You might also like

- Tax BillDocument1 pageTax BillBrenda SorensonNo ratings yet

- Bank SecrecyDocument12 pagesBank SecrecyRobeh AtudNo ratings yet

- BANKING LAWS - CommercialDocument45 pagesBANKING LAWS - CommercialGenelle Mae MadrigalNo ratings yet

- Modern Drummer Magazine - August 2022Document86 pagesModern Drummer Magazine - August 2022Justin Francis BriggsNo ratings yet

- Family Law PDFDocument416 pagesFamily Law PDFNathan JahanNo ratings yet

- Basel 2.5, Basel III. Their Tasks Are To Identify Risks To The Financial Stability of TheDocument5 pagesBasel 2.5, Basel III. Their Tasks Are To Identify Risks To The Financial Stability of TheSahoo SKNo ratings yet

- Judges and DiscriminationDocument365 pagesJudges and DiscriminationYun YiNo ratings yet

- Knitting Issue 228 2022Document100 pagesKnitting Issue 228 2022Justin Francis Briggs100% (5)

- Maharlika Investment FundDocument4 pagesMaharlika Investment FundMary Ann LubaoNo ratings yet

- TB ch07Document31 pagesTB ch07ajaysatpadi100% (1)

- Mccalls Quilting September October 2022Document98 pagesMccalls Quilting September October 2022Justin Francis Briggs100% (1)

- Loans ReceivableDocument22 pagesLoans ReceivableJendall SisonNo ratings yet

- Transcript SEC Fundamentals Part 1Document10 pagesTranscript SEC Fundamentals Part 1archanaanuNo ratings yet

- Quickbooks AssignmentDocument11 pagesQuickbooks AssignmentTauqeer Ahmed100% (1)

- RA 11057 or The Personal Property Security ActDocument14 pagesRA 11057 or The Personal Property Security ActLaughLy ReuyanNo ratings yet

- Salary Pay Slip Model PDF FreeDocument1 pageSalary Pay Slip Model PDF FreeAYUSH PRADHANNo ratings yet

- Gov. Villafuerte, Jr. and Prov. of Camsur v. RobredoDocument2 pagesGov. Villafuerte, Jr. and Prov. of Camsur v. RobredoNoreenesse SantosNo ratings yet

- Insolvency and Bankruptcy Code RMDocument28 pagesInsolvency and Bankruptcy Code RMSarvy JosephNo ratings yet

- Villafuerte Vs RobredoDocument2 pagesVillafuerte Vs RobredoElyn ApiadoNo ratings yet

- Case DigestDocument10 pagesCase DigestEqui TinNo ratings yet

- SUMMARYDocument44 pagesSUMMARYGenelle Mae MadrigalNo ratings yet

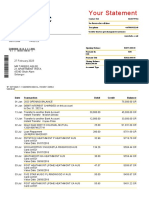

- Bank Statement TareeqDocument2 pagesBank Statement TareeqIzza NabbilaNo ratings yet

- 2007-2010 Banking Bar QuestionsDocument4 pages2007-2010 Banking Bar QuestionsNorhalisa Naga SalicNo ratings yet

- Backtesting Long Short Moving Average Crossover Strategy in ExcelDocument24 pagesBacktesting Long Short Moving Average Crossover Strategy in ExcelKiongboh AngNo ratings yet

- Introduction To Cost AccountingDocument2 pagesIntroduction To Cost AccountingHunson AbadeerNo ratings yet

- ABC of VSA Signs of Weakness PDFDocument17 pagesABC of VSA Signs of Weakness PDFPiet Nijsten100% (1)

- GSIS Family Bank Employees Union v. Villanueva PDFDocument27 pagesGSIS Family Bank Employees Union v. Villanueva PDFgrurocketNo ratings yet

- National Social Security Fund (Amendment) Bill, 2019)Document20 pagesNational Social Security Fund (Amendment) Bill, 2019)The Independent Magazine100% (1)

- Banking NotesDocument17 pagesBanking Notescmv mendozaNo ratings yet

- 5 Province of Batangas vs. Romulo, GR 152774, May 27, 2004Document16 pages5 Province of Batangas vs. Romulo, GR 152774, May 27, 2004Perry YapNo ratings yet

- Villafuerte v. RobredoDocument3 pagesVillafuerte v. RobredoClarisseNo ratings yet

- 'PH Bank Secrecy Laws Strictest in The World Along With LebanonDocument12 pages'PH Bank Secrecy Laws Strictest in The World Along With LebanonjealousmistressNo ratings yet

- ProblemSet Cash Flow EstimationQA-160611 - 021520Document25 pagesProblemSet Cash Flow EstimationQA-160611 - 021520Jonathan Punnalagan100% (2)

- Villafuerte v. RobredoDocument3 pagesVillafuerte v. RobredoClarisseNo ratings yet

- 4 - Legal Cases On Local Budgeting With FactsDocument139 pages4 - Legal Cases On Local Budgeting With FactsAnnbantotNo ratings yet

- Answers To Chapter 13 QuestionsDocument7 pagesAnswers To Chapter 13 QuestionsLe QuangNo ratings yet

- Rejet de La Demande de Gel de La CSG: BM Obtient Des Garanties Malgré Un Premier DésaveuDocument11 pagesRejet de La Demande de Gel de La CSG: BM Obtient Des Garanties Malgré Un Premier DésaveuDefimediaNo ratings yet

- General Banking Act and Classifications of Banks (15nov21)Document5 pagesGeneral Banking Act and Classifications of Banks (15nov21)Robinson MojicaNo ratings yet

- BNK 601 - Tutorial 1 Solutions 2020Document5 pagesBNK 601 - Tutorial 1 Solutions 2020Inoke RawaigagaNo ratings yet

- 2019 March PibDocument30 pages2019 March PibDeepak SinghNo ratings yet

- Denham C.J. O'Donnell J. Mckechnie J. Clarke J. Dunne J. Charleton JDocument46 pagesDenham C.J. O'Donnell J. Mckechnie J. Clarke J. Dunne J. Charleton JRita CahillNo ratings yet

- Qanda: Rbi Docs, Non-Banking Finance Companies in India'S Financial Landscape, Available At: IdDocument8 pagesQanda: Rbi Docs, Non-Banking Finance Companies in India'S Financial Landscape, Available At: IdAparajita MarwahNo ratings yet

- EKHURULENI V GERMISTON MUNICIPALDocument11 pagesEKHURULENI V GERMISTON MUNICIPALNene onetwoNo ratings yet

- E Risk - USSLCaseStudyDocument6 pagesE Risk - USSLCaseStudymadanishkanna5677No ratings yet

- The SAFE Banking Act of 2021Document30 pagesThe SAFE Banking Act of 2021Marijuana Moment100% (1)

- Business Mangement 2Document7 pagesBusiness Mangement 2manjulakrishna2005No ratings yet

- Statutes 1 1Document38 pagesStatutes 1 1edwinNo ratings yet

- The Reserve Bank of India ActDocument36 pagesThe Reserve Bank of India ActShaji MullookkaaranNo ratings yet

- Chapter I: Bangko Sentral NG Pilipinas LawDocument42 pagesChapter I: Bangko Sentral NG Pilipinas Lawyolacz04No ratings yet

- Villafuerte v. RobredoDocument19 pagesVillafuerte v. RobredoLaw SchoolNo ratings yet

- The New Insurance Bill: by An Insurance ManagerDocument3 pagesThe New Insurance Bill: by An Insurance ManagerMogambo KhushNo ratings yet

- The B.E. Journal of Economic Analysis & Policy: TopicsDocument30 pagesThe B.E. Journal of Economic Analysis & Policy: TopicsShahban KhanNo ratings yet

- Young 2009Document32 pagesYoung 2009rabiatul adawiyahNo ratings yet

- LPA3-21-Report On The Administrator General's (Amendment) Bill, 2019 PDFDocument43 pagesLPA3-21-Report On The Administrator General's (Amendment) Bill, 2019 PDFbogere robertNo ratings yet

- However, As A Matter of Observation, Undersigned Wishes To Express Reservation On The Following Sections of The Subject Ordinance, To Quote: 1Document4 pagesHowever, As A Matter of Observation, Undersigned Wishes To Express Reservation On The Following Sections of The Subject Ordinance, To Quote: 1Bayani ParagasNo ratings yet

- State-Interests-And-Gov.-Act (Siga Act)Document18 pagesState-Interests-And-Gov.-Act (Siga Act)Isaac Annan RiversonNo ratings yet

- The Savings and Loan Crisis - Assignment PDFDocument2 pagesThe Savings and Loan Crisis - Assignment PDFtylerNo ratings yet

- Critical Analysis Including Suggestions For ImprovementDocument4 pagesCritical Analysis Including Suggestions For ImprovementAditya DeshmukhNo ratings yet

- BDO Fortescue PaperDocument12 pagesBDO Fortescue Paperpeter_martin9335No ratings yet

- Forgot Villafuerte V RobredoDocument9 pagesForgot Villafuerte V RobredoLou LaguardiaNo ratings yet

- Mortgage Report Ouma-1Document8 pagesMortgage Report Ouma-1Real TrekstarNo ratings yet

- Companies Act 2013 and The Draft Rules Towards Better Corporate GovernanceDocument8 pagesCompanies Act 2013 and The Draft Rules Towards Better Corporate GovernanceNehaNo ratings yet

- Gordon College Olongapo City S.Y. 2017-2018: General Banking Law of 2000 R.A-8791Document14 pagesGordon College Olongapo City S.Y. 2017-2018: General Banking Law of 2000 R.A-8791pasign inNo ratings yet

- S&L CrisisDocument22 pagesS&L CrisisClara MwangolaNo ratings yet

- Maharlika Investment FundsDocument41 pagesMaharlika Investment Fundsangelica merceneNo ratings yet

- PROMESA PREPA - Utier Appointments Complaint WATERMARKDocument26 pagesPROMESA PREPA - Utier Appointments Complaint WATERMARKMetro Puerto RicoNo ratings yet

- Lml4806 Final 2023 No 1Document10 pagesLml4806 Final 2023 No 1Nonofo MkhutshwaNo ratings yet

- 2022 141 Taxmann Com 533 ArticleDocument5 pages2022 141 Taxmann Com 533 ArticleraghavbediNo ratings yet

- The Abridgment of A Flawed Insolvency RegimeDocument10 pagesThe Abridgment of A Flawed Insolvency RegimegurneetNo ratings yet

- The effects of investment regulations on pension funds performance in BrazilFrom EverandThe effects of investment regulations on pension funds performance in BrazilNo ratings yet

- Moviemaker Issue 143 Spring 2022Document86 pagesMoviemaker Issue 143 Spring 2022Justin Francis BriggsNo ratings yet

- CQ 02 February 1980Document100 pagesCQ 02 February 1980Justin Francis BriggsNo ratings yet

- CQ 02 February 1974Document100 pagesCQ 02 February 1974Justin Francis BriggsNo ratings yet

- CQ 01 January 1960Document132 pagesCQ 01 January 1960Justin Francis BriggsNo ratings yet

- LM03263 PDFDocument40 pagesLM03263 PDFJustin Francis BriggsNo ratings yet

- Provincial Gazette ZA GT Vol 24 No 313 Dated 2018 10 31 PDFDocument228 pagesProvincial Gazette ZA GT Vol 24 No 313 Dated 2018 10 31 PDFJustin Francis BriggsNo ratings yet

- Financial Matters Amendment Bill 04022019 PDFDocument28 pagesFinancial Matters Amendment Bill 04022019 PDFJustin Francis BriggsNo ratings yet

- Disaster Management Act, 2002: Amendment of Regulations Issued in Terms of Section 27Document20 pagesDisaster Management Act, 2002: Amendment of Regulations Issued in Terms of Section 27Justin Francis BriggsNo ratings yet

- Staatskoerant, 11 Oktober 2013 No. 36907 101Document1 pageStaatskoerant, 11 Oktober 2013 No. 36907 101Justin Francis BriggsNo ratings yet

- South African National Health Act of 2003Document49 pagesSouth African National Health Act of 2003Justin Francis BriggsNo ratings yet

- The Labour Court of South Africa, Johannesburg JudgmentDocument15 pagesThe Labour Court of South Africa, Johannesburg JudgmentJustin Francis BriggsNo ratings yet

- Department of Trade and Industry, Draft Liqour Amendent Bill of 2016Document24 pagesDepartment of Trade and Industry, Draft Liqour Amendent Bill of 2016Justin Francis BriggsNo ratings yet

- Saving, Investment and The Financial SystemDocument47 pagesSaving, Investment and The Financial SystemKaifNo ratings yet

- Supply Side PoliciesDocument5 pagesSupply Side PoliciesVanessa KuaNo ratings yet

- HT Connection DocumentsDocument2 pagesHT Connection Documentsdan_geplNo ratings yet

- Tata Power Compensation 2013Document5 pagesTata Power Compensation 2013Vivek SinghNo ratings yet

- 09-PCSO2019 Part2-Observations and RecommDocument40 pages09-PCSO2019 Part2-Observations and RecommdemosreaNo ratings yet

- AMCO-11006822-V1-Prosus N V ProspectusDocument426 pagesAMCO-11006822-V1-Prosus N V ProspectussuedelopeNo ratings yet

- ACCT 6011 Assignment #1 TemplateDocument8 pagesACCT 6011 Assignment #1 Templatepatel avaniNo ratings yet

- The Anatomy of A Transaction 020311Document1 pageThe Anatomy of A Transaction 020311ealpeshpatelNo ratings yet

- Trial Balance - For The Month of June 2014: Jawat Johan SDN BHDDocument8 pagesTrial Balance - For The Month of June 2014: Jawat Johan SDN BHDchabiconNo ratings yet

- 1) Leung Yee V Strong Machinery Co., G.R. No. L-11658, 15 Feb. 1918, 37 Phil 644Document3 pages1) Leung Yee V Strong Machinery Co., G.R. No. L-11658, 15 Feb. 1918, 37 Phil 644TrinNo ratings yet

- Corporate Banking Chapter 2 PDFDocument38 pagesCorporate Banking Chapter 2 PDFMuhammad shazibNo ratings yet

- Assignment September 2020 Semester: Subject Code MKM602 Subject Title Marketing Management Level Master'S DegreeDocument15 pagesAssignment September 2020 Semester: Subject Code MKM602 Subject Title Marketing Management Level Master'S Degreemahnoor arifNo ratings yet

- PC-1 Project DigestDocument9 pagesPC-1 Project DigestWaleed Khalid100% (1)

- Additonal CVP QuestionsDocument2 pagesAdditonal CVP QuestionsDianne Madrid0% (1)

- Muh. SyukurDocument6 pagesMuh. SyukurDrawing For LifeNo ratings yet

- Multinational CorporationsDocument26 pagesMultinational CorporationsHarshal ShindeNo ratings yet

- Kanika Khurana: 2018. Clients Experience IncludesDocument3 pagesKanika Khurana: 2018. Clients Experience IncludesjfrNo ratings yet

- Accounting Standard 11Document10 pagesAccounting Standard 11api-3828505100% (1)

- Government Gazette - 20th October, 2017Document96 pagesGovernment Gazette - 20th October, 2017istructeNo ratings yet

- Citibank CaseDocument6 pagesCitibank CaseLalatendu Das0% (1)