You might also like

- Cash Flow Estimation and Risk AnalysisDocument42 pagesCash Flow Estimation and Risk AnalysisdaidainaNo ratings yet

- Initial Year Net Cash FlowDocument4 pagesInitial Year Net Cash FlowWawex DavisNo ratings yet

- CH #12Document5 pagesCH #12BWB DONALDNo ratings yet

- Corporate Finance Canadian 7th Edition Jaffe Solutions ManualDocument16 pagesCorporate Finance Canadian 7th Edition Jaffe Solutions Manualtaylorhughesrfnaebgxyk100% (25)

- CH 12 Cash Flow Estimatision and Risk AnalysisDocument39 pagesCH 12 Cash Flow Estimatision and Risk AnalysisRidhoVerianNo ratings yet

- Brealey 5CE Ch09 SolutionsDocument27 pagesBrealey 5CE Ch09 SolutionsToby Tobes TobezNo ratings yet

- Fundamentals of Corporate Finance Canadian 6th Edition Brealey Solutions ManualDocument26 pagesFundamentals of Corporate Finance Canadian 6th Edition Brealey Solutions Manualmisentrynotal6ip1lp100% (16)

- Cash Flow Estimation and Risk AnalysisDocument52 pagesCash Flow Estimation and Risk AnalysisAmmad Shahid MinhasNo ratings yet

- Final CaseDocument25 pagesFinal CaseSakshi SharmaNo ratings yet

- Case01 02Document24 pagesCase01 02Sakshi SharmaNo ratings yet

- Chapter 1Document18 pagesChapter 1Kenny WongNo ratings yet

- Engg. Economics ProjectDocument13 pagesEngg. Economics ProjectkawtharNo ratings yet

- Modern Pharma SolnDocument3 pagesModern Pharma SolnSakshiNo ratings yet

- Making Capital Investment DecisionsDocument48 pagesMaking Capital Investment DecisionsJerico ClarosNo ratings yet

- Normalization AdjustmentsDocument1 pageNormalization AdjustmentsAbraham ChinNo ratings yet

- PGDM CV DCF 20th August LectureDocument11 pagesPGDM CV DCF 20th August Lecturepratik waliwandekarNo ratings yet

- Training Business Case Day 2Document13 pagesTraining Business Case Day 2amritakiranaaNo ratings yet

- Fundamentals of Corporate Finance Canadian 6th Edition Brealey Solutions Manual 1Document36 pagesFundamentals of Corporate Finance Canadian 6th Edition Brealey Solutions Manual 1jillhernandezqortfpmndz100% (23)

- Determining Cash Flows for Investment AnalysisDocument19 pagesDetermining Cash Flows for Investment AnalysisJack mazeNo ratings yet

- 3.1 Class Revision - Upload With AnswersDocument10 pages3.1 Class Revision - Upload With AnswersAnne AnnaNo ratings yet

- 23 Nov 2018 Mixed Questions With Solutions PDFDocument9 pages23 Nov 2018 Mixed Questions With Solutions PDFLaston MilanziNo ratings yet

- Exercises - 4 (Solutions) Chapter 10, Practice QuestionsDocument7 pagesExercises - 4 (Solutions) Chapter 10, Practice QuestionsFoititika.netNo ratings yet

- Fin Model Class9 Merger Model Using DCF MethodologyDocument1 pageFin Model Class9 Merger Model Using DCF MethodologyGel viraNo ratings yet

- Nov 2019 Suggested AnsDocument27 pagesNov 2019 Suggested Ansinter g19No ratings yet

- (Financial Figures in 000) : ARR Calculation: Invest LimitedDocument15 pages(Financial Figures in 000) : ARR Calculation: Invest LimitedYenJangNo ratings yet

- Bora Assignment FinalDocument12 pagesBora Assignment FinalBora AslanNo ratings yet

- Inv Appraisal Example and TemplateDocument3 pagesInv Appraisal Example and Templatecons theNo ratings yet

- Part 3Document1 pagePart 3sanjay mouryaNo ratings yet

- Part 1. Worksheet For Chapter 11, Capital BudgetingDocument9 pagesPart 1. Worksheet For Chapter 11, Capital BudgetingIndrama PurbaNo ratings yet

- BOK ValuationDocument7 pagesBOK ValuationsuryagcNo ratings yet

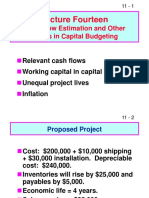

- Lecture Fourteen: Cash Flow Estimation and Other Topics in Capital BudgetingDocument38 pagesLecture Fourteen: Cash Flow Estimation and Other Topics in Capital BudgetingHồng KhánhNo ratings yet

- Solution Problem On Project EvaluationDocument5 pagesSolution Problem On Project EvaluationHasanNo ratings yet

- PLFM D22 Student Mark Plan PDFDocument12 pagesPLFM D22 Student Mark Plan PDFscottNo ratings yet

- Chapter 13 Capital Budgeting Estimating Cash Flow and Analyzing Risk Answers To End of Chapter Questions 13 3 Since The Cost of Capital Includes A Premium For Expected Inflation Failure 1Document8 pagesChapter 13 Capital Budgeting Estimating Cash Flow and Analyzing Risk Answers To End of Chapter Questions 13 3 Since The Cost of Capital Includes A Premium For Expected Inflation Failure 1ghzNo ratings yet

- FIN304 (End-Sem Model Answer 2021)Document9 pagesFIN304 (End-Sem Model Answer 2021)sha ve3No ratings yet

- Price EscalationDocument1 pagePrice EscalationsaptaraqsNo ratings yet

- Chapter 14 LEASINGDocument17 pagesChapter 14 LEASINGKaran KashyapNo ratings yet

- Answers Are Displayed in Red.: Assumptions and Other Problem Notes Are Displayed at The Very BottomDocument13 pagesAnswers Are Displayed in Red.: Assumptions and Other Problem Notes Are Displayed at The Very BottomShekar PalaniNo ratings yet

- Exercise 1:: 1,1 100 1,1 220 1,1 +46× 1,1 1 0,1×1,1 161,614 MilusdDocument4 pagesExercise 1:: 1,1 100 1,1 220 1,1 +46× 1,1 1 0,1×1,1 161,614 Milusdmai huongNo ratings yet

- NPV QuestionsDocument9 pagesNPV QuestionsSanjay MehrotraNo ratings yet

- (IE) Chapter 4 - Investment EfficiencyDocument88 pages(IE) Chapter 4 - Investment EfficiencyJane VickyNo ratings yet

- ACCT 328 - Assignment 2Document7 pagesACCT 328 - Assignment 2MalekNo ratings yet

- Midterm - Solutions 1) Theoretical QuestionsDocument4 pagesMidterm - Solutions 1) Theoretical QuestionsMarcos CachuloNo ratings yet

- Name: Course: SEGI Course Code: UCLAN Module Code: Registration Number Institution: Lecturer: Due Date: Student SignatureDocument8 pagesName: Course: SEGI Course Code: UCLAN Module Code: Registration Number Institution: Lecturer: Due Date: Student SignatureErick KinotiNo ratings yet

- Chapter 4 CB Problems - IDocument11 pagesChapter 4 CB Problems - IRoy YadavNo ratings yet

- Afm New Topic CompiledDocument59 pagesAfm New Topic Compiledganesh bhaiNo ratings yet

- CFI 2021 Fall Sem 5Document8 pagesCFI 2021 Fall Sem 5g87mjjj8rnNo ratings yet

- ITC Limited DCF Valuation and Intrinsic Value AnalysisDocument3 pagesITC Limited DCF Valuation and Intrinsic Value Analysissuraj nairNo ratings yet

- SMChap 006Document22 pagesSMChap 006Anonymous mKjaxpMaLNo ratings yet

- Financial Management Session 10Document20 pagesFinancial Management Session 10vaidehirajput03No ratings yet

- Chapter 13 Income Taxes GuideDocument17 pagesChapter 13 Income Taxes GuideKhilbran MuhammadNo ratings yet

- MC200912013 GSFM7514Document6 pagesMC200912013 GSFM7514Yaga KanggaNo ratings yet

- EconomicsDocument5 pagesEconomicsbrian mochez01No ratings yet

- Integrated CaseDocument31 pagesIntegrated Casechong chojun balsaNo ratings yet

- PGP25394 Keshav Sureka G CFDocument13 pagesPGP25394 Keshav Sureka G CFKeshavSurekaNo ratings yet

- FIN201 Comprehensive Final CaseDocument11 pagesFIN201 Comprehensive Final CaseRahmatullah AbirNo ratings yet

- FINA 3330 - Notes CH 9Document2 pagesFINA 3330 - Notes CH 9fische100% (1)

- Variable Costs R/tonneDocument3 pagesVariable Costs R/tonneChemEngGirl89No ratings yet

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- BMKT302 Ch1Document6 pagesBMKT302 Ch1Khalil KannaNo ratings yet

- Three Types of InnovationDocument1 pageThree Types of InnovationKhalil KannaNo ratings yet

- BFIN302 Ch1Document3 pagesBFIN302 Ch1Khalil KannaNo ratings yet

- Chapter Eleven Capital BudgetingDocument5 pagesChapter Eleven Capital BudgetingKhalil KannaNo ratings yet

- FM CH11 SummaryDocument3 pagesFM CH11 SummaryKhalil KannaNo ratings yet

- Microbiology - Prokaryotic Cell Biology: Bacterial Surface Structures Bacterial Cell Wall StructureDocument5 pagesMicrobiology - Prokaryotic Cell Biology: Bacterial Surface Structures Bacterial Cell Wall StructureDani AnyikaNo ratings yet

- Som-Ii Uqb 2019-20Document23 pagesSom-Ii Uqb 2019-20VENKATESH METHRINo ratings yet

- The 9 Building Blocks of Business ModelsDocument3 pagesThe 9 Building Blocks of Business ModelsTobeFrankNo ratings yet

- Omega 1 Akanksha 9069664Document5 pagesOmega 1 Akanksha 9069664Akanksha SarangiNo ratings yet

- MIT LL. Target Radar Cross Section (RCS)Document45 pagesMIT LL. Target Radar Cross Section (RCS)darin koblickNo ratings yet

- DGN ExamDocument5 pagesDGN ExamMaiga Ayub HusseinNo ratings yet

- Studies of Land Restoration On Spoil Heaps From Brown Coal MiningDocument11 pagesStudies of Land Restoration On Spoil Heaps From Brown Coal MiningeftychidisNo ratings yet

- E-Way BillDocument1 pageE-Way BillShriyans DaftariNo ratings yet

- The Brain from Inside Out Chapter 4 SummaryDocument20 pagesThe Brain from Inside Out Chapter 4 SummaryjuannnnNo ratings yet

- X-Plane Installer LogDocument3 pagesX-Plane Installer LogMarsala NistoNo ratings yet

- List of Trigonometric IdentitiesDocument16 pagesList of Trigonometric IdentitiesArnab NandiNo ratings yet

- Audit Chapter 7Document5 pagesAudit Chapter 7Addi Såïñt George100% (2)

- Strategic Management and Municipal Financial ReportingDocument38 pagesStrategic Management and Municipal Financial ReportingMarius BuysNo ratings yet

- Chen2019 PDFDocument5 pagesChen2019 PDFPriya VeerNo ratings yet

- K&J Quotation For Geotechnical - OLEODocument4 pagesK&J Quotation For Geotechnical - OLEORamakrishnaNo ratings yet

- Rate of ChangeDocument22 pagesRate of ChangeTrisha MariehNo ratings yet

- PEOPLE IN MY TOWN - Song Worksheet PAULA 2019Document2 pagesPEOPLE IN MY TOWN - Song Worksheet PAULA 2019PauNo ratings yet

- Teachers' Notes: ©film Education 1Document20 pagesTeachers' Notes: ©film Education 1רז ברקוNo ratings yet

- Lesson 2 - Procedures in Cleaning Utensils and EquipmentDocument26 pagesLesson 2 - Procedures in Cleaning Utensils and EquipmentReizel TulauanNo ratings yet

- Understanding Arthrogyposis Multiplex Congenita and Muscular DystrophiesDocument38 pagesUnderstanding Arthrogyposis Multiplex Congenita and Muscular DystrophiessmrutiptNo ratings yet

- Gen Z WhitepaperDocument13 pagesGen Z Whitepaperjurgute2000No ratings yet

- Customer Satisfaction in Maruti SuzukiDocument31 pagesCustomer Satisfaction in Maruti Suzukirajesh laddha100% (1)

- January 2011Document64 pagesJanuary 2011sake1978No ratings yet

- Gripper of FTV Invisio Panels For Horizontal FacadeDocument16 pagesGripper of FTV Invisio Panels For Horizontal FacadefghfNo ratings yet

- Folktalesofkeral 00 MenoDocument124 pagesFolktalesofkeral 00 Menoreena sudhirNo ratings yet

- Bartending and Catering: Agenda: Basics of Bartending Bar Tools and EquipmentDocument146 pagesBartending and Catering: Agenda: Basics of Bartending Bar Tools and EquipmentMars Mar100% (1)

- React Rich Text EditorDocument3 pagesReact Rich Text Editordhirendrapratapsingh398No ratings yet

- Roof Beam Layout - r1Document1 pageRoof Beam Layout - r1Niraj ShindeNo ratings yet

- ISO 9000 Standards Guide Quality Systems InternationallyDocument12 pagesISO 9000 Standards Guide Quality Systems InternationallyArslan Saleem0% (1)