You might also like

- CIMA Ba2chapter6Document21 pagesCIMA Ba2chapter6sylvesterNo ratings yet

- Leverage and Capital StructureDocument8 pagesLeverage and Capital StructureC H ♥ N T ZNo ratings yet

- Break Even-Analysis: By, Abhilash.k Pgdm-A P11103Document17 pagesBreak Even-Analysis: By, Abhilash.k Pgdm-A P11103Abhilash KallayilNo ratings yet

- CVP AnalysisDocument18 pagesCVP AnalysisKashvi MakadiaNo ratings yet

- 19 Costs of ProductionDocument5 pages19 Costs of ProductionHiNo ratings yet

- Tgs MenejDocument13 pagesTgs MenejAnita MangootNo ratings yet

- For ReportingDocument6 pagesFor ReportingColeen Rich - BobierNo ratings yet

- Final Project of Cost Accounting - 88683650Document16 pagesFinal Project of Cost Accounting - 88683650nidhi UnnikrishnanNo ratings yet

- Break-Even Analysis PDFDocument4 pagesBreak-Even Analysis PDFirvin5de5los5riosNo ratings yet

- CVP Analysis Break-Even PointDocument5 pagesCVP Analysis Break-Even PointApril Jeeleane RecioNo ratings yet

- Final Project of Cost AccountingDocument16 pagesFinal Project of Cost AccountingMariya Saeed100% (1)

- Breakeven Point AnalysisDocument7 pagesBreakeven Point AnalysisronaldNo ratings yet

- BepDocument5 pagesBeparjun435No ratings yet

- Break-Even Point, Return On Investment and Return On SalesDocument8 pagesBreak-Even Point, Return On Investment and Return On SalesGaurav kumarNo ratings yet

- Cost Volume Profit AnalysisDocument4 pagesCost Volume Profit AnalysisPratiksha GaikwadNo ratings yet

- Break Even AnalysisDocument9 pagesBreak Even AnalysisBankatesh ChoudharyNo ratings yet

- Marginal CostDocument25 pagesMarginal Costkautilya_09No ratings yet

- ACN Final AssignmentDocument12 pagesACN Final AssignmenttonmoyNo ratings yet

- CVP Analysis Objectives and MethodsDocument5 pagesCVP Analysis Objectives and MethodsSajedul AlamNo ratings yet

- Break EvenDocument5 pagesBreak EvenPratham PunawalaNo ratings yet

- Sensitivity Analysis and Uncertainty in CVPDocument12 pagesSensitivity Analysis and Uncertainty in CVPsinghalok1980No ratings yet

- Break Even Point AnalysisDocument11 pagesBreak Even Point AnalysisRose Munyasia100% (2)

- Break-even Point Analysis: Determine When Profits BeginDocument29 pagesBreak-even Point Analysis: Determine When Profits BeginDr. Yogesh Kumar SharmaNo ratings yet

- Break Even Analysis PresentationDocument32 pagesBreak Even Analysis PresentationShivam Verma 5127No ratings yet

- Break Even AnalysisDocument15 pagesBreak Even AnalysisPawan BiswaNo ratings yet

- Break-even Point ExplainedDocument5 pagesBreak-even Point Explainedsarthakm80No ratings yet

- Break-Even Point NotesDocument3 pagesBreak-Even Point NotesMinu Mary Jolly100% (1)

- What Is The Breakeven Point (BEP) ?Document4 pagesWhat Is The Breakeven Point (BEP) ?Muhammad NazmuddinNo ratings yet

- Breakeven PointDocument4 pagesBreakeven PointHershey ReyesNo ratings yet

- Break-Even / Cost-Volume-Profit Analysis: by S.ClementDocument31 pagesBreak-Even / Cost-Volume-Profit Analysis: by S.ClementAayush JaiswalNo ratings yet

- Marginal AnalysisDocument6 pagesMarginal AnalysisSha MatNo ratings yet

- BEP NotesDocument5 pagesBEP NotesAbhijit PaulNo ratings yet

- Why firms reach shutdown points and how to determine when to shutdown productionDocument3 pagesWhy firms reach shutdown points and how to determine when to shutdown productionPinky DaisiesNo ratings yet

- Presented By: Lutfi Ms Ananthakrishnan Malavika Sreekumar Manilal Kasera Mitesh KumarDocument14 pagesPresented By: Lutfi Ms Ananthakrishnan Malavika Sreekumar Manilal Kasera Mitesh KumarManilal kaseraNo ratings yet

- Cost Volume Profit AnalysisDocument7 pagesCost Volume Profit Analysissofyan timotyNo ratings yet

- Presented By:: Group NoDocument14 pagesPresented By:: Group NoAbhinav SharmaNo ratings yet

- Break-even analysis explainedDocument5 pagesBreak-even analysis explainedlojainNo ratings yet

- Break Even AnalysisDocument3 pagesBreak Even AnalysisShiv MalhotraNo ratings yet

- 03-04-2012Document62 pages03-04-2012Adeel AliNo ratings yet

- Understand Break-Even Analysis in 40 CharactersDocument8 pagesUnderstand Break-Even Analysis in 40 CharactersashokchhotuNo ratings yet

- Break-Even AnalysisDocument2 pagesBreak-Even AnalysisMahadie HasanNo ratings yet

- BEP AnalysisDocument7 pagesBEP Analysissumaya tasnimNo ratings yet

- BEP CalculationDocument3 pagesBEP CalculationGaming WarriorNo ratings yet

- Cost-Volume-Profit Analysis: Fixed CostsDocument9 pagesCost-Volume-Profit Analysis: Fixed CostsSatarupa BhoiNo ratings yet

- Importance of Break-Even Point For A Manager in Decision MakingDocument6 pagesImportance of Break-Even Point For A Manager in Decision MakingAnkita DasNo ratings yet

- Break-Even Analysis: Understanding the BEP, Contribution Margin and MOSDocument17 pagesBreak-Even Analysis: Understanding the BEP, Contribution Margin and MOSRobinson GnanaduraiNo ratings yet

- CVP Analysis Break-Even Point ProfitDocument6 pagesCVP Analysis Break-Even Point ProfitMark Aldrich Ubando0% (1)

- Break-Even PointDocument6 pagesBreak-Even Pointsheebakbs5144No ratings yet

- CVP Analysis: Cost-Volume-Profit RelationshipsDocument4 pagesCVP Analysis: Cost-Volume-Profit RelationshipsSayed HossainNo ratings yet

- Break Even Point Analysis Definition, Explanation Formula and CalculationDocument5 pagesBreak Even Point Analysis Definition, Explanation Formula and CalculationTelemetric Sight100% (2)

- What Is Break Even Analysis?: Cost Accounting Total Revenue Fixed and Variable CostsDocument9 pagesWhat Is Break Even Analysis?: Cost Accounting Total Revenue Fixed and Variable CostsShuvro RahmanNo ratings yet

- Break Even Analysis in ProductionDocument17 pagesBreak Even Analysis in Productionyashwant4043994No ratings yet

- Cost-Volume-profit Analysis NotesDocument20 pagesCost-Volume-profit Analysis Notestmpvd6gw8fNo ratings yet

- 03 Cost Volume Profit AnalysisDocument6 pages03 Cost Volume Profit AnalysisPhoebe WalastikNo ratings yet

- Business Math Week 7 ReportingDocument7 pagesBusiness Math Week 7 ReportingRalph EgeNo ratings yet

- Question AnswerDocument6 pagesQuestion AnswerSoloymanNo ratings yet

- Breakeven PointDocument7 pagesBreakeven PointronaldNo ratings yet

- Accounting, Maths and Computing for Business Studies V11 Home StudyFrom EverandAccounting, Maths and Computing for Business Studies V11 Home StudyNo ratings yet

- Learn Accounting, Maths and Computing for Business Studies on Your SmartphoneFrom EverandLearn Accounting, Maths and Computing for Business Studies on Your SmartphoneNo ratings yet

- Accounting, Maths and Computing Principles for Business Studies Teachers Pack V11From EverandAccounting, Maths and Computing Principles for Business Studies Teachers Pack V11No ratings yet

- Document GhjkjhghjkoihugyhyhjiklDocument3 pagesDocument GhjkjhghjkoihugyhyhjikleuqehtbNo ratings yet

- Pas 12Document6 pagesPas 12AnneNo ratings yet

- CallidusCloud Training Overview BrochureDocument2 pagesCallidusCloud Training Overview Brochuregupta_pankajkr5626No ratings yet

- Life Cycle CostingDocument4 pagesLife Cycle CostingSanjay Kumar SinghNo ratings yet

- Astrology Setup GuideLinesDocument15 pagesAstrology Setup GuideLinesVipul JujarNo ratings yet

- Inventory EstimationDocument4 pagesInventory EstimationShy Ng0% (1)

- Questionnare BookletDocument36 pagesQuestionnare BookletCaldito RockNo ratings yet

- For The Exclusive Use of N. TAKEZAWA, 2019.: Nike, Inc.: Cost of CapitalDocument8 pagesFor The Exclusive Use of N. TAKEZAWA, 2019.: Nike, Inc.: Cost of CapitalVidura Dilshan HewagamaNo ratings yet

- E - Business Management Prevoius Year Quetion PaperDocument9 pagesE - Business Management Prevoius Year Quetion Papersallavudeen ashwinNo ratings yet

- JIT For Lean Manufacturing FinalDocument83 pagesJIT For Lean Manufacturing FinalMusical CorruptionNo ratings yet

- Global-Talent-Monitor EVPDocument19 pagesGlobal-Talent-Monitor EVPJosé F. NetoNo ratings yet

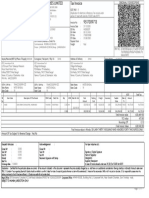

- Tax Invoice for ACSR ZEBRA CONDUCTOR, UNGREASED from APAR INDUSTRIES LIMITED to KEC International LtdDocument1 pageTax Invoice for ACSR ZEBRA CONDUCTOR, UNGREASED from APAR INDUSTRIES LIMITED to KEC International LtdDoita Dutta ChoudhuryNo ratings yet

- Template Organizational ChartDocument11 pagesTemplate Organizational ChartJess SidadologNo ratings yet

- Ch20 PensionDocument17 pagesCh20 PensionEmma Mariz Garcia100% (1)

- System analysis and design process overviewDocument13 pagesSystem analysis and design process overviewCassandra FrancescaNo ratings yet

- BDAP2203 Management AccountingDocument7 pagesBDAP2203 Management Accountingdicky chongNo ratings yet

- Sycip Salazar Hernandez GatmaitanDocument3 pagesSycip Salazar Hernandez GatmaitanLoren SanapoNo ratings yet

- Bobs Coffee ShopDocument1 pageBobs Coffee Shopz zzzNo ratings yet

- Sap Fico, Introduction, Sap Fico Fullform, Sap Fico Course, What Is Sap FicoDocument8 pagesSap Fico, Introduction, Sap Fico Fullform, Sap Fico Course, What Is Sap Ficopoojaw.allenticsNo ratings yet

- Campus Recruitment ProposalDocument2 pagesCampus Recruitment ProposalAmit Mitra100% (1)

- LLP Agreement for Business Advisory FirmDocument22 pagesLLP Agreement for Business Advisory FirmRamanil AnkurNo ratings yet

- Target Dental Patients with SegmentationDocument10 pagesTarget Dental Patients with Segmentationaj4444No ratings yet

- SalesDocument3 pagesSalesEdgardo MartinezNo ratings yet

- 03 - Clubs and Societies Complete Notes-1 PDFDocument13 pages03 - Clubs and Societies Complete Notes-1 PDFDanny FarrukhNo ratings yet

- Financial Markets and Institutions 8th Edition Mishkin Eakins Solutions Manual Instant DownloadDocument6 pagesFinancial Markets and Institutions 8th Edition Mishkin Eakins Solutions Manual Instant DownloadEng Abdikarim WalhadNo ratings yet

- Bayer CropScience Limited 2021-22 - Web Upload (17 MB) - IndiaDocument192 pagesBayer CropScience Limited 2021-22 - Web Upload (17 MB) - IndiaAadarsh jainNo ratings yet

- This Study Resource Was: Use The Following Information For The Next Two QuestionsDocument2 pagesThis Study Resource Was: Use The Following Information For The Next Two QuestionsClaudette Clemente100% (1)

- Modeling with Linear Programming in ExcelDocument1 pageModeling with Linear Programming in ExcelNirmal SubudhiNo ratings yet

- August 2017 Wells Fargo StatementDocument11 pagesAugust 2017 Wells Fargo StatementAnonymous qQaGsVkFNo ratings yet

- Comprehensive Planning TemplateDocument21 pagesComprehensive Planning TemplateErnan BaldomeroNo ratings yet