Interest Method (Amortized Cost, FVOCI, FVPL)Document66 pagesChapter 20 - Effective Interest Method (Amortized Cost, FVOCI, FVPL)Never Letting GoNo ratings yet

- Ia PPT 6Document20 pagesIa PPT 6lorriejaneNo ratings yet

- Chapter 20 - Effective Interest Method PDFDocument18 pagesChapter 20 - Effective Interest Method PDFTurksNo ratings yet

- Liam Mescall CDS Trading 1Document7 pagesLiam Mescall CDS Trading 1Liam MescallNo ratings yet

- Multiple Choice Questions: Share CapitaalDocument21 pagesMultiple Choice Questions: Share CapitaalYashik JindalNo ratings yet

- PAS 36 Test BankDocument8 pagesPAS 36 Test BankJake ScotNo ratings yet

- LCCA: Life-Cycle Cost AnalysisDocument2 pagesLCCA: Life-Cycle Cost AnalysisglennpanNo ratings yet

- 1000 Questions PDFDocument149 pages1000 Questions PDFManju Rana100% (1)

- WEEK 1 - TVM and GrowthDocument32 pagesWEEK 1 - TVM and GrowthowenNo ratings yet

- Basic Economic Study MethodsDocument53 pagesBasic Economic Study MethodsDrix ReyesNo ratings yet

- Adjust Accounts Receivable, Allowances and Notes ReceivableDocument6 pagesAdjust Accounts Receivable, Allowances and Notes ReceivablekrizzmaaaayNo ratings yet

- Week 2 Theory of Accounts Part 2 QuizDocument6 pagesWeek 2 Theory of Accounts Part 2 QuizMarilou Arcillas PanisalesNo ratings yet

- SDA Modeling Recommendations 2016Document264 pagesSDA Modeling Recommendations 2016MarcoNo ratings yet

- ACC 30 Research PaperDocument29 pagesACC 30 Research PaperPat RiveraNo ratings yet

- Adventity Valuation DCF AnalysisDocument22 pagesAdventity Valuation DCF AnalysisKnowledge GuruNo ratings yet

- ICAEW Financial Accounting Answers March 2015 To March 2016 (SPirate)Document82 pagesICAEW Financial Accounting Answers March 2015 To March 2016 (SPirate)Ahmed Raza Mir100% (1)

- Emaar Properties Q4 2021 Investor PresentationDocument75 pagesEmaar Properties Q4 2021 Investor PresentationprONo ratings yet

- PMP Exam Prep: (What It Really Takes To Prepare and Pass)Document26 pagesPMP Exam Prep: (What It Really Takes To Prepare and Pass)PrabirNo ratings yet

- Long-Term Liabilities: Intermediate Accounting 12th Edition Kieso, Weygandt, and WarfieldDocument41 pagesLong-Term Liabilities: Intermediate Accounting 12th Edition Kieso, Weygandt, and WarfieldYunus Alfani100% (1)

- Fin 202 S1 2016Document29 pagesFin 202 S1 2016herueuxNo ratings yet

- Unit 4Document25 pagesUnit 4Vinita ThoratNo ratings yet

- Tutorial 2 Problem Set Answers - FinalDocument37 pagesTutorial 2 Problem Set Answers - FinalHelloNo ratings yet

- INVESTMENTS W Matrix PFRS 9 PDFDocument7 pagesINVESTMENTS W Matrix PFRS 9 PDFAra DucusinNo ratings yet

- ACCA P4 Investment International.Document19 pagesACCA P4 Investment International.saeed_r2000422100% (1)

- DCF Model of Bharti Airtel: AssumptionsDocument4 pagesDCF Model of Bharti Airtel: AssumptionsHARSHIL RATHINo ratings yet

- The Gold Standard Journal 12Document13 pagesThe Gold Standard Journal 12ulfheidner9103No ratings yet

- BOE - JumpstartDocument4 pagesBOE - JumpstartMeester Kewpie0% (1)

- Accounting for Property, Plant and Equipment (PPEDocument64 pagesAccounting for Property, Plant and Equipment (PPENicol Jay DuriguezNo ratings yet

- TUI AG Bericht 2019 ENDocument48 pagesTUI AG Bericht 2019 ENgoggsNo ratings yet

- AC825 - 46C - Money Market - Foreign Exchage and DerivativesDocument379 pagesAC825 - 46C - Money Market - Foreign Exchage and DerivativesUmarah Furqan100% (1)

- Compliance Officers Certification Course Registration FormDocument1 pageCompliance Officers Certification Course Registration Formsheshe gamiaoNo ratings yet

- Group Assigment IAPMDocument6 pagesGroup Assigment IAPMasdNo ratings yet

- Introduction to Economics and Math of Financial MarketsDocument517 pagesIntroduction to Economics and Math of Financial MarketsMaria Estrella Che Bruja100% (1)