You might also like

- Franklin Covey Sample PlannerDocument45 pagesFranklin Covey Sample Plannerdynamico0100% (12)

- 100 Baggers PDFDocument202 pages100 Baggers PDFAmitabhDash97% (58)

- Habit Busting by Pete CohenDocument175 pagesHabit Busting by Pete CohenSirajGhumroNo ratings yet

- Habit Busting by Pete CohenDocument175 pagesHabit Busting by Pete CohenSirajGhumroNo ratings yet

- CSR Group Activity - Week 4Document3 pagesCSR Group Activity - Week 4Kenisha ManicksinghNo ratings yet

- Harley-Davidson: 29.4 20.0 Recent Price P/E Ratio Relative P/E Ratio Div'D YLDDocument1 pageHarley-Davidson: 29.4 20.0 Recent Price P/E Ratio Relative P/E Ratio Div'D YLDBrent UptonNo ratings yet

- Walmart Inc PDFDocument1 pageWalmart Inc PDFWaqar AhmedNo ratings yet

- SF No 28 Kadhampadi ModelDocument1 pageSF No 28 Kadhampadi ModelmanojNo ratings yet

- SF No 28 Kadhampadi ModelDocument1 pageSF No 28 Kadhampadi ModelmanojNo ratings yet

- Apple - Report PDFDocument1 pageApple - Report PDFUwie AndrianaNo ratings yet

- Link Net Company Presentation - Investor UpdateDocument47 pagesLink Net Company Presentation - Investor UpdateumarhidayatNo ratings yet

- Bby AaDocument1 pageBby AalondonmorganNo ratings yet

- 6754 DatasheetDocument1 page6754 DatasheetSuryakanth KattimaniNo ratings yet

- Spiva Us Year End 2021Document39 pagesSpiva Us Year End 2021Hyenuk ChuNo ratings yet

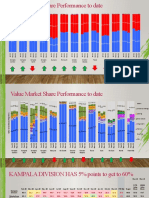

- Kampala Central Kampala East Kampala North Kampala South Bunyoro Far South Greater Ankole Greater Masaka Tooro East Far East North West NileDocument4 pagesKampala Central Kampala East Kampala North Kampala South Bunyoro Far South Greater Ankole Greater Masaka Tooro East Far East North West NileBenjamin SsematubiNo ratings yet

- SRMPCDocument3 pagesSRMPCBHANUKRISHNA VISAKOTANo ratings yet

- Nextera Library Validation and Cluster Density OptimizationDocument2 pagesNextera Library Validation and Cluster Density OptimizationhellowinstonNo ratings yet

- Fund Report - Pure Stock Fund - Aug 2021Document3 pagesFund Report - Pure Stock Fund - Aug 2021faleela IsmailNo ratings yet

- European Union Labour Force Survey-Annual Results 2008: Population and Social Conditions 33/2009Document8 pagesEuropean Union Labour Force Survey-Annual Results 2008: Population and Social Conditions 33/2009ekonimija86No ratings yet

- Intervalos Musicales Puros en Escala Loraritmica de Base 2Document1 pageIntervalos Musicales Puros en Escala Loraritmica de Base 2Felipe RodríguezNo ratings yet

- VFD HarmonicsDocument1 pageVFD HarmonicstwinvbooksNo ratings yet

- Session 8 - Fiscal Policy - Part 2Document19 pagesSession 8 - Fiscal Policy - Part 2Anurag DharNo ratings yet

- Total Hydrocarbon Content (THC) Testing in Liquid Oxygen (LOX)Document9 pagesTotal Hydrocarbon Content (THC) Testing in Liquid Oxygen (LOX)mario oteroNo ratings yet

- GEA - Bock - SemiHerm - Catalogue - GB 4Document1 pageGEA - Bock - SemiHerm - Catalogue - GB 4hadi mehrabiNo ratings yet

- Book 2Document1 pageBook 2Abu TalhaNo ratings yet

- Monitor de SequiaDocument7 pagesMonitor de Sequiass.sefi.infraestructuraNo ratings yet

- SKANDA HILLS - D BLOCK LAYOUT PLAN FOR MARKETING-Model-8 PDFDocument1 pageSKANDA HILLS - D BLOCK LAYOUT PLAN FOR MARKETING-Model-8 PDFR DAMODARNo ratings yet

- Pongalur 232,242 1NNDocument1 pagePongalur 232,242 1NNGeo Mapl InfraNo ratings yet

- No 04 97Document1 pageNo 04 97widibae jokotholeNo ratings yet

- Think and HistoryDocument1 pageThink and HistoryfaizNo ratings yet

- Planta 1er Piso Planta 2do Piso: Corte A-ADocument1 pagePlanta 1er Piso Planta 2do Piso: Corte A-ANacho Sepulveda SagalNo ratings yet

- Evaluasi & Optimalisasi Capaian Program Dan Kegiatan Yang Mendukung Capaian SPM Bidang Kesehatan Di Kab. Wonosobo TAHUN 2018Document42 pagesEvaluasi & Optimalisasi Capaian Program Dan Kegiatan Yang Mendukung Capaian SPM Bidang Kesehatan Di Kab. Wonosobo TAHUN 2018Anonymous dxMzYhQR8No ratings yet

- Bby 2008Document1 pageBby 2008londonmorganNo ratings yet

- THM0044014S6Document1 pageTHM0044014S6Srf Saharin100% (1)

- VDS MasterplanDocument1 pageVDS MasterplanSamudrala SreepranaviNo ratings yet

- Materi Pak YunartoDocument13 pagesMateri Pak YunartoAsiska SiswiyonoNo ratings yet

- What Is TDS?: Usage Instructions Temperature Conversion ChartDocument2 pagesWhat Is TDS?: Usage Instructions Temperature Conversion ChartyierbNo ratings yet

- BP Stats Review 2019 Full Report 43Document1 pageBP Stats Review 2019 Full Report 43Sakaros BogningNo ratings yet

- Gonorrhea: Sexually Transmitted Disease Surveillance 2000Document12 pagesGonorrhea: Sexually Transmitted Disease Surveillance 2000Srinivas KasiNo ratings yet

- The Graduate Course in Electromagnetics: Integrating The Past, Present, and FutureDocument34 pagesThe Graduate Course in Electromagnetics: Integrating The Past, Present, and FutureAntonioAguiarNo ratings yet

- B400 B700 ManualDocument2 pagesB400 B700 ManualMultiservicios aqualectNo ratings yet

- GEA - Bock - SemiHerm - Catalogue - GB 18Document1 pageGEA - Bock - SemiHerm - Catalogue - GB 18hadi mehrabiNo ratings yet

- Acoustics AVR ModelDocument1 pageAcoustics AVR ModelChelsea Wenceslao AmistadNo ratings yet

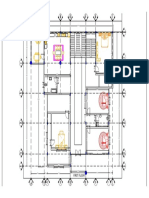

- Second Floor Plan: Proposed Two (2) - Storey Commercial Building With RoofdeckDocument1 pageSecond Floor Plan: Proposed Two (2) - Storey Commercial Building With Roofdeckdante mortelNo ratings yet

- Chuyên đề 3a - Biểu thuế XNK Việt NamDocument48 pagesChuyên đề 3a - Biểu thuế XNK Việt NamThao BuiNo ratings yet

- Precipitación de Los Años 1997-2010Document8 pagesPrecipitación de Los Años 1997-2010Vanessa Vera ReyesNo ratings yet

- 8-Baf - DP 3045 MT 234 Motor 1,2kw AtexDocument5 pages8-Baf - DP 3045 MT 234 Motor 1,2kw AtexSantiago RodaNo ratings yet

- Historico PIB MexicoDocument1 pageHistorico PIB MexicoJUAN SINMIEDONo ratings yet

- Hardscape Layout-ModelDocument1 pageHardscape Layout-ModelJannet RodriguezNo ratings yet

- VSX 6154 V2Document1 pageVSX 6154 V2Hira SinghNo ratings yet

- Aecom 23-Nov-23 Ccs123 DraftDocument33 pagesAecom 23-Nov-23 Ccs123 DraftakshayNo ratings yet

- Manual Pressureswitch b400 b700 SnapactDocument2 pagesManual Pressureswitch b400 b700 SnapactDickson ChungNo ratings yet

- Intervalos Musicales Puros Relación de FrecuenciasDocument1 pageIntervalos Musicales Puros Relación de FrecuenciasFelipe RodríguezNo ratings yet

- Lead Screw Phi 18Document1 pageLead Screw Phi 18bhageshlNo ratings yet

- Mba I SemDocument58 pagesMba I Semshrutiv vishwakarmaNo ratings yet

- First TT TTTTTDocument1 pageFirst TT TTTTTAbdirizak HusseinNo ratings yet

- First TT TTTTTDocument1 pageFirst TT TTTTTAbdirizak HusseinNo ratings yet

- Plan de Travail Cotes DéfinitivesDocument1 pagePlan de Travail Cotes DéfinitivesSergey YusupovNo ratings yet

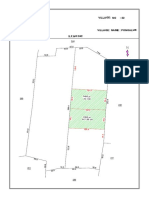

- Farmland DimensionsDocument1 pageFarmland DimensionsKumar KingslyNo ratings yet

- SDP NewDocument1 pageSDP NewJulie Ann GutierrezNo ratings yet

- Sodapdf MergedDocument5 pagesSodapdf MergedBartolome, Rohan Siegfried B.No ratings yet

- Pakistan's Air Transportation SystemDocument22 pagesPakistan's Air Transportation SystemAMNANo ratings yet

- MW 04/08/2013 - RELEASED ON ECO: 500007751: Maximum Weight Capacity 75 LBS. 34.1 KGSDocument2 pagesMW 04/08/2013 - RELEASED ON ECO: 500007751: Maximum Weight Capacity 75 LBS. 34.1 KGSJesus Daniel Diaz de Guzman DiazNo ratings yet

- Shruti Vishwakarma Mba I Sem Moe 2021mba015Document81 pagesShruti Vishwakarma Mba I Sem Moe 2021mba015shrutiv vishwakarmaNo ratings yet

- 2023 - Q1 Press Release BAM - FDocument9 pages2023 - Q1 Press Release BAM - FJ Pierre RicherNo ratings yet

- Dispelling Myths in The Value vs. Growth Debate: Quarterly Letter 2Q 2021Document11 pagesDispelling Myths in The Value vs. Growth Debate: Quarterly Letter 2Q 2021Xavier StraussNo ratings yet

- 2023 - Q1 Supplemental - BAM - FinalDocument40 pages2023 - Q1 Supplemental - BAM - FinalJ Pierre Richer100% (1)

- 2022 Full Annual ReportDocument234 pages2022 Full Annual ReportJ Pierre RicherNo ratings yet

- Amalthea Letter 202106Document7 pagesAmalthea Letter 202106J Pierre RicherNo ratings yet

- THE Brookfield WAY: Real Estate SpecialDocument11 pagesTHE Brookfield WAY: Real Estate SpecialJ Pierre RicherNo ratings yet

- Bam 2021 Q2interim FDocument92 pagesBam 2021 Q2interim FJ Pierre RicherNo ratings yet

- SANW Q218 Presentation March 2018 FINALDocument38 pagesSANW Q218 Presentation March 2018 FINALJ Pierre RicherNo ratings yet

- Brookfield Transforming Businesses For A Zero-Carbon World - 0Document19 pagesBrookfield Transforming Businesses For A Zero-Carbon World - 0J Pierre RicherNo ratings yet

- 1 Quarter Commentary: Arket OmmentaryDocument34 pages1 Quarter Commentary: Arket OmmentaryJ Pierre RicherNo ratings yet

- Under The Hood ETF Based IndexationDocument5 pagesUnder The Hood ETF Based IndexationJ Pierre RicherNo ratings yet

- 01GreenwaldonGraham PDFDocument11 pages01GreenwaldonGraham PDFJ Pierre RicherNo ratings yet

- CFA Society Talk in DelhiDocument70 pagesCFA Society Talk in DelhiKushal JawliaNo ratings yet

- Navigating The New Normal David A. RosenbergDocument73 pagesNavigating The New Normal David A. Rosenbergannawitkowski88No ratings yet

- Benjamin Graham The Memoirs of The Dean of Wall Street ExcerptDocument65 pagesBenjamin Graham The Memoirs of The Dean of Wall Street ExcerptJ Pierre RicherNo ratings yet

- SSRN Id1970250Document55 pagesSSRN Id1970250J Pierre RicherNo ratings yet

- BIS Annual Report 2011 - 2012Document214 pagesBIS Annual Report 2011 - 2012limesinferiorNo ratings yet

- Bengraham ValuationtechniqueclassnotesDocument5 pagesBengraham ValuationtechniqueclassnotesJ Pierre RicherNo ratings yet

- THOUFIQ Resume MbaDocument3 pagesTHOUFIQ Resume MbanaveenNo ratings yet

- L1F21BBAM0233Document4 pagesL1F21BBAM0233Ahmad KakarNo ratings yet

- Causes and Effects Into Reasons For The Decline of Wood Cable Reels Production in The CompanyDocument7 pagesCauses and Effects Into Reasons For The Decline of Wood Cable Reels Production in The CompanyQueryy DavidNo ratings yet

- FIN 073 P1 Exam PDFDocument8 pagesFIN 073 P1 Exam PDFRiamē NonøNo ratings yet

- MBA Finance (Production Functions: CH 3) MBS (Production and Cost Analysis: CH 3) MBM (Theory of Production and Cost: Ch3)Document48 pagesMBA Finance (Production Functions: CH 3) MBS (Production and Cost Analysis: CH 3) MBM (Theory of Production and Cost: Ch3)Saru Regmi100% (1)

- Internal Quality Management System Audit Checklist (ISO/TS 16949:2009)Document48 pagesInternal Quality Management System Audit Checklist (ISO/TS 16949:2009)sharif1974No ratings yet

- Middle & Back Office Treasury ManagementDocument3 pagesMiddle & Back Office Treasury Managementlinkrink68890% (2)

- Major Issues in Data MiningDocument45 pagesMajor Issues in Data MiningProsper Muzenda75% (4)

- Project Report On Personal Loan CompressDocument62 pagesProject Report On Personal Loan CompressSudhakar GuntukaNo ratings yet

- Loan Agreement Paperwork of $5000.00Document8 pagesLoan Agreement Paperwork of $5000.00Alex SpecimenNo ratings yet

- RMS Stock Ledger White Paper-14.1.xDocument94 pagesRMS Stock Ledger White Paper-14.1.xanvesh5435No ratings yet

- Creating New Market Space SlidesDocument28 pagesCreating New Market Space SlidesMuhammad Raffay MaqboolNo ratings yet

- 16 - Rahul Mundada - Mudita MathurDocument8 pages16 - Rahul Mundada - Mudita MathurRahul MundadaNo ratings yet

- Tractor Supply Company Case Study 2Document1 pageTractor Supply Company Case Study 2KAR WAI PHOONNo ratings yet

- 2nd Phase TestDocument6 pages2nd Phase TestFaiza OmarNo ratings yet

- Review of Related Literature FinalDocument6 pagesReview of Related Literature Finalmacrisa caraganNo ratings yet

- Global In-House Center (GIC) Landscape in Costa Rica and Trends in Offshore GIC MarketDocument14 pagesGlobal In-House Center (GIC) Landscape in Costa Rica and Trends in Offshore GIC MarketeverestgrpNo ratings yet

- Chapter 2 - Biz ModelsDocument37 pagesChapter 2 - Biz Modelsthảo nguyễnNo ratings yet

- Chapter01.the Changing Role of Managerial Accounting in A Dynamic Business EnvironmentDocument62 pagesChapter01.the Changing Role of Managerial Accounting in A Dynamic Business EnvironmentAnjo Bautista Saip100% (1)

- Quality Principles of Deming Juran & CrosbyDocument1 pageQuality Principles of Deming Juran & CrosbyStephen De GuzmanNo ratings yet

- 3464172Document34 pages3464172Aasri RNo ratings yet

- Banasthali Vidyapith: Master of Business AdministrationDocument112 pagesBanasthali Vidyapith: Master of Business AdministrationRuchi AgarwallNo ratings yet

- Test 5-ConsolidationDocument3 pagesTest 5-ConsolidationAli OptimisticNo ratings yet

- The State Bank of IndiaDocument4 pagesThe State Bank of IndiaHimanshu JainNo ratings yet

- Ch2 Auditing IT Governance ControlsDocument39 pagesCh2 Auditing IT Governance ControlsCrazy DaveNo ratings yet

- Malaysia: Selected IssuesDocument21 pagesMalaysia: Selected Issuesالميثاق موبايلNo ratings yet

- DissertationDocument24 pagesDissertationSaima NishatNo ratings yet

- QUESTION BANK For Banking and Insurance MBA Sem IV-FinanceDocument2 pagesQUESTION BANK For Banking and Insurance MBA Sem IV-FinanceAgnya PatelNo ratings yet

- Sanofi India IAR 2022Document111 pagesSanofi India IAR 20221012914707No ratings yet