You might also like

- Adjusting Journal EntriesDocument8 pagesAdjusting Journal EntriesChaaaNo ratings yet

- Adjusting Entries For StudentsDocument57 pagesAdjusting Entries For Studentsselvia egayNo ratings yet

- Module 3 Adjusting Journal EntriesDocument25 pagesModule 3 Adjusting Journal EntriesThriztan Andrei BaluyutNo ratings yet

- Journal Entry DiscussionDocument8 pagesJournal Entry DiscussionAyesha Eunice SalvaleonNo ratings yet

- Week 7-8Document8 pagesWeek 7-8Kim Albero Cubel0% (1)

- Module 3Document47 pagesModule 3Harrold HarryNo ratings yet

- Fabm 1 - Q2 - Week 1 - Module 1 - Preparing Adjusting Entries of A Service Business - For ReproductionDocument16 pagesFabm 1 - Q2 - Week 1 - Module 1 - Preparing Adjusting Entries of A Service Business - For ReproductionJosephine C QuibidoNo ratings yet

- Learning Kit EnglishDocument3 pagesLearning Kit EnglishJoselle Cayanan LawNo ratings yet

- Adjusting EntryDocument38 pagesAdjusting EntryNicaela Margareth YusoresNo ratings yet

- Fabm2 Q2 M4 - 4 CsefDocument20 pagesFabm2 Q2 M4 - 4 CsefZeus MalicdemNo ratings yet

- QSN 2 Fabm T AccountDocument3 pagesQSN 2 Fabm T AccountKisha Del mundoNo ratings yet

- Adjusting Entries (Accruals)Document4 pagesAdjusting Entries (Accruals)Geneen LouiseNo ratings yet

- 01 Quiz 1Document2 pages01 Quiz 1Laisan SantosNo ratings yet

- Abm Fabm1 Airs LM q4-m9Document18 pagesAbm Fabm1 Airs LM q4-m9MEDILEN O. BORRESNo ratings yet

- Fabm1 Completing The Accounting CycleDocument16 pagesFabm1 Completing The Accounting CycleVeniceNo ratings yet

- Integrated Accounting Learning Module Attachment (Do Not Copy)Document15 pagesIntegrated Accounting Learning Module Attachment (Do Not Copy)Jasper PelicanoNo ratings yet

- B.1 Directions: Prepare Journal Entries For The Following Transactions Using A Periodic Inventory SystemDocument4 pagesB.1 Directions: Prepare Journal Entries For The Following Transactions Using A Periodic Inventory SystemJestine AlcantaraNo ratings yet

- Accounting Cycle of A Merchandising BusinessDocument21 pagesAccounting Cycle of A Merchandising Businesszedrick edenNo ratings yet

- Principles of Marketing GRADE 12/week 3 & 4Document6 pagesPrinciples of Marketing GRADE 12/week 3 & 4Master NistroNo ratings yet

- Statement of Financial PositionDocument7 pagesStatement of Financial PositionJay KwonNo ratings yet

- Topic: Accounting Cycle of A Service BusinessDocument5 pagesTopic: Accounting Cycle of A Service BusinessJohn Rey BusimeNo ratings yet

- Assignment November11 KylaAccountingDocument2 pagesAssignment November11 KylaAccountingADRIANO, Glecy C.No ratings yet

- Q4 ABM Fundamentals of ABM1 11 Week 4Document4 pagesQ4 ABM Fundamentals of ABM1 11 Week 4Celine Angela AbreaNo ratings yet

- Closing EntriesDocument13 pagesClosing EntriesAlliyah Manzano CalvoNo ratings yet

- ABM FABM1 AIRs LM Q3 W5 M5Document20 pagesABM FABM1 AIRs LM Q3 W5 M5Trisha Mae DuatNo ratings yet

- Rovelyn E. Forcadas ABM-11 Activity #9-BDocument2 pagesRovelyn E. Forcadas ABM-11 Activity #9-BRovelyn E. ForcadasNo ratings yet

- w1 Fabmii Review of Basic Bookkeeping Skills Part2Document18 pagesw1 Fabmii Review of Basic Bookkeeping Skills Part2Mizuki YamizakiNo ratings yet

- Adjsuting Journal EntriesDocument2 pagesAdjsuting Journal EntriesRey Luna100% (1)

- Activity Sheet Adjusting Entries DeferralsDocument1 pageActivity Sheet Adjusting Entries DeferralsShania LiwanagNo ratings yet

- Busmath Wages Salaries, Etc.Document16 pagesBusmath Wages Salaries, Etc.Aki AngelNo ratings yet

- TOPIC 2 - SCI-Single-Step (Preparation)Document6 pagesTOPIC 2 - SCI-Single-Step (Preparation)JUDITH PIANONo ratings yet

- Fabm Nites PrintDocument3 pagesFabm Nites Printwiz wizNo ratings yet

- The Accounting Process: Recording and Classifying Business TransactionsDocument15 pagesThe Accounting Process: Recording and Classifying Business TransactionsSykkuno ToastNo ratings yet

- Example For Chapter 2 (FABM2)Document10 pagesExample For Chapter 2 (FABM2)Althea BañaciaNo ratings yet

- FAR Chapter4 FinalDocument43 pagesFAR Chapter4 FinalPATRICIA COLINANo ratings yet

- Funacc1 Las Q4 Week 1 9 96 PagesDocument95 pagesFunacc1 Las Q4 Week 1 9 96 PagesCHRISTINE JOY BONDOC100% (1)

- Acctg. Equation Puring CompanyDocument8 pagesAcctg. Equation Puring CompanyAngelNo ratings yet

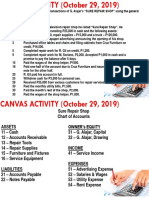

- Canvas Activity - Journalizing - Oct - 29 PDFDocument2 pagesCanvas Activity - Journalizing - Oct - 29 PDFJian Francisco100% (2)

- Chapter 6Document6 pagesChapter 6Ellen Joy PenieroNo ratings yet

- Republic of The Philippines Department of Education Region Vii, Central Visayas Division of Cebu Province Self-Learning Home Task (SLHT)Document20 pagesRepublic of The Philippines Department of Education Region Vii, Central Visayas Division of Cebu Province Self-Learning Home Task (SLHT)Joseph Entera100% (2)

- SLK Fabm1 Week 6Document8 pagesSLK Fabm1 Week 6Mylene SantiagoNo ratings yet

- Activity 1: Recording Transactions in The JournalDocument2 pagesActivity 1: Recording Transactions in The JournalSieadel Dalumpines50% (2)

- Accounting Equation Lesson 1.1Document23 pagesAccounting Equation Lesson 1.1Renz RaphNo ratings yet

- Activity:: I. Define The Following TermsDocument3 pagesActivity:: I. Define The Following TermsAnonymousNo ratings yet

- ABM 12 - Analysis and Interpretation of FS 1Document5 pagesABM 12 - Analysis and Interpretation of FS 1Wella LozadaNo ratings yet

- Fundamentals of Accountancy, Business, and Management 2: ExpectationDocument131 pagesFundamentals of Accountancy, Business, and Management 2: ExpectationAngela Garcia100% (1)

- Week 6Document11 pagesWeek 6Kim Albero CubelNo ratings yet

- Quiz 2 AnswerDocument4 pagesQuiz 2 AnswerJessa Mae Banse Limosnero100% (4)

- Fa1 Assignment #1 DacayananDocument9 pagesFa1 Assignment #1 DacayananMikha DacayananNo ratings yet

- Work Sheet in Accounting 1Document12 pagesWork Sheet in Accounting 1Nancy Atentar50% (2)

- Bookkeeping Assignment JournalizingDocument1 pageBookkeeping Assignment JournalizingPhilpNil8000No ratings yet

- Grade11 Fabm1 Q2 Week1Document22 pagesGrade11 Fabm1 Q2 Week1Mickaela MonterolaNo ratings yet

- Fabm - Q2 - Las-For LearnersDocument113 pagesFabm - Q2 - Las-For LearnersABM-AKRISTINE DELA CRUZNo ratings yet

- Grade11 Business Math - Module 4Document6 pagesGrade11 Business Math - Module 4Erickson SongcalNo ratings yet

- FABM2 Module-1Document18 pagesFABM2 Module-1Jean Carlo Delizo CacheroNo ratings yet

- Negros Occidental (ACCOUNTING1)Document7 pagesNegros Occidental (ACCOUNTING1)Maxine Ceballos Glodove100% (1)

- Saint Louis College-Cebu: (Servant Leaders For Mission)Document4 pagesSaint Louis College-Cebu: (Servant Leaders For Mission)Marc Graham NacuaNo ratings yet

- Adjusting EntriesDocument71 pagesAdjusting EntriesLeteSsie66% (29)

- Fabm Note 6Document12 pagesFabm Note 6Angelica ManahanNo ratings yet

- Types of IP AddressesDocument3 pagesTypes of IP Addressesbekalu amenuNo ratings yet

- Ansys Autodyn Users Manual PDFDocument501 pagesAnsys Autodyn Users Manual PDFRama BaruvaNo ratings yet

- Political Science, History Of: Erkki Berndtson, University of Helsinki, Helsinki, FinlandDocument6 pagesPolitical Science, History Of: Erkki Berndtson, University of Helsinki, Helsinki, FinlandRanjan Kumar SinghNo ratings yet

- (U) Daily Activity Report: Marshall DistrictDocument5 pages(U) Daily Activity Report: Marshall DistrictFauquier NowNo ratings yet

- Fourth Trumpet From The Fourth Anglican Global South To South EncounterDocument4 pagesFourth Trumpet From The Fourth Anglican Global South To South EncounterTheLivingChurchdocsNo ratings yet

- Rental ApplicationDocument1 pageRental Applicationnicholas alexanderNo ratings yet

- On Nontraditional TrademarksDocument80 pagesOn Nontraditional Trademarksshivanjay aggarwalNo ratings yet

- School AllotDocument1 pageSchool Allotamishameena294No ratings yet

- 6 Master Plans - ReviewerDocument2 pages6 Master Plans - ReviewerJue Lei0% (1)

- Bài Tập Unit 4Document7 pagesBài Tập Unit 4Nguyễn Lanh AnhNo ratings yet

- 5 Engineering - Machinery Corp. v. Court of Appeals, G.R. No. 52267, January 24, 1996.Document16 pages5 Engineering - Machinery Corp. v. Court of Appeals, G.R. No. 52267, January 24, 1996.June DoriftoNo ratings yet

- Reyes v. CA 216 SCRA 25 (1993)Document7 pagesReyes v. CA 216 SCRA 25 (1993)Karla KanashiiNo ratings yet

- Preamble of The Philippine ConstitutionDocument21 pagesPreamble of The Philippine ConstitutionKriss Luciano100% (1)

- Kant 9 ThesisDocument6 pagesKant 9 ThesisMary Montoya100% (1)

- State Common Entrance Test Cell, Maharashtra: Provisional Selection Letter (CAP 2)Document1 pageState Common Entrance Test Cell, Maharashtra: Provisional Selection Letter (CAP 2)Vrushali ShirsathNo ratings yet

- Cyber Crime PresentationDocument20 pagesCyber Crime Presentationvipin rathi78% (9)

- Xpacoac A101 5 8Document33 pagesXpacoac A101 5 8TeamACEsPH Back-up AccountNo ratings yet

- Kosse v. Kiesza Complaint PDFDocument7 pagesKosse v. Kiesza Complaint PDFMark JaffeNo ratings yet

- Walmart Morningstar ReportDocument26 pagesWalmart Morningstar ReportcmcbuyersgNo ratings yet

- Date Sheet For Pms in Service 02 2021Document1 pageDate Sheet For Pms in Service 02 2021Oceans AdvocateNo ratings yet

- OurCatholicFaith PowerPoint Chapter8Document20 pagesOurCatholicFaith PowerPoint Chapter8Jamsy PacaldoNo ratings yet

- Indira Gandhi Work DoneDocument4 pagesIndira Gandhi Work DoneRupesh DekateNo ratings yet

- Master Deed SampleDocument29 pagesMaster Deed Samplepot420_aivan0% (1)

- Quotation For Am PM Snack and Lunch 100 Pax Feu Tech 260Document3 pagesQuotation For Am PM Snack and Lunch 100 Pax Feu Tech 260Heidi Clemente50% (2)

- Rule 30 - TrialDocument5 pagesRule 30 - TrialCecil BernabeNo ratings yet

- Microsoft Dynamics AX Lean AccountingDocument26 pagesMicrosoft Dynamics AX Lean AccountingYaowalak Sriburadej100% (2)

- A Case Study in The Historical and Political Background of Barangay 77 Banez VillDocument7 pagesA Case Study in The Historical and Political Background of Barangay 77 Banez VillPogi MedinoNo ratings yet

- People V Lopez 232247Document7 pagesPeople V Lopez 232247Edwino Nudo Barbosa Jr.No ratings yet

- Separation of East Pakistan Javed Iqbal PDFDocument22 pagesSeparation of East Pakistan Javed Iqbal PDFsabaahat100% (2)

- City Vs PrietoDocument15 pagesCity Vs PrietoDindo Jr Najera BarcenasNo ratings yet