You might also like

- Debt for Sale: A Social History of the Credit TrapFrom EverandDebt for Sale: A Social History of the Credit TrapRating: 4.5 out of 5 stars4.5/5 (3)

- Facilitate: OriginsDocument8 pagesFacilitate: OriginsZara BhayoNo ratings yet

- The Great Recession: The burst of the property bubble and the excesses of speculationFrom EverandThe Great Recession: The burst of the property bubble and the excesses of speculationNo ratings yet

- Case Study 1 - What Was The Financial Crisis of 2007-2008Document4 pagesCase Study 1 - What Was The Financial Crisis of 2007-2008Anh NguyenNo ratings yet

- How Did MortgageDocument5 pagesHow Did MortgageUlisesNo ratings yet

- 2008 CrisisDocument3 pages2008 CrisismoshiNo ratings yet

- The Financial Crisis of 2008Document10 pagesThe Financial Crisis of 2008Lede Ann Calipus Yap100% (1)

- The House of CardsDocument42 pagesThe House of Cardsramesm38No ratings yet

- The Financial Crisis of 2008Document8 pagesThe Financial Crisis of 2008Mary June Tive VasquezNo ratings yet

- Michael Burry and Mark BaumDocument13 pagesMichael Burry and Mark BaumMario Nakhleh0% (1)

- Case Study On Subprime CrisisDocument24 pagesCase Study On Subprime CrisisNakul SainiNo ratings yet

- Washington MutualDocument20 pagesWashington Mutualyud4No ratings yet

- US Subprime MortgageDocument9 pagesUS Subprime MortgageN MNo ratings yet

- Future of SecuritizationDocument6 pagesFuture of SecuritizationPulak SinhaNo ratings yet

- 2007-2008 Housing CrashDocument5 pages2007-2008 Housing CrashKanishk R.SinghNo ratings yet

- Q: - "Why Is British Banking in Crisis?" Provide Reasons and Suggest Possible Solutions?Document6 pagesQ: - "Why Is British Banking in Crisis?" Provide Reasons and Suggest Possible Solutions?scorpio786No ratings yet

- The Financial Crisis of 2008Document9 pagesThe Financial Crisis of 2008SerenajlyNo ratings yet

- The Financial Crisis of 2008Document2 pagesThe Financial Crisis of 2008Soufiane ZibouhNo ratings yet

- Crisis FinancieraDocument4 pagesCrisis Financierahawk91No ratings yet

- Financial Instruments Responsible For Global Financial CrisisDocument15 pagesFinancial Instruments Responsible For Global Financial Crisisabhishek gupte100% (4)

- The Financial Crisis of 2008: What Happened in Simple TermsDocument2 pagesThe Financial Crisis of 2008: What Happened in Simple TermsBig ALNo ratings yet

- 63 - Ankita Baburao Nighut-FDRM-Case Study 1Document4 pages63 - Ankita Baburao Nighut-FDRM-Case Study 1Ankita NighutNo ratings yet

- Course File 3-AssessmentDocument5 pagesCourse File 3-AssessmentLilibeth OrongNo ratings yet

- Case AnalysisDocument6 pagesCase AnalysisFranzing LebsNo ratings yet

- The 2008 Financial CrisisDocument4 pagesThe 2008 Financial CrisisLede Ann Calipus YapNo ratings yet

- US Sub-Prime Mortgage CrisisDocument6 pagesUS Sub-Prime Mortgage CrisisKumar GoutamNo ratings yet

- Which Were Backed Merely by Derivatives and Credit Default SwapsDocument3 pagesWhich Were Backed Merely by Derivatives and Credit Default SwapsPatrick HookNo ratings yet

- Global Financial CrisisDocument16 pagesGlobal Financial Crisisshreya pooniaNo ratings yet

- NINJA Loans To Blame For Financial CrisisDocument25 pagesNINJA Loans To Blame For Financial Crisischapy86No ratings yet

- K204040222 - Phạm Trần Cẩm Vi 4Document4 pagesK204040222 - Phạm Trần Cẩm Vi 4Nam Đỗ PhươngNo ratings yet

- Economics PresentationsDocument2 pagesEconomics PresentationsMunny Akter KhanNo ratings yet

- Ellen Brown 24032023Document7 pagesEllen Brown 24032023Thuan TrinhNo ratings yet

- Subprime Crisis FeiDocument13 pagesSubprime Crisis FeiDavuluri SasiNo ratings yet

- Ibt Movie ReviewDocument7 pagesIbt Movie ReviewNorolhaya Usman100% (1)

- Financial Service: Project On: Economic MeltdownDocument40 pagesFinancial Service: Project On: Economic MeltdownJas777No ratings yet

- Fall of Lehman BrothersDocument3 pagesFall of Lehman BrothersFrFlordianNo ratings yet

- What Is A Subprime Mortgage?Document5 pagesWhat Is A Subprime Mortgage?Chigo RamosNo ratings yet

- WamuDocument8 pagesWamuSylvia KharatNo ratings yet

- Financial Crisis of 2007Document6 pagesFinancial Crisis of 2007absolutelyarpitaNo ratings yet

- Bank of America CorpDocument7 pagesBank of America Corpbcm85No ratings yet

- The Subprime Mortgage CrisisDocument38 pagesThe Subprime Mortgage Crisiseric3215No ratings yet

- Another Financial Meltdown Is Closer Than It Appears.: Source: FREDDocument14 pagesAnother Financial Meltdown Is Closer Than It Appears.: Source: FREDVidit HarsulkarNo ratings yet

- The Role of CDOs in Subprime CrisisDocument6 pagesThe Role of CDOs in Subprime CrisisKunal BhodiaNo ratings yet

- Name: Syed Sikander Hussain Shah Course: Eco 607 Topic: Mortgage Crisis STUDENT ID: 024003260Document7 pagesName: Syed Sikander Hussain Shah Course: Eco 607 Topic: Mortgage Crisis STUDENT ID: 024003260Sam GitongaNo ratings yet

- The Credit Crisis ExplainedDocument4 pagesThe Credit Crisis ExplainedIPINGlobal100% (1)

- UssamaDocument12 pagesUssamaRizwan RizzuNo ratings yet

- Too Big To FailDocument9 pagesToo Big To FailPriyank Hariyani0% (1)

- 1 Leonhardt 2008 Cant Grasp The Credit CrisisDocument3 pages1 Leonhardt 2008 Cant Grasp The Credit Crisiscarmo-netoNo ratings yet

- Book Review (Roll 93, Batch 27)Document6 pagesBook Review (Roll 93, Batch 27)naziba aliNo ratings yet

- Chronicle of World Financial Crisis 2007-2008Document4 pagesChronicle of World Financial Crisis 2007-2008Md. Azim Ferdous100% (1)

- Mortgage Credit CrisisDocument5 pagesMortgage Credit Crisisasfand yar waliNo ratings yet

- The Stony Brook Press - Volume 30, Issue 10Document32 pagesThe Stony Brook Press - Volume 30, Issue 10The Stony Brook PressNo ratings yet

- The Financial Crisis of 2007-08Document23 pagesThe Financial Crisis of 2007-08SabinaNo ratings yet

- The Anatomy of A Crisis: Speculative BubbleDocument3 pagesThe Anatomy of A Crisis: Speculative BubbleVbiidbdiaan ExistimeNo ratings yet

- 2008 Credit CrisisDocument14 pages2008 Credit CrisisSharmila JoshiNo ratings yet

- U.S. Subprime Mortgage Crisis (A & B)Document8 pagesU.S. Subprime Mortgage Crisis (A & B)prabhat kumarNo ratings yet

- Economic Crisis Matttick JRDocument31 pagesEconomic Crisis Matttick JRAnonymous mOdaetXf7iNo ratings yet

- Anul III Trad Business English Part III 15 Noiembrie 2014Document6 pagesAnul III Trad Business English Part III 15 Noiembrie 2014Ana-Maria Dumitroiu0% (1)

- CitibankDocument5 pagesCitibankPooja GuptaNo ratings yet

- The Panic of 1907 - Federal Reserve HistoryDocument6 pagesThe Panic of 1907 - Federal Reserve HistoryThomas WilliamsNo ratings yet

- De Guzman, Daniella Jae - Uratex Strategic PlanDocument18 pagesDe Guzman, Daniella Jae - Uratex Strategic Plandaniella jae de guzmanNo ratings yet

- Strategic Leadership Rodgie FloresDocument11 pagesStrategic Leadership Rodgie Floresdaniella jae de guzmanNo ratings yet

- Strategic LeadershipDocument16 pagesStrategic Leadershipdaniella jae de guzmanNo ratings yet

- Market PowerDocument19 pagesMarket Powerdaniella jae de guzmanNo ratings yet

- Benitez, Allan Christian C. Doctrine: Bill of Exchange (Definition & Concept)Document5 pagesBenitez, Allan Christian C. Doctrine: Bill of Exchange (Definition & Concept)Arrianne ObiasNo ratings yet

- Enquiry Regarding Token Numbers of Outstanding Pre-Check BillsDocument3 pagesEnquiry Regarding Token Numbers of Outstanding Pre-Check BillsARAVIND K100% (1)

- Ibs JLN Gombak, KL 1 31/05/20Document3 pagesIbs JLN Gombak, KL 1 31/05/20Nada NadhirahNo ratings yet

- AR0708 Co Oprative BanksDocument68 pagesAR0708 Co Oprative BanksNaveenNo ratings yet

- Bank CommandsDocument7 pagesBank CommandsShubham CharanNo ratings yet

- Cendana - CITYZEN HILLS - 291123-1Document5 pagesCendana - CITYZEN HILLS - 291123-1Oky Arnol SunjayaNo ratings yet

- Abhisarika Sex Education Magazine Nov 2015Document40 pagesAbhisarika Sex Education Magazine Nov 2015Dr. DVR Poosha100% (4)

- Model Question Paper AsstDirector Co Op AuditDocument12 pagesModel Question Paper AsstDirector Co Op AuditChandan NNo ratings yet

- What Is Borrowing MoneyDocument5 pagesWhat Is Borrowing MoneyMiNh sóiNo ratings yet

- Tutorial Hedge Fund WEEK 12 With SolutionsDocument13 pagesTutorial Hedge Fund WEEK 12 With SolutionsYaonik HimmatramkaNo ratings yet

- Time Value of Money: Marios MavridesDocument35 pagesTime Value of Money: Marios Mavridesandreas panayiotouNo ratings yet

- Instructions / Checklist For Filling KYC FormDocument18 pagesInstructions / Checklist For Filling KYC Formbaishali royNo ratings yet

- CASE STUDY ON Mergers & AcquisitionDocument32 pagesCASE STUDY ON Mergers & AcquisitionPrernaNo ratings yet

- The-Balance-Of-Payments AUSDocument6 pagesThe-Balance-Of-Payments AUSrahul ingleNo ratings yet

- Upay - ProjectDocument19 pagesUpay - ProjectDevillz Advocate0% (2)

- Tax Invoice / Statement of Account: Invoice Cukai / Penyata AkaunDocument4 pagesTax Invoice / Statement of Account: Invoice Cukai / Penyata AkaunMuhammad NaqibNo ratings yet

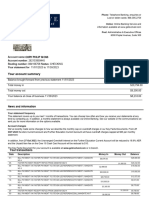

- Wells Fargo Business Bank Statement PDFDocument4 pagesWells Fargo Business Bank Statement PDFquannbui9577% (13)

- Icici Mission and Vision Statement AnalysisDocument9 pagesIcici Mission and Vision Statement AnalysisJasmine SikariaNo ratings yet

- Fabm1 Quarter3 Module 8 Week 8 Week 9Document19 pagesFabm1 Quarter3 Module 8 Week 8 Week 9Princess Nicole EsioNo ratings yet

- A Study On A Financial Performance Analysis of Private Banks in IndiaDocument26 pagesA Study On A Financial Performance Analysis of Private Banks in Indiashrisha sharma100% (1)

- Why Did Lakshmi Walk Away From LVB - 2020Document1 pageWhy Did Lakshmi Walk Away From LVB - 2020Sriram RanganathanNo ratings yet

- India Is Becoming The Fintech Hub of The WorldDocument49 pagesIndia Is Becoming The Fintech Hub of The WorldGanesh BhandaryNo ratings yet

- Firestone v. CADocument2 pagesFirestone v. CAYodh Jamin OngNo ratings yet

- Notes Business Studies Lesson 4 XI ComDocument4 pagesNotes Business Studies Lesson 4 XI Comadarshchoudhary2796No ratings yet

- Oct Evolve and TrustDocument2 pagesOct Evolve and TrustSafeBit ProsNo ratings yet

- Welcome To IBPS CWEDocument1 pageWelcome To IBPS CWERamu AlladiNo ratings yet

- Power of Attorney (Poa) in Favour of Iifl Securities LimitedDocument4 pagesPower of Attorney (Poa) in Favour of Iifl Securities LimitedGANESH JAINNo ratings yet

- BRM Cce-2Document8 pagesBRM Cce-2Akshat PandeNo ratings yet

- SLHT Business Finance WEEK 910Document7 pagesSLHT Business Finance WEEK 910Ian OcheaNo ratings yet

- English Forum SwitzerlandDocument3 pagesEnglish Forum SwitzerlandMarlene BritoNo ratings yet