You might also like

- Aviation Biofuels Develp Conference Oct 2012, Zia Haq, Advanced Biofuels Cost of ProductionDocument10 pagesAviation Biofuels Develp Conference Oct 2012, Zia Haq, Advanced Biofuels Cost of ProductionJuanFleitesNo ratings yet

- Excel QuestinnaireDocument51 pagesExcel QuestinnaireprernaNo ratings yet

- Commitment Control Reports-PeoplesoftDocument46 pagesCommitment Control Reports-Peoplesoftscribd_renjithNo ratings yet

- Advanced Corporate Reporting: Professional 2 ExaminationDocument18 pagesAdvanced Corporate Reporting: Professional 2 ExaminationmohedNo ratings yet

- Weekly Trends July 23Document12 pagesWeekly Trends July 23derailedcapitalism.comNo ratings yet

- Thunderbird Pilipinas Hotels V CIR (CTA 8612, Feb 3 2017)Document64 pagesThunderbird Pilipinas Hotels V CIR (CTA 8612, Feb 3 2017)Firenze PHNo ratings yet

- Deutsche Bank Dr. Josef AckermannDocument32 pagesDeutsche Bank Dr. Josef AckermannLuis Rguez. Del BarrioNo ratings yet

- Trade Portifolio ManagementDocument610 pagesTrade Portifolio ManagementCardoso PenhaNo ratings yet

- SPC EjemplosDocument59 pagesSPC EjemplosDaniel LópezNo ratings yet

- Product Specifications of HOTS Bill Validator: Hitachi Cash Module (HCM)Document11 pagesProduct Specifications of HOTS Bill Validator: Hitachi Cash Module (HCM)immortalNo ratings yet

- Interest Tutor BlankDocument3 pagesInterest Tutor Blankstephanie_krumreiNo ratings yet

- The Real EconomyDocument18 pagesThe Real Economygkmishra2001 at gmail.comNo ratings yet

- 7110 s08 Ms 2Document8 pages7110 s08 Ms 2meelas123No ratings yet

- 13 47 749294 BPStatisticalReviewofWorldEnergy-Brussels September2008 PDFDocument37 pages13 47 749294 BPStatisticalReviewofWorldEnergy-Brussels September2008 PDFyoesseoyNo ratings yet

- Q3 FY08 Earnings ReportDocument14 pagesQ3 FY08 Earnings ReportЂорђе МалешевићNo ratings yet

- Balance of PaymentDocument38 pagesBalance of Paymentalia35002No ratings yet

- Schroder GAIA Egerton Equity: Quarterly Fund UpdateDocument7 pagesSchroder GAIA Egerton Equity: Quarterly Fund UpdatejackefellerNo ratings yet

- September 2018 ECB Staff Macroeconomic Projections For The Euro AreaDocument11 pagesSeptember 2018 ECB Staff Macroeconomic Projections For The Euro AreaIK CleeseNo ratings yet

- Remuneration 2008 VaDocument1 pageRemuneration 2008 VafatmaNo ratings yet

- BNSMT - December 4 - 2009Document12 pagesBNSMT - December 4 - 2009Miir ViirNo ratings yet

- DOST Form 4 - Financial ReportDocument1 pageDOST Form 4 - Financial ReportSelyun E OnnajNo ratings yet

- CP Sev Q1-2012 Va DefDocument5 pagesCP Sev Q1-2012 Va DefGelmu sherpaNo ratings yet

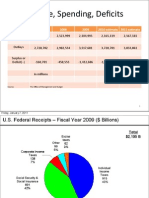

- Income, Spending, DeficitsDocument3 pagesIncome, Spending, DeficitsBill Gram-ReeferNo ratings yet

- Economic Highlights - Fuel and Sugar Prices Were Raised To Reduce - 16/7/2010Document3 pagesEconomic Highlights - Fuel and Sugar Prices Were Raised To Reduce - 16/7/2010Rhb InvestNo ratings yet

- Economic and Monetary Developments: Forecasts by Other InstitutionsDocument2 pagesEconomic and Monetary Developments: Forecasts by Other InstitutionsaldhibahNo ratings yet

- IIFLAMC Multicap Advantage Presentation Online Version December 2017Document32 pagesIIFLAMC Multicap Advantage Presentation Online Version December 2017paresh revarNo ratings yet

- 122011011P1T099Document1 page122011011P1T099L'z TaylorNo ratings yet

- DL Ecb - Fsr201805.enDocument12 pagesDL Ecb - Fsr201805.enIK CleeseNo ratings yet

- Q2 2020 Earnings Presentation American Tower CorporationDocument25 pagesQ2 2020 Earnings Presentation American Tower CorporationKenya ToledoNo ratings yet

- Bop Annual 2008 PDFDocument65 pagesBop Annual 2008 PDFKhNo ratings yet

- The Overview of Taiwanese Petrochem..Document5 pagesThe Overview of Taiwanese Petrochem..林正忠No ratings yet

- The Power of The Royalty Business Model: Gold vs. Gold Miners vs. Franco NevadaDocument7 pagesThe Power of The Royalty Business Model: Gold vs. Gold Miners vs. Franco NevadaTodd SullivanNo ratings yet

- A58c7b3ed5d7d4-Operator-S-Manual-Rev01-2017-03 (Motor Checo)Document88 pagesA58c7b3ed5d7d4-Operator-S-Manual-Rev01-2017-03 (Motor Checo)ToniNo ratings yet

- Budget DeficitsDocument1 pageBudget Deficitsrick_mills8181No ratings yet

- Book 1Document2 pagesBook 1Francisc MozesNo ratings yet

- Investitii GermaniaDocument4 pagesInvestitii GermaniaCristea NicolaeNo ratings yet

- Inddec 10Document12 pagesInddec 10Surbhi SarnaNo ratings yet

- Change in StockDocument75 pagesChange in Stockrajat ranjanNo ratings yet

- LNL Iklcqd /: Page 1 of 14Document14 pagesLNL Iklcqd /: Page 1 of 14Narendra Singh SimghNo ratings yet

- Vol18Sabah Section2Document38 pagesVol18Sabah Section2Naziemi AhmadNo ratings yet

- Singapore's Balance Sheet 2008Document7 pagesSingapore's Balance Sheet 2008Alwin TanNo ratings yet

- F6rom 2009 Jun ADocument13 pagesF6rom 2009 Jun AInga ȚîgaiNo ratings yet

- Course Calendar 121310-022711Document2 pagesCourse Calendar 121310-022711Lisa SmithNo ratings yet

- OECD's Interim AssessmentDocument23 pagesOECD's Interim AssessmentTheGlobeandMailNo ratings yet

- Second Quarter and First Half 2013 Results: Paris, July 26, 2013Document38 pagesSecond Quarter and First Half 2013 Results: Paris, July 26, 2013Yves-donald MakoumbouNo ratings yet

- Hannah Yanoski FIN 344 Exchange Rate Project Part 1 3/4/21Document6 pagesHannah Yanoski FIN 344 Exchange Rate Project Part 1 3/4/21Hannah YanoskiNo ratings yet

- Thailand: Where Do We Stand?: COMPETITIVENESS: Thailand Is CompetitiveDocument15 pagesThailand: Where Do We Stand?: COMPETITIVENESS: Thailand Is CompetitivebegateamNo ratings yet

- AIN Conomic Ndicators: Ashemite Ingdom of OrdanDocument16 pagesAIN Conomic Ndicators: Ashemite Ingdom of OrdanbamakuNo ratings yet

- BIS Report On Derivatives - Year End 2008Document24 pagesBIS Report On Derivatives - Year End 2008Terry Tate BuffettNo ratings yet

- ScotiaBank JUN 11 Weekly TrendDocument9 pagesScotiaBank JUN 11 Weekly TrendMiir ViirNo ratings yet

- Schroder GAIA Egerton Equity: Quarterly Fund UpdateDocument8 pagesSchroder GAIA Egerton Equity: Quarterly Fund UpdatejackefellerNo ratings yet

- 04 - 03 Practica de Formulas MatricialesDocument9 pages04 - 03 Practica de Formulas MatricialesDaniel Marcelo VelasquezNo ratings yet

- DNB Report Bre Weekly No277Document4 pagesDNB Report Bre Weekly No277Miquel PuertasNo ratings yet

- General Journal Entries: Jurnal Entries Pension Expense Pension Liability CashDocument6 pagesGeneral Journal Entries: Jurnal Entries Pension Expense Pension Liability CashREG.B/0118104021/MEILANI PUTRINo ratings yet

- Global Recovery Advances But Remains Uneven: Embargoed Until ReleaseDocument9 pagesGlobal Recovery Advances But Remains Uneven: Embargoed Until ReleaseJoaquín Vergara BengoecheaNo ratings yet

- Chapter 8Document24 pagesChapter 8Dhruv DaveNo ratings yet

- Mese en Bilten 1. 2008 /: Monthly Bulletin 1. 2008Document3 pagesMese en Bilten 1. 2008 /: Monthly Bulletin 1. 2008emilija prodanoskaNo ratings yet

- International Macroeconomics 4th Edition Feenstra Solutions ManualDocument25 pagesInternational Macroeconomics 4th Edition Feenstra Solutions ManualElizabethPhillipsfztqc100% (64)

- Important Question Papers ICSE Class XII Maths 2009 Solved Moving AverageDocument7 pagesImportant Question Papers ICSE Class XII Maths 2009 Solved Moving AverageAnvesha AgarwalNo ratings yet

- Handout F9 Session 5Document14 pagesHandout F9 Session 5Taariq Abdul-MajeedNo ratings yet

- Security Market LineDocument5 pagesSecurity Market LineHAFIAZ MUHAMMAD IMTIAZ100% (1)

- FinanceDocument6 pagesFinancecharlie tunaNo ratings yet

- Creating Value Through Required ReturnDocument74 pagesCreating Value Through Required Returnriz4winNo ratings yet

- Research Methodology of Portfolio ManagementDocument6 pagesResearch Methodology of Portfolio ManagementZalak Shah100% (1)

- Risk and Retrun TheoryDocument40 pagesRisk and Retrun TheorySonakshi TayalNo ratings yet

- BF330 FPD 7 2020 2Document58 pagesBF330 FPD 7 2020 2richard kapimpaNo ratings yet

- Chap010 Text Bank (1) SolutionDocument22 pagesChap010 Text Bank (1) SolutionPrang ErokinNo ratings yet

- Project Report On Risk MGT in Life InsuranceDocument75 pagesProject Report On Risk MGT in Life InsurancePuja Singh80% (5)

- Security Analysis and Portfolio Management Questions and AnswersDocument15 pagesSecurity Analysis and Portfolio Management Questions and AnswersPashminaDoshiNo ratings yet

- Credit Risk Management Lecture 5Document79 pagesCredit Risk Management Lecture 5ameeque khaskheliNo ratings yet

- Types of RiskDocument7 pagesTypes of RiskMaruf AhmedNo ratings yet

- Capm ApmDocument6 pagesCapm ApmmedolinjacNo ratings yet

- 2021 July ADocument10 pages2021 July AAmar Farhan b. Abdul JalilNo ratings yet

- Test Bank For Financial Management For Decision Makers Second Canadian Edition 2 e 2nd Edition Peter Atrill Paul Hurley DownloadDocument18 pagesTest Bank For Financial Management For Decision Makers Second Canadian Edition 2 e 2nd Edition Peter Atrill Paul Hurley Downloadbriannacochrankaoesqinxw100% (19)

- Weekly Quiz 2Document30 pagesWeekly Quiz 2Emmmanuel ArthurNo ratings yet

- ACC501 Solved FinaltermDocument96 pagesACC501 Solved Finaltermdani100% (1)

- Bac 408 ModuleDocument54 pagesBac 408 ModuleJustus MasambaNo ratings yet

- Equities and Portfolio ManagementDocument55 pagesEquities and Portfolio ManagementAK Creations100% (1)

- Treynor-Black Model Presentation - Group 09Document15 pagesTreynor-Black Model Presentation - Group 09UNNATI SHUKLANo ratings yet

- Risk and Return PDFDocument14 pagesRisk and Return PDFluv silenceNo ratings yet

- AF208 Testbank CompiledDocument100 pagesAF208 Testbank Compileds11186706No ratings yet

- Risks and Risk Management in Banking by Edutap Rbi Course PDFDocument19 pagesRisks and Risk Management in Banking by Edutap Rbi Course PDFPiyush Chauhan0% (1)

- Unit 4 Derivatives Part 1Document19 pagesUnit 4 Derivatives Part 1UnathiNo ratings yet

- Sharpe's Single Index ModelDocument27 pagesSharpe's Single Index ModelVaidyanathan Ravichandran100% (2)

- You Own Stock in The Lewis Striden Drug Company Suppose YouDocument1 pageYou Own Stock in The Lewis Striden Drug Company Suppose YouAmit PandeyNo ratings yet

- Chapter 17Document21 pagesChapter 17pvaibhyNo ratings yet

- Performance Evaluation of Mutual Funds in Pakistan For The Period 2004-2008Document13 pagesPerformance Evaluation of Mutual Funds in Pakistan For The Period 2004-2008Mustafa ShabbarNo ratings yet

- Presentation TO FIN 6000 CLASS - SUMMER 2012: INSTRUCTOR: Prof. F.M. GatumoDocument25 pagesPresentation TO FIN 6000 CLASS - SUMMER 2012: INSTRUCTOR: Prof. F.M. GatumogatimupNo ratings yet

- Chapter 8: Risk and ReturnDocument56 pagesChapter 8: Risk and ReturnMohamed HussienNo ratings yet