You might also like

- Mobile Money Guidelines in NigeriaDocument24 pagesMobile Money Guidelines in Nigerialine MANNo ratings yet

- Exposure Draft On E-KYC PDFDocument18 pagesExposure Draft On E-KYC PDFShamsulfahmi Shamsudin100% (1)

- Short TitleDocument16 pagesShort Titleዝምታ ተሻለNo ratings yet

- Operational Guidelines For Open Banking in NigeriaDocument68 pagesOperational Guidelines For Open Banking in NigeriaCYNTHIA Jumoke100% (1)

- BSP Circular No. 1166 S. 2023Document26 pagesBSP Circular No. 1166 S. 2023Bernadette Kaye DumaNo ratings yet

- Ipr & Technology Bulletin Technology and Electronic Payment System in IndiaDocument7 pagesIpr & Technology Bulletin Technology and Electronic Payment System in IndiaVivek DubeyNo ratings yet

- Mobile Payments Systems GuidelinesDocument20 pagesMobile Payments Systems Guidelinesmohammad zameenNo ratings yet

- An Overview of The Regulatory Framework of FinTech in Nigeria - Fin Tech - Nigeria PDFDocument9 pagesAn Overview of The Regulatory Framework of FinTech in Nigeria - Fin Tech - Nigeria PDFAjiboye TooniNo ratings yet

- Annex 1 - E-Money (Transtech)Document4 pagesAnnex 1 - E-Money (Transtech)Sarah Jean CaneteNo ratings yet

- E Banking RulesDocument36 pagesE Banking RulesRohit KhuranaNo ratings yet

- E-KYC Exposure DraftDocument26 pagesE-KYC Exposure DraftLeslie FernandezNo ratings yet

- Circular and Exposure Draft On The Framework For BVN Operations and WatchlistDocument16 pagesCircular and Exposure Draft On The Framework For BVN Operations and WatchlistFrancis OkonkwoNo ratings yet

- BSP Circular No 268-2000-1Document5 pagesBSP Circular No 268-2000-1narcoleptic_insomaniacNo ratings yet

- SEBI Master Circular On PMLADocument31 pagesSEBI Master Circular On PMLAharshalaNo ratings yet

- QR CODE-BOT Draft V1.0 - 271120192Document19 pagesQR CODE-BOT Draft V1.0 - 271120192Nairobian SumukhNo ratings yet

- Issues To Undertake A Project or An AssignmentDocument40 pagesIssues To Undertake A Project or An AssignmentJOHANNES WondeyNo ratings yet

- Annex 6 Mobile and Agent Banking Pilot ReportDocument20 pagesAnnex 6 Mobile and Agent Banking Pilot ReportAbdiazizNo ratings yet

- 702 Issuance and Operations of Electronic MoneyDocument4 pages702 Issuance and Operations of Electronic MoneyHiraeth WeltschmerzNo ratings yet

- Summary of Payment Systems and Services Act, 2019 (Act 987)Document15 pagesSummary of Payment Systems and Services Act, 2019 (Act 987)Bernet AnimNo ratings yet

- BPRD Circular No. 10 of 2019 C10-Branchless-Banking-RegulationsDocument26 pagesBPRD Circular No. 10 of 2019 C10-Branchless-Banking-RegulationsArshia ZamirNo ratings yet

- CBK GUIDELINES MOBILE PAYMENT AMLDocument10 pagesCBK GUIDELINES MOBILE PAYMENT AMLashuumusungugmailcomNo ratings yet

- Licensing Framework For Digital BanksDocument27 pagesLicensing Framework For Digital BanksHarsimran Kaur VirkNo ratings yet

- eKYC PDFDocument26 pageseKYC PDFChrisNo ratings yet

- BSP Circular 1055Document3 pagesBSP Circular 1055MARC CHRISTIAN LOPEZ100% (2)

- Guidelines On Operations of Bank Accounts For Virtual Asset ProvidersDocument12 pagesGuidelines On Operations of Bank Accounts For Virtual Asset ProvidersMuritala JinaduNo ratings yet

- How RBI Is Changing Trends in M-PaymentDocument14 pagesHow RBI Is Changing Trends in M-PaymentVikash GopalanNo ratings yet

- Section No: A. PurposeDocument24 pagesSection No: A. Purposepuja_sarkar_2No ratings yet

- India - RBI Mobile Banking Guidelines - 20081010 Via Medianama - ComDocument7 pagesIndia - RBI Mobile Banking Guidelines - 20081010 Via Medianama - Commixedbag100% (3)

- Annex - IDocument9 pagesAnnex - IRicha RaghuvanshiNo ratings yet

- Rules and Regulations Governing The Philippine Payment and Settlement System (Philpass)Document9 pagesRules and Regulations Governing The Philippine Payment and Settlement System (Philpass)CPMMNo ratings yet

- Guidelines For Cheque Truncation in Nigeria - March 14 2012Document21 pagesGuidelines For Cheque Truncation in Nigeria - March 14 2012Jessica WeightNo ratings yet

- ENG PBI 18 40 PBI 2016 Pemrosesan Transaksi PembayaranDocument36 pagesENG PBI 18 40 PBI 2016 Pemrosesan Transaksi PembayaranFariz GhassenNo ratings yet

- Master Direction On Digital Payment Security ControlsDocument10 pagesMaster Direction On Digital Payment Security Controlsgolfclashpd1No ratings yet

- 701 Electronic Banking ServicesDocument5 pages701 Electronic Banking ServicesHiraeth WeltschmerzNo ratings yet

- Framework For Regulatory Sandbox OperationsDocument15 pagesFramework For Regulatory Sandbox Operationskuforiji fikunayoNo ratings yet

- SGAGSDHDocument14 pagesSGAGSDHharshul yadavNo ratings yet

- UntitledDocument33 pagesUntitledKristine Grace Noceda ArangNo ratings yet

- PD Merchant Acquiring ServicesDocument69 pagesPD Merchant Acquiring Servicesnerz8830No ratings yet

- Mobile Banking PolicyDocument12 pagesMobile Banking PolicySuraj GCNo ratings yet

- SBP Guidelines for Clearing OperationsDocument13 pagesSBP Guidelines for Clearing OperationsAli ShahbazNo ratings yet

- AP Intraregional IRF GuideDocument20 pagesAP Intraregional IRF GuideMenot OmarNo ratings yet

- RBI Money Laundering ComplianceDocument5 pagesRBI Money Laundering ComplianceshubhamNo ratings yet

- Fil-R-01 Mobile Financial Services Regulation Eng Final Website 4-4-2016 - 5Document10 pagesFil-R-01 Mobile Financial Services Regulation Eng Final Website 4-4-2016 - 5Maria MidiriNo ratings yet

- Bank of Thailand Regulations on Interest and FeesDocument52 pagesBank of Thailand Regulations on Interest and FeesMuay Muay PSNo ratings yet

- RBI Discussion PaperDocument18 pagesRBI Discussion PaperRuletaNo ratings yet

- PD Digital Currency v.14 14.12.17Document51 pagesPD Digital Currency v.14 14.12.17Li ZhenNo ratings yet

- Guidelines On International Money Transfer Services in Nigeria Approved DDocument19 pagesGuidelines On International Money Transfer Services in Nigeria Approved DmayorladNo ratings yet

- RBI Digital Payment 2021 FebDocument22 pagesRBI Digital Payment 2021 FebRajkumarmishra31No ratings yet

- Nextstag Communication Pvt. LTD: Micro-AtmDocument21 pagesNextstag Communication Pvt. LTD: Micro-Atmchintan310No ratings yet

- Nigerian Payments System Risk and Information Security Management FrameworkDocument23 pagesNigerian Payments System Risk and Information Security Management FrameworkKawtar MoNo ratings yet

- Nigeria Mobile Number Portability Business RulesDocument60 pagesNigeria Mobile Number Portability Business RulesMaxNo ratings yet

- Amended Branch Less Banking Regulations - 6!20!2011Document37 pagesAmended Branch Less Banking Regulations - 6!20!2011syedjanNo ratings yet

- Truncated Cheque Clearance Procedures Case StudyDocument31 pagesTruncated Cheque Clearance Procedures Case Studyjhanvi75% (4)

- MNP Porting Process Guidelines 280410Document34 pagesMNP Porting Process Guidelines 280410Qais KaisraniNo ratings yet

- Payment Systems in India: Reserve Bank of IndiaDocument16 pagesPayment Systems in India: Reserve Bank of IndiaRahul BadaniNo ratings yet

- Payment System Oversight FrameworkDocument16 pagesPayment System Oversight FrameworkNarayanPrajapatiNo ratings yet

- Electronic Clearing ServiceDocument41 pagesElectronic Clearing Servicejsdhilip0% (1)

- Pbi 230621 enDocument199 pagesPbi 230621 enGerald de BrittoNo ratings yet

- BSP Circular No. 944-2017 (Guidelines For Virtual Currency (VC) Exchanges)Document6 pagesBSP Circular No. 944-2017 (Guidelines For Virtual Currency (VC) Exchanges)Bobby Olavides SebastianNo ratings yet

- Acquiring New Knowledge: Module 26 AgricultureDocument10 pagesAcquiring New Knowledge: Module 26 AgricultureAngelica Sanchez de VeraNo ratings yet

- Government Incentives For EntrepreneurshipDocument3 pagesGovernment Incentives For EntrepreneurshipCato InstituteNo ratings yet

- CMA Exam Review - Strategic Planning ToolsDocument67 pagesCMA Exam Review - Strategic Planning ToolsLe BlancNo ratings yet

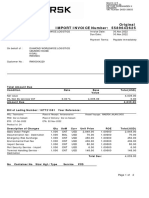

- Original IMPORT INVOICE Number: 5589642625: Total Amount Due Condition Rate Base Value Total (USD)Document2 pagesOriginal IMPORT INVOICE Number: 5589642625: Total Amount Due Condition Rate Base Value Total (USD)AllyNo ratings yet

- Managing Uncertainty During A Global PandemicDocument6 pagesManaging Uncertainty During A Global PandemicJuvy AguirreNo ratings yet

- Dusty R BouthilletteDocument16 pagesDusty R Bouthillettedanw5646No ratings yet

- MIT18 S096F13 Lecnote14Document34 pagesMIT18 S096F13 Lecnote14eni100% (1)

- Technics Oil & Gas: Initiation of CoverageDocument15 pagesTechnics Oil & Gas: Initiation of Coveragecentaurus553587No ratings yet

- Part III Money Market (Revised For 2e)Document31 pagesPart III Money Market (Revised For 2e)Harun MusaNo ratings yet

- Functional Definition of Insurance: MeaningDocument6 pagesFunctional Definition of Insurance: MeaningShubham DhimaanNo ratings yet

- Jurnal PajakDocument43 pagesJurnal PajakIndahNo ratings yet

- Bill statement chargesDocument6 pagesBill statement chargesjjayNo ratings yet

- Module 5: What You Will LearnDocument54 pagesModule 5: What You Will Learn刘宝英No ratings yet

- My CA Articleship Experience of Working at Deloitte (Big 4)Document5 pagesMy CA Articleship Experience of Working at Deloitte (Big 4)Rudrin Das100% (1)

- Harpoon Pricing Strategies PDFDocument37 pagesHarpoon Pricing Strategies PDFAmith SoyzaNo ratings yet

- 905 XXXXXXXXX 20267Document2 pages905 XXXXXXXXX 20267snbnbbNo ratings yet

- 17Q June 2016Document95 pages17Q June 2016Juliana ChengNo ratings yet

- Market CapitalitationDocument2 pagesMarket CapitalitationRahul PanwarNo ratings yet

- Short-Term Budgeting: (Problem 1)Document18 pagesShort-Term Budgeting: (Problem 1)princess bubblegumNo ratings yet

- Mathematics of Finance: Faculty of Business Studies (FBS) Bangladesh University of Professionals (BUP)Document52 pagesMathematics of Finance: Faculty of Business Studies (FBS) Bangladesh University of Professionals (BUP)Sadia Afrin ArinNo ratings yet

- Financial Statement Analysis: Presenter's Name Presenter's Title DD Month YyyyDocument79 pagesFinancial Statement Analysis: Presenter's Name Presenter's Title DD Month Yyyyjohny BraveNo ratings yet

- Explain How Interest Rates Can Affect Supply and DemandDocument2 pagesExplain How Interest Rates Can Affect Supply and Demandhafeez ahmedNo ratings yet

- Idx Monthly Oct 2023Document154 pagesIdx Monthly Oct 2023ikhsan AdiNo ratings yet

- Natco Medicine CompanyDocument12 pagesNatco Medicine CompanyPawan SoniNo ratings yet

- Funding Amount (INR)Document8 pagesFunding Amount (INR)Rahul PatelNo ratings yet

- Fdi & FiiDocument38 pagesFdi & FiiJitendra KalwaniNo ratings yet

- Unbilled Transactions PDFDocument2 pagesUnbilled Transactions PDFArjun NkNo ratings yet

- Fixed Asset and Depreciation Schedule: Instructions: InputsDocument5 pagesFixed Asset and Depreciation Schedule: Instructions: InputsPatrick GhariosNo ratings yet

- Unit 1 Portfolio Activity Review of Key Financial StatementsDocument4 pagesUnit 1 Portfolio Activity Review of Key Financial StatementsSimran PannuNo ratings yet

- Andrew AngDocument3 pagesAndrew AngShane Kimberly LubatNo ratings yet

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindFrom EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindRating: 5 out of 5 stars5/5 (231)

- Love Your Life Not Theirs: 7 Money Habits for Living the Life You WantFrom EverandLove Your Life Not Theirs: 7 Money Habits for Living the Life You WantRating: 4.5 out of 5 stars4.5/5 (146)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)From EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Rating: 4.5 out of 5 stars4.5/5 (12)

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!From EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Rating: 4.5 out of 5 stars4.5/5 (14)

- Financial Accounting For Dummies: 2nd EditionFrom EverandFinancial Accounting For Dummies: 2nd EditionRating: 5 out of 5 stars5/5 (10)

- Profit First for Therapists: A Simple Framework for Financial FreedomFrom EverandProfit First for Therapists: A Simple Framework for Financial FreedomNo ratings yet

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)From EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Rating: 4.5 out of 5 stars4.5/5 (5)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- Excel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetFrom EverandExcel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetNo ratings yet

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)From EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Rating: 4 out of 5 stars4/5 (33)

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 5 out of 5 stars5/5 (1)

- Business Valuation: Private Equity & Financial Modeling 3 Books In 1: 27 Ways To Become A Successful Entrepreneur & Sell Your Business For BillionsFrom EverandBusiness Valuation: Private Equity & Financial Modeling 3 Books In 1: 27 Ways To Become A Successful Entrepreneur & Sell Your Business For BillionsNo ratings yet

- LLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyFrom EverandLLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyRating: 5 out of 5 stars5/5 (1)

- SAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsFrom EverandSAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsNo ratings yet

- Basic Accounting: Service Business Study GuideFrom EverandBasic Accounting: Service Business Study GuideRating: 5 out of 5 stars5/5 (2)

- Accounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsFrom EverandAccounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsRating: 4 out of 5 stars4/5 (7)

- Emprender un Negocio: Paso a Paso Para PrincipiantesFrom EverandEmprender un Negocio: Paso a Paso Para PrincipiantesRating: 3 out of 5 stars3/5 (1)

- NLP:The Essential Handbook for Business: The Essential Handbook for Business: Communication Techniques to Build Relationships, Influence Others, and Achieve Your GoalsFrom EverandNLP:The Essential Handbook for Business: The Essential Handbook for Business: Communication Techniques to Build Relationships, Influence Others, and Achieve Your GoalsRating: 4.5 out of 5 stars4.5/5 (4)

- Bookkeeping: An Essential Guide to Bookkeeping for Beginners along with Basic Accounting PrinciplesFrom EverandBookkeeping: An Essential Guide to Bookkeeping for Beginners along with Basic Accounting PrinciplesRating: 4.5 out of 5 stars4.5/5 (30)

- The Big Four: The Curious Past and Perilous Future of the Global Accounting MonopolyFrom EverandThe Big Four: The Curious Past and Perilous Future of the Global Accounting MonopolyRating: 4 out of 5 stars4/5 (4)

- Full Charge Bookkeeping, For the Beginner, Intermediate & Advanced BookkeeperFrom EverandFull Charge Bookkeeping, For the Beginner, Intermediate & Advanced BookkeeperRating: 5 out of 5 stars5/5 (3)