You might also like

- ABBYDocument11 pagesABBYSahilNo ratings yet

- Smart Money Concept and Prospects For Further Research From A Perspective of The Polish Startup Ecosystem DevelopmentDocument12 pagesSmart Money Concept and Prospects For Further Research From A Perspective of The Polish Startup Ecosystem DevelopmentPhát MinhNo ratings yet

- InternationalDocument9 pagesInternationalrituudubey09No ratings yet

- 4522 ArticleText 12351 1 10 20210502Document21 pages4522 ArticleText 12351 1 10 20210502dsrawlotNo ratings yet

- Assessing The Dynamics of Fintech in Indonesia"Document9 pagesAssessing The Dynamics of Fintech in Indonesia"Khurram AbidNo ratings yet

- Business Models for Startups Based on TechnologyDocument8 pagesBusiness Models for Startups Based on TechnologyMuhammad Rafif FarhanNo ratings yet

- Understanding Fintech Ecosystem Evolution Through Service Innovation and Socio-Technical System PerspectiveDocument15 pagesUnderstanding Fintech Ecosystem Evolution Through Service Innovation and Socio-Technical System PerspectiveJery Rivadeneira SantamariaNo ratings yet

- Fintech 1Document24 pagesFintech 1Mohamed LaarabiNo ratings yet

- What Have We Learnt From 10 Years of Fintech Research A ScientometricDocument12 pagesWhat Have We Learnt From 10 Years of Fintech Research A ScientometricFatima zahra OtmaniNo ratings yet

- Economics Project Report FinalDocument11 pagesEconomics Project Report Finaldivyanshu.221ch018No ratings yet

- Digital EntrepreneurshipDocument25 pagesDigital EntrepreneurshipSudeesha Wenura BandaraNo ratings yet

- Application of Entrepreneurship in Small BusinessesDocument6 pagesApplication of Entrepreneurship in Small BusinessesIJAERS JOURNALNo ratings yet

- Social Media EntrepreneushipDocument71 pagesSocial Media Entrepreneushipdaniel100% (1)

- Thailand’s Evolving Ecosystem Support for Technology StartupsFrom EverandThailand’s Evolving Ecosystem Support for Technology StartupsNo ratings yet

- Future of FintechDocument6 pagesFuture of FintechNguyễn Hoàng ViệtNo ratings yet

- Study of TheStart-Up Ecosystem in Lima Peru-Analysis of Interorganizational NetworksDocument13 pagesStudy of TheStart-Up Ecosystem in Lima Peru-Analysis of Interorganizational Networkschcenzano100% (1)

- Literature ReviewDocument30 pagesLiterature Reviewda__nnaNo ratings yet

- Assignment 1 Course Name: Entrepreneurship For Engineers CHE-405Document10 pagesAssignment 1 Course Name: Entrepreneurship For Engineers CHE-405MALIK ZARYABBABARNo ratings yet

- The First Annual Toronto Fintech Conference: Call For PapersDocument5 pagesThe First Annual Toronto Fintech Conference: Call For PapersramNo ratings yet

- Taming The Beast: A Scientific Definition of FintechDocument24 pagesTaming The Beast: A Scientific Definition of FintecheviananhicolashNo ratings yet

- A Study On Emerging Trends in Indian Startup Ecosystem - Big Data, Crowd Funding, Shared EconomyDocument16 pagesA Study On Emerging Trends in Indian Startup Ecosystem - Big Data, Crowd Funding, Shared EconomyLuis NedvedNo ratings yet

- Paper Fintech Open Journalof Economicsand Commerce 2019Document14 pagesPaper Fintech Open Journalof Economicsand Commerce 2019dsrawlotNo ratings yet

- Hybridity ConsultingDocument22 pagesHybridity Consultingpoliran.sheilamaeNo ratings yet

- Entrepreneurship Module 1Document10 pagesEntrepreneurship Module 1Renjith RNo ratings yet

- Entrepreneurship & Innovation in Tech StartupsDocument5 pagesEntrepreneurship & Innovation in Tech StartupsTuti Thuy MaiNo ratings yet

- Entrepre Nuer ShipDocument6 pagesEntrepre Nuer ShipNag28rajNo ratings yet

- 591_Research_PaperDocument5 pages591_Research_PaperLexene CamposNo ratings yet

- Start Ups LandscapeDocument63 pagesStart Ups LandscapePARAS JAINNo ratings yet

- 9 - Fintech & Milenial GenrtDocument12 pages9 - Fintech & Milenial GenrtDiah Tiffani AnnisaNo ratings yet

- An Analytical Study On Problems and Challenges Faced by Startup India Initiative and Its Role On Economic Development of IndiaDocument6 pagesAn Analytical Study On Problems and Challenges Faced by Startup India Initiative and Its Role On Economic Development of IndiaSuyash JainNo ratings yet

- Will Design Thinking Save UsDocument7 pagesWill Design Thinking Save UsClaire NouvelNo ratings yet

- SSRN-id3823361Document9 pagesSSRN-id3823361inconnueNo ratings yet

- The Future of FintechDocument6 pagesThe Future of FintechMukul SharmaNo ratings yet

- Literature ReviewDocument2 pagesLiterature ReviewMukul SharmaNo ratings yet

- Finding the Innovation Gap: Disruptive Idea, a Better Way of Managing Prototypes: Disruptive Idea, a Better Way of Managing PrototypesFrom EverandFinding the Innovation Gap: Disruptive Idea, a Better Way of Managing Prototypes: Disruptive Idea, a Better Way of Managing PrototypesNo ratings yet

- Why Do Software Startups FailDocument12 pagesWhy Do Software Startups FailKunal KhetarpalNo ratings yet

- Future Challenges To The Entrepreneur in Relation To The Changing Business EnvironmentDocument10 pagesFuture Challenges To The Entrepreneur in Relation To The Changing Business EnvironmentShan rNo ratings yet

- The Effect of E-Marketing With Aisas Model AttentiDocument12 pagesThe Effect of E-Marketing With Aisas Model AttentiSơn NguyễnNo ratings yet

- Sustainability-13-02242-V2 - Cópia - Cópia - Cópia - CópiaDocument14 pagesSustainability-13-02242-V2 - Cópia - Cópia - Cópia - CópiaGuiguitoNo ratings yet

- Schueffel 2016 Tamingthe Beast AScientific Definitionof Fintech JIMDocument24 pagesSchueffel 2016 Tamingthe Beast AScientific Definitionof Fintech JIMbaohoanguyen1027No ratings yet

- Fintech Unit 1Document70 pagesFintech Unit 1Sushrut ChauhanNo ratings yet

- IntroductionDocument2 pagesIntroductionAsif Bin ZamanNo ratings yet

- Fintech Business Models Applied Canvas Method and Analysis of Venture Capital Rounds (Matthias Fischer) (Z-Library)Document312 pagesFintech Business Models Applied Canvas Method and Analysis of Venture Capital Rounds (Matthias Fischer) (Z-Library)Minh Khánh NguyenNo ratings yet

- P.C.C.O.E F.Y.M.B.A 2018-19Document20 pagesP.C.C.O.E F.Y.M.B.A 2018-19karanNo ratings yet

- The Philosophy of Digital Entrepreneurship: What it Takes to Become Part of Digital EntrepreneurshipFrom EverandThe Philosophy of Digital Entrepreneurship: What it Takes to Become Part of Digital EntrepreneurshipNo ratings yet

- Financial Technology Fintech Dalam Perspektif Aksi PDFDocument16 pagesFinancial Technology Fintech Dalam Perspektif Aksi PDFihsanul ikhwanNo ratings yet

- FinTech and Shadow Banks Loan ComparisonDocument10 pagesFinTech and Shadow Banks Loan ComparisonHilmansyah AminNo ratings yet

- Potential Businesses in Batangas CityDocument24 pagesPotential Businesses in Batangas CityMichael DimayugaNo ratings yet

- Ijtm 2021 115761Document22 pagesIjtm 2021 115761Muluken AlemuNo ratings yet

- Metamorphosis of Intrapreneurship As An Effective Organizational StrategyDocument12 pagesMetamorphosis of Intrapreneurship As An Effective Organizational StrategyNgo Ngoc Quynh NhuNo ratings yet

- Entrepreneurial Mindset of Information and Communication Technology FirmsDocument21 pagesEntrepreneurial Mindset of Information and Communication Technology FirmsSiti Zalina Mat HussinNo ratings yet

- International Journal of EngineeringDocument15 pagesInternational Journal of EngineeringRanjita ChakrabortyNo ratings yet

- Research ProposalDocument14 pagesResearch ProposalFerdyana LieNo ratings yet

- 4-A Framework For Business Model With Strategic Innovation in ICT FirmsDocument26 pages4-A Framework For Business Model With Strategic Innovation in ICT FirmsKlly CadavidNo ratings yet

- StartupsDocument8 pagesStartupscanadian diazNo ratings yet

- Fin Tech Business ModelsDocument21 pagesFin Tech Business ModelspufuNo ratings yet

- CIL Sustainability Report-2020-21Document100 pagesCIL Sustainability Report-2020-21IndraniGhoshNo ratings yet

- Paper Fintech Open Journalof Economicsand Commerce 2019Document14 pagesPaper Fintech Open Journalof Economicsand Commerce 2019dsrawlotNo ratings yet

- 1 Automobile Intro v5 1Document66 pages1 Automobile Intro v5 1igoysinghNo ratings yet

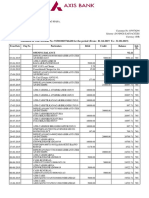

- Statement of Axis Account No:915010025746420 For The Period (From: 01-04-2019 To: 31-08-2019)Document3 pagesStatement of Axis Account No:915010025746420 For The Period (From: 01-04-2019 To: 31-08-2019)dsrawlotNo ratings yet

- All National Safety ConferencesDocument89 pagesAll National Safety ConferencesdsrawlotNo ratings yet

- ITC Limited: CIN WB PLC: L16005 1910 001985Document8 pagesITC Limited: CIN WB PLC: L16005 1910 001985dsrawlotNo ratings yet

- Office ComparisonDocument4 pagesOffice ComparisondsrawlotNo ratings yet

- 3.prevention of Firedamp ExplosionsDocument4 pages3.prevention of Firedamp ExplosionsdsrawlotNo ratings yet

- 1 Automobile Intro v5 1Document66 pages1 Automobile Intro v5 1igoysinghNo ratings yet

- Sewage 004Document19 pagesSewage 004dsrawlotNo ratings yet

- 3.prevention of Firedamp ExplosionsDocument4 pages3.prevention of Firedamp ExplosionsdsrawlotNo ratings yet

- 42.2.1 Objectives of Accident StudiesDocument28 pages42.2.1 Objectives of Accident StudiesAsghar Hussain ShahNo ratings yet

- SR 1Document3 pagesSR 1dsrawlotNo ratings yet

- Excel Kpi Target 90269275Document5 pagesExcel Kpi Target 90269275dsrawlotNo ratings yet

- 42.2.1 Objectives of Accident StudiesDocument28 pages42.2.1 Objectives of Accident StudiesAsghar Hussain ShahNo ratings yet

- Excel Kpi Target 90269275Document5 pagesExcel Kpi Target 90269275dsrawlotNo ratings yet

- Indg 453Document5 pagesIndg 453AsimNo ratings yet

- 1.introduction About Mine ExplosionsDocument4 pages1.introduction About Mine ExplosionsdsrawlotNo ratings yet

- Excel Kpi Target 90269275Document5 pagesExcel Kpi Target 90269275dsrawlotNo ratings yet

- RARBGDocument1 pageRARBGdsrawlotNo ratings yet

- The Coal Mines Regulations, 1957Document140 pagesThe Coal Mines Regulations, 1957mrbads67% (3)

- De Thi Giua Hoc Ki 1 Mon Anh 9 de 1Document4 pagesDe Thi Giua Hoc Ki 1 Mon Anh 9 de 1Nade LemonNo ratings yet

- 2017 Normal EnglishDocument854 pages2017 Normal EnglishÂnuda M ĞalappaththiNo ratings yet

- WEEK 11 Reading MaterialsDocument5 pagesWEEK 11 Reading MaterialsVineetha Victor GonsalvezNo ratings yet

- 16.11.22 - EDT - Prof. Ziad Al-Ani - NotesDocument3 pages16.11.22 - EDT - Prof. Ziad Al-Ani - NotesAarya Haridasan NairNo ratings yet

- Condenser TemperatureDocument10 pagesCondenser TemperatureBerkay AslanNo ratings yet

- Chapter 1:: Grammatical Description of English, Basic TermsDocument6 pagesChapter 1:: Grammatical Description of English, Basic Termsleksandra1No ratings yet

- Crabtree-Industrial Circuit ProtectionDocument104 pagesCrabtree-Industrial Circuit ProtectionAbhyuday Ghosh0% (1)

- Horno Industrial HC1 v1.1Document30 pagesHorno Industrial HC1 v1.1Cristian urielNo ratings yet

- United States v. Jose Antonio Mercado, 307 F.3d 1226, 10th Cir. (2002)Document7 pagesUnited States v. Jose Antonio Mercado, 307 F.3d 1226, 10th Cir. (2002)Scribd Government DocsNo ratings yet

- Well Construction Journal - May/June 2014Document28 pagesWell Construction Journal - May/June 2014Venture PublishingNo ratings yet

- Revised Revenue Code of Puerto Galera 2010Document157 pagesRevised Revenue Code of Puerto Galera 2010Jesselle MamintaNo ratings yet

- Liturgical Music For LentDocument11 pagesLiturgical Music For LentShirly Benedictos100% (1)

- Rfc3435 Dial Plan Digit MapsDocument211 pagesRfc3435 Dial Plan Digit MapsSrinivas VenumuddalaNo ratings yet

- PE Week QuizDocument2 pagesPE Week QuizMarvin RetutalNo ratings yet

- Athangudi TilesDocument84 pagesAthangudi TilesSMITH DESIGN STUDIONo ratings yet

- SAP ABAP Training: String Manipulation and Simple Classical ReportDocument33 pagesSAP ABAP Training: String Manipulation and Simple Classical ReportpraveengkumarerNo ratings yet

- Acacia School Development Plan Proposal v4Document40 pagesAcacia School Development Plan Proposal v4Tim EburneNo ratings yet

- Substation - NoaraiDocument575 pagesSubstation - NoaraiShahriar AhmedNo ratings yet

- PTQM 3 Merged-CombinedDocument562 pagesPTQM 3 Merged-Combined6804 Anushka GhoshNo ratings yet

- Mmk265 Marketing Research Major Project (3) 1.doc 22891Document26 pagesMmk265 Marketing Research Major Project (3) 1.doc 22891dnlkabaNo ratings yet

- About The Rosary of Our LadyDocument2 pagesAbout The Rosary of Our LadyINONG235No ratings yet

- 100 Phrasal Verbs PDFDocument4 pages100 Phrasal Verbs PDFMaia KiladzeNo ratings yet

- Ravi KantDocument1 pageRavi KanthimeltoujoursperitusNo ratings yet

- Worksheet 2-8Document14 pagesWorksheet 2-8Ria LopezNo ratings yet

- Activity 9 - Invitations Valentina Muñoz AriasDocument2 pagesActivity 9 - Invitations Valentina Muñoz AriasValentina Muñoz0% (1)

- Essay Assessment CriteriaDocument1 pageEssay Assessment CriteriaNguyen Quynh AnhNo ratings yet

- Ticket 3586662689Document2 pagesTicket 3586662689dev dNo ratings yet

- TB Chapter08Document79 pagesTB Chapter08CGNo ratings yet

- Appendix D - Correction SymbolsDocument2 pagesAppendix D - Correction SymbolsnhanhoangNo ratings yet

- Prabuddha Bharata June10Document58 pagesPrabuddha Bharata June10talk2ankitNo ratings yet