You might also like

- Banking Governance, Performance and Risk-Taking: Conventional Banks vs Islamic BanksFrom EverandBanking Governance, Performance and Risk-Taking: Conventional Banks vs Islamic BanksNo ratings yet

- Unit - 5 Banking Regulation and Central Bank Policy For Bank and Fis Meaning of RegulationDocument13 pagesUnit - 5 Banking Regulation and Central Bank Policy For Bank and Fis Meaning of Regulationsahil ShresthaNo ratings yet

- CENTRAL BANKING & MONETARY POLICY Short NoteDocument11 pagesCENTRAL BANKING & MONETARY POLICY Short NoteDipayan_luNo ratings yet

- Government'S Role in BankingDocument11 pagesGovernment'S Role in BankingDianePaguiaAngelesNo ratings yet

- CHAPTER 2 Bank RegulationDocument55 pagesCHAPTER 2 Bank RegulationBaby Khor0% (1)

- Lexicon in The Phil BankingDocument13 pagesLexicon in The Phil BankingSuzethNo ratings yet

- Operations ManagemnetDocument6 pagesOperations ManagemnetMuhammad Zerak JahanNo ratings yet

- Reserve Bank of IndiaDocument25 pagesReserve Bank of IndiaUdayan SamirNo ratings yet

- Non Banking Financial InstitutionsDocument10 pagesNon Banking Financial InstitutionsJyothi SoniNo ratings yet

- Bank RegulationDocument6 pagesBank RegulationAndre WestNo ratings yet

- Essay RichardoDocument19 pagesEssay RichardoRichardo WilliamsNo ratings yet

- 2.1.1 The Concepts of Central BankingDocument9 pages2.1.1 The Concepts of Central Bankingjoel minaniNo ratings yet

- Central Bank As RegulatorDocument20 pagesCentral Bank As Regulatoroptimist4uNo ratings yet

- Gill Marcus: Issues For Consideration in Mergers and Takeovers From A Regulatory PerspectiveDocument12 pagesGill Marcus: Issues For Consideration in Mergers and Takeovers From A Regulatory PerspectiveTushar AhujaNo ratings yet

- BANKING INDUSTRY REGULATIONDocument23 pagesBANKING INDUSTRY REGULATIONPia De LaraNo ratings yet

- Interview DataDocument8 pagesInterview DataFaisi GikianNo ratings yet

- Liquidity Management and Commercial Banks' Profitability in NigeriaDocument16 pagesLiquidity Management and Commercial Banks' Profitability in NigeriaPrince KumarNo ratings yet

- Analysis of Banking Regulation in Hong KongDocument7 pagesAnalysis of Banking Regulation in Hong KongLeung Shing HeiNo ratings yet

- ASSET LIABILITIES Mnagament in BanksDocument25 pagesASSET LIABILITIES Mnagament in Bankspriyank shah100% (6)

- Undercover EconomistDocument14 pagesUndercover EconomistAreeba AfridiNo ratings yet

- Systematical Importance of BanksDocument5 pagesSystematical Importance of Banksandrejasprovski16No ratings yet

- UNEC TheoryofbankingDocument24 pagesUNEC TheoryofbankingTaKo TaKoNo ratings yet

- Gamay Kag ItlogDocument11 pagesGamay Kag ItlogAlfie OmegaNo ratings yet

- Capital Adequacy: Credit ExposureDocument10 pagesCapital Adequacy: Credit ExposureHimani DhingraNo ratings yet

- A222 BWBB3193 Topic 02 RegulationDocument48 pagesA222 BWBB3193 Topic 02 RegulationNurFazalina AkbarNo ratings yet

- Overview of Financial System: Prof. Mishu Tripathi Asst. Professor-FinanceDocument16 pagesOverview of Financial System: Prof. Mishu Tripathi Asst. Professor-FinanceAashutosh SinghNo ratings yet

- Central Banking Functions & EvolutionDocument112 pagesCentral Banking Functions & EvolutionSK Mishra100% (2)

- Bank Regulations and SupervisionDocument6 pagesBank Regulations and SupervisionYashna BeeharryNo ratings yet

- Bank Regulation: A Presentation byDocument16 pagesBank Regulation: A Presentation byabdalla osmanNo ratings yet

- Bank Regulations and Compliance SummaryDocument46 pagesBank Regulations and Compliance Summarysabrina hanifNo ratings yet

- Commercial Bank Investment Banks UnderwriteDocument12 pagesCommercial Bank Investment Banks UnderwriteDana MunteanNo ratings yet

- Commercial Banks: Role and Importance in IndiaDocument134 pagesCommercial Banks: Role and Importance in Indiaanjali jainNo ratings yet

- Role of Central Banks and Credit CreationDocument44 pagesRole of Central Banks and Credit Creationdua tanveerNo ratings yet

- Central Bank Functions and Challenges in BangladeshDocument3 pagesCentral Bank Functions and Challenges in BangladeshAyesha SiddikaNo ratings yet

- Id 07Document3 pagesId 07Ayesha SiddikaNo ratings yet

- L 012 - Banking SystemDocument5 pagesL 012 - Banking SystemFelix OkinyiNo ratings yet

- How Banks Function and Their Role in the EconomyDocument12 pagesHow Banks Function and Their Role in the EconomySonam JainNo ratings yet

- Functions of Central BankDocument4 pagesFunctions of Central BankK8suser JNo ratings yet

- Regulatory Framework QuestionsDocument10 pagesRegulatory Framework QuestionsAndreaNo ratings yet

- Government Regulation Banks: Bank Regulations and Functions Are A Form ofDocument1 pageGovernment Regulation Banks: Bank Regulations and Functions Are A Form ofsarangpandey05No ratings yet

- Chapter 2Document48 pagesChapter 2Muhaizam MusaNo ratings yet

- Banking Law Project FINALDocument28 pagesBanking Law Project FINALibrar aliNo ratings yet

- Unit 5 - Central BankDocument21 pagesUnit 5 - Central Banktempacc9322No ratings yet

- Bwbb2013 Topic 2Document22 pagesBwbb2013 Topic 2myteacheroht.managementNo ratings yet

- Group 1Document12 pagesGroup 1eranyigiNo ratings yet

- CB-05 Functions and Operations of BSPDocument5 pagesCB-05 Functions and Operations of BSPJHERRY MIG SEVILLA100% (1)

- Lecture Note on BankingDocument68 pagesLecture Note on Bankinggeta beleteNo ratings yet

- Law and Practice of Banking Assignment - 1Document4 pagesLaw and Practice of Banking Assignment - 1SALIM SHARIFUNo ratings yet

- Banking RegulationsDocument5 pagesBanking RegulationsManuella RyanNo ratings yet

- Financial Markets and Resource MobilizationDocument13 pagesFinancial Markets and Resource MobilizationFred Raphael Ilomo100% (3)

- Bank Regulation and Supervision: Key Concepts and FrameworkDocument36 pagesBank Regulation and Supervision: Key Concepts and FrameworkAsniNo ratings yet

- Capita Adequacy of Himalayan BankDocument23 pagesCapita Adequacy of Himalayan BankArjunNo ratings yet

- Corporate Governance Critical for Bank StabilityDocument12 pagesCorporate Governance Critical for Bank StabilityPritismasatyalNo ratings yet

- Governance 29 May 06 PDFDocument10 pagesGovernance 29 May 06 PDFrehanNo ratings yet

- Government Regulation Banks: Bank Regulations Are A Form ofDocument1 pageGovernment Regulation Banks: Bank Regulations Are A Form ofsarangpandey05No ratings yet

- Business Finance: I. Regulators of Financial MarketsDocument6 pagesBusiness Finance: I. Regulators of Financial Marketscristine aguilarNo ratings yet

- The Top Four Techniques of Credit Control Adopt by Central Bank. The Technique Are: 1. The Bank Rate 2. Open Market OperationsDocument4 pagesThe Top Four Techniques of Credit Control Adopt by Central Bank. The Technique Are: 1. The Bank Rate 2. Open Market OperationsAbdul WahabNo ratings yet

- Liquidity Management of Citi BankDocument8 pagesLiquidity Management of Citi BankGanesh AppNo ratings yet

- Term PaperDocument8 pagesTerm PaperKetema AsfawNo ratings yet

- Guidelines & Norms For Basel Committee For Bank SupervisionDocument5 pagesGuidelines & Norms For Basel Committee For Bank SupervisionkinNo ratings yet

- PW-DEPARTMENT CODES GUIDELINESDocument19 pagesPW-DEPARTMENT CODES GUIDELINESanilNo ratings yet

- Raoul Pal GMI July2015 MonthlyDocument61 pagesRaoul Pal GMI July2015 MonthlyZerohedge100% (4)

- Manacle and Coin (Oef)Document130 pagesManacle and Coin (Oef)goflux pwns50% (2)

- Cash FLowDocument60 pagesCash FLowSakshi SharmaNo ratings yet

- 1 What Are The Differences Between A Direct Subsidized LoanDocument2 pages1 What Are The Differences Between A Direct Subsidized LoanAmit PandeyNo ratings yet

- Commercial Law SyllabusDocument163 pagesCommercial Law SyllabusJms SapNo ratings yet

- Group 4 - PARITY CONDITIONS IN INTERNATIONAL FINANCE AND CURRENCY FORECASTINGDocument37 pagesGroup 4 - PARITY CONDITIONS IN INTERNATIONAL FINANCE AND CURRENCY FORECASTINGadindaNo ratings yet

- Summer Internship Report (Sanket Yadav) PDFDocument54 pagesSummer Internship Report (Sanket Yadav) PDFtejasNo ratings yet

- Set of CceDocument1 pageSet of CceC/PVT DAET, SHAINA JOYNo ratings yet

- 21 FAR460 SS SET 1 Dec21 Kel - StudentDocument9 pages21 FAR460 SS SET 1 Dec21 Kel - StudentRuzaikha razaliNo ratings yet

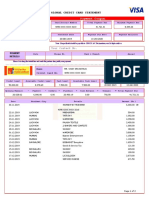

- Credit Card Statement Dated 20122019 PDFDocument3 pagesCredit Card Statement Dated 20122019 PDFvivek srivastavaNo ratings yet

- Adjusting Entries Depreciation MethodDocument11 pagesAdjusting Entries Depreciation MethodClarissa Rivera VillalobosNo ratings yet

- Personal Earnings Annuity Scheme (PEAS)Document14 pagesPersonal Earnings Annuity Scheme (PEAS)DafideeNo ratings yet

- UBL UK Application Form FinalDocument6 pagesUBL UK Application Form Finalfaisal_ahsan7919No ratings yet

- Central Government Act: The Foreign Exchange Regulation Act, 1973Document50 pagesCentral Government Act: The Foreign Exchange Regulation Act, 1973Nilesh MandlikNo ratings yet

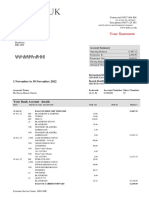

- Cheque account statement summaryDocument6 pagesCheque account statement summaryMarkNo ratings yet

- R12 - Bank Account Transfer Ver 1.0Document644 pagesR12 - Bank Account Transfer Ver 1.0phanisure100% (5)

- 89598085594Document3 pages89598085594Adrian GonzalezNo ratings yet

- The New Government Accounting System ManualDocument35 pagesThe New Government Accounting System ManualelminvaldezNo ratings yet

- B V M Engineering College Vallabh VidyanagarDocument9 pagesB V M Engineering College Vallabh VidyanagarShish DattaNo ratings yet

- Course Notes MGT338 - Class 5Document3 pagesCourse Notes MGT338 - Class 5Luciene20No ratings yet

- Tugas P17-8 - AKLDocument15 pagesTugas P17-8 - AKLNovie AriyantiNo ratings yet

- Non Current LiabilitiesDocument7 pagesNon Current LiabilitiesRomano CruzNo ratings yet

- Functions of Financial Systems and Markets LessonDocument10 pagesFunctions of Financial Systems and Markets LessonMark Angelo BustosNo ratings yet

- Canara BankDocument8 pagesCanara BankKrithika SalrajNo ratings yet

- 2022 11 30 - StatementDocument7 pages2022 11 30 - StatementGiovanni SlackNo ratings yet

- Finladder Financial Modeling Course and InternshipDocument1 pageFinladder Financial Modeling Course and Internshipbadar10131No ratings yet

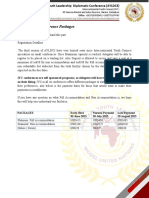

- AYLDC3 Packages and Payment InstructionDocument5 pagesAYLDC3 Packages and Payment InstructionAbu Bakarr ContehNo ratings yet

- Key Takeaways on Top Cryptocurrencies Beyond BitcoinDocument4 pagesKey Takeaways on Top Cryptocurrencies Beyond BitcoinJonhmark AniñonNo ratings yet

- BVMF Presentation - July 2014Document51 pagesBVMF Presentation - July 2014BVMF_RINo ratings yet