You might also like

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)From EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Rating: 3.5 out of 5 stars3.5/5 (17)

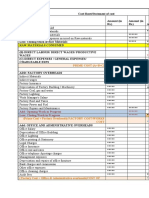

- Cost sheet format breakdownDocument2 pagesCost sheet format breakdownabhijeetNo ratings yet

- Handout 1 - Cost & Management Accounting - Feb 17, 2019 - 3pm To 6pmDocument3 pagesHandout 1 - Cost & Management Accounting - Feb 17, 2019 - 3pm To 6pmBhunesh KumarNo ratings yet

- Manufacturing Cost ClassificationDocument61 pagesManufacturing Cost Classificationdamayogesh4No ratings yet

- Cost Accounting Notes by Rehan FarhatDocument38 pagesCost Accounting Notes by Rehan FarhatImran SaeeNo ratings yet

- Cost Accounting - Classifying Manufacturing CostsDocument3 pagesCost Accounting - Classifying Manufacturing CostsAdil ArshadNo ratings yet

- Cost Sheet Basics and FormatDocument33 pagesCost Sheet Basics and FormatShubham Saurav SSNo ratings yet

- Costing FormulaDocument76 pagesCosting FormulaRamyapapu100% (5)

- Costing Formulas NewDocument62 pagesCosting Formulas Newvenky_1986100% (6)

- Costing Formulae Topic WiseDocument81 pagesCosting Formulae Topic Wiseamit kathaitNo ratings yet

- Cost Sheet: Practical Problems 05-08-20Document14 pagesCost Sheet: Practical Problems 05-08-20Shubham Saurav SSNo ratings yet

- For CS Students-Costing FormulasDocument85 pagesFor CS Students-Costing FormulasSubhash Sahu100% (12)

- Prime Cost (A+B+C) : Add: Opening Work in Progress Less: Closing Work in ProgressDocument6 pagesPrime Cost (A+B+C) : Add: Opening Work in Progress Less: Closing Work in ProgressHarish PahadiyaNo ratings yet

- Chapter 1: Cost Sheet: Rohit AgarwalDocument4 pagesChapter 1: Cost Sheet: Rohit Agarwalbcom100% (1)

- Cost SheetDocument10 pagesCost SheetAmanNo ratings yet

- Costing Formulae Topic WiseDocument83 pagesCosting Formulae Topic WiseViswanathan SrkNo ratings yet

- 3 Cost Centre, Classification and Cost SheetDocument5 pages3 Cost Centre, Classification and Cost SheetJAY PRAKASH HINDOCHA-BBANo ratings yet

- Statement of Cash Flow (Indirect Method) : Cash Flows From Investing ActivitiesDocument25 pagesStatement of Cash Flow (Indirect Method) : Cash Flows From Investing ActivitiesnislamdollerNo ratings yet

- Classification of CostsDocument84 pagesClassification of CostsRoyal ProjectsNo ratings yet

- b85946fc 1608023673050Document23 pagesb85946fc 1608023673050RobinsNo ratings yet

- Cost Sheet - Job - Batch - Contract Work Sheet - 08-04-2023Document9 pagesCost Sheet - Job - Batch - Contract Work Sheet - 08-04-2023JAYARAJALAKSHMI IlangoNo ratings yet

- Cost sheet format breakdown expensesDocument2 pagesCost sheet format breakdown expensesRoshni MoryeNo ratings yet

- How to prepare a cost sheet to analyze production costsDocument23 pagesHow to prepare a cost sheet to analyze production costsShubham Saurav SSNo ratings yet

- L3-L4 CostsheetDocument30 pagesL3-L4 CostsheetDhawal RajNo ratings yet

- Cost Sheet: Basics and Format 040820Document18 pagesCost Sheet: Basics and Format 040820Shubham Saurav SSNo ratings yet

- Cost SheetDocument14 pagesCost SheetNirmal SinghNo ratings yet

- Cost Terms, Concepts and ClassificationDocument12 pagesCost Terms, Concepts and Classificationu1909030No ratings yet

- Manufacturing Accounts: Igcse - 2020 - Accounting (9-1) - Mahdi SamdaniDocument4 pagesManufacturing Accounts: Igcse - 2020 - Accounting (9-1) - Mahdi SamdaniNasif KhanNo ratings yet

- Practice Material On Cost of Goods Manufectured and Sold Statement. MGT402Document34 pagesPractice Material On Cost of Goods Manufectured and Sold Statement. MGT402Syed Ali HaiderNo ratings yet

- Marginal Cost Analysis of Britannia: Presented By: Shraddha Bhatt (A024) Jincey Jose (A009) Richa Tupsakhare (A022)Document29 pagesMarginal Cost Analysis of Britannia: Presented By: Shraddha Bhatt (A024) Jincey Jose (A009) Richa Tupsakhare (A022)Sriram MNo ratings yet

- Format 4 Cost AccountingDocument4 pagesFormat 4 Cost AccountingRahul PurshottamNo ratings yet

- Explain The Procedure of Reconciliation of Financial and Cost Accounting DataDocument6 pagesExplain The Procedure of Reconciliation of Financial and Cost Accounting DataKritika JainNo ratings yet

- Cost Sheet AnalysisDocument4 pagesCost Sheet Analysiskhushboo rajputNo ratings yet

- Costing Formulae Topic WiseDocument81 pagesCosting Formulae Topic WiseSuresh SharmaNo ratings yet

- CA ClubIndia 35 Cost AccountingDocument17 pagesCA ClubIndia 35 Cost AccountingAshwin S ChettiarNo ratings yet

- Chargeable ExpensesDocument33 pagesChargeable ExpensesMahmud MugdhoNo ratings yet

- Cost StatementDocument1 pageCost StatementTahsinul Haque TasifNo ratings yet

- Course Title: Cost Accounting Course Code:441 BBA Program Lecture-2Document14 pagesCourse Title: Cost Accounting Course Code:441 BBA Program Lecture-2Tanvir Ahmed ChowdhuryNo ratings yet

- 1 Introduction To Cost Accounting (2017)Document62 pages1 Introduction To Cost Accounting (2017)kilogek124No ratings yet

- Cost and Management Accounting and Quandative TechniqueDocument86 pagesCost and Management Accounting and Quandative TechniquesaiyuvatechNo ratings yet

- Cost Sheet AnalysisDocument23 pagesCost Sheet AnalysisBalkrushna Shingare33% (3)

- New Microsoft Word Document (4)Document3 pagesNew Microsoft Word Document (4)Santosh PatelNo ratings yet

- Cost FormulasDocument26 pagesCost FormulasshivaswapnaNo ratings yet

- Direct Materials Add: Direct Labour Add: Direct ExpensesDocument5 pagesDirect Materials Add: Direct Labour Add: Direct Expensesavinal malikNo ratings yet

- Bba Project 3.0Document8 pagesBba Project 3.0Mr UniqueNo ratings yet

- Module 4Document12 pagesModule 4aishwaryaNo ratings yet

- Project ReportDocument34 pagesProject ReportSaicharan UppalapattiNo ratings yet

- Generate Salary Certificate TitleDocument1 pageGenerate Salary Certificate TitleSaicharan UppalapattiNo ratings yet

- PayslipDocument2 pagesPayslipSaicharan UppalapattiNo ratings yet

- PayslipDocument2 pagesPayslipSaicharan UppalapattiNo ratings yet

- PayslipDocument2 pagesPayslipSaicharan UppalapattiNo ratings yet

- Important Links Login Id and Password RM Details For PLDocument3 pagesImportant Links Login Id and Password RM Details For PLSaicharan UppalapattiNo ratings yet

- Agreement Flat No.301 Phani PlazaDocument4 pagesAgreement Flat No.301 Phani PlazaSaicharan UppalapattiNo ratings yet

- HDB Relieving Letter-1Document1 pageHDB Relieving Letter-1Saicharan UppalapattiNo ratings yet

- Certificate of DepartureDocument1 pageCertificate of DepartureSaicharan UppalapattiNo ratings yet

- Be Sem VDocument1 pageBe Sem VSaicharan UppalapattiNo ratings yet

- Exxon Mobil CorpDocument1 pageExxon Mobil Corpgarikai masawiNo ratings yet

- In The High Court of Justice Business and Property Courts of England and Wales Business List (CH D)Document190 pagesIn The High Court of Justice Business and Property Courts of England and Wales Business List (CH D)Legal CheekNo ratings yet

- Moodys Approach To Rating The Petroleum Industry PDFDocument32 pagesMoodys Approach To Rating The Petroleum Industry PDFMujtabaNo ratings yet

- CONFRASDocument68 pagesCONFRASLorraine Mae RobridoNo ratings yet

- Chapter 4Document103 pagesChapter 4JeanetteMcduffieNo ratings yet

- Benchmark KPI (On Desk)Document4 pagesBenchmark KPI (On Desk)indah7575No ratings yet

- Zero-Coupon Yield Curve ExerciseDocument22 pagesZero-Coupon Yield Curve ExercisePham Minh DucNo ratings yet

- 6Document9 pages6abadi gebru100% (1)

- Street Prostitute Like Department Store SantaDocument32 pagesStreet Prostitute Like Department Store SantaAlena Bondarenko100% (2)

- Deptals 2Document6 pagesDeptals 2jenylyn acostaNo ratings yet

- ACCO 20213 Fundamentals of AccountingDocument3 pagesACCO 20213 Fundamentals of AccountingPatrick John AvilaNo ratings yet

- ADZUCL Incomesyllabus SY2014 15Document72 pagesADZUCL Incomesyllabus SY2014 15Benn DegusmanNo ratings yet

- ACCT 2500 Test 2 Format, Instructions and ReviewDocument17 pagesACCT 2500 Test 2 Format, Instructions and Reviewyahye ahmedNo ratings yet

- A-Level Economics/AQA/Markets and Market FailureDocument35 pagesA-Level Economics/AQA/Markets and Market FailureMatthew Harris100% (1)

- CHAPTER 4 Caselette Audit of Receivables PDFDocument32 pagesCHAPTER 4 Caselette Audit of Receivables PDFDaniela BombezaNo ratings yet

- Oman Foreign Capital Investment LawDocument8 pagesOman Foreign Capital Investment LawShishir Kumar SinghNo ratings yet

- Audit Chapter on Inventory and Fixed AssetsDocument41 pagesAudit Chapter on Inventory and Fixed AssetsAbbie Sajonia DollenoNo ratings yet

- Yulo Vs YangDocument2 pagesYulo Vs YangGil Ray Vergara OntalNo ratings yet

- 04 Marginal CostingDocument67 pages04 Marginal CostingAyushNo ratings yet

- Principles of Macroeconomics 10th Edition Solution ManualDocument43 pagesPrinciples of Macroeconomics 10th Edition Solution ManualAhmed GhanimNo ratings yet

- Brief Notes On CVP Analysis and Short Term Decision Making: Hanish RajpalDocument5 pagesBrief Notes On CVP Analysis and Short Term Decision Making: Hanish RajpalRaunak_Gattani_4769No ratings yet

- PayrollDocument2 pagesPayrollAlanlovely Arazaampong Amos73% (11)

- Edited AC2104 BibleDocument166 pagesEdited AC2104 BibleStreak CalmNo ratings yet

- Project Report FOR 1000 MT Cold Storage: Details of Project Cost and Means of FinanceDocument11 pagesProject Report FOR 1000 MT Cold Storage: Details of Project Cost and Means of FinancePraveenKDNo ratings yet

- Flicker Fade Gone by Carljoe JavierDocument5 pagesFlicker Fade Gone by Carljoe JavierJohn AlbertNo ratings yet

- BA13 AssignmentDocument2 pagesBA13 AssignmentKatrina youngNo ratings yet

- ActDocument2 pagesActJeffrey Garcia IlaganNo ratings yet

- Hawai ChappalsDocument3 pagesHawai ChappalsvambuNo ratings yet

- Alternative Revenues Raising Mechanism - City of Dasmarinas, CaviteDocument15 pagesAlternative Revenues Raising Mechanism - City of Dasmarinas, CaviteOman Paul AntiojoNo ratings yet

- W 8ben TdaDocument1 pageW 8ben TdaAnamaria Suciu100% (1)