You might also like

- BankNotes Feb 2012Document12 pagesBankNotes Feb 2012Michael HeidbrinkNo ratings yet

- Solow - Dumb and Dumber in Macroeconomics PDFDocument3 pagesSolow - Dumb and Dumber in Macroeconomics PDFjrodascNo ratings yet

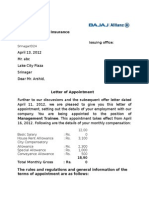

- Appointment Letter Format For Bajaj AllianzDocument4 pagesAppointment Letter Format For Bajaj Allianzmir_umaramin100% (2)

- Honest Money: John TomlinsonDocument77 pagesHonest Money: John Tomlinsonrifishman100% (1)

- Grants Interest Rate ObserverDocument28 pagesGrants Interest Rate ObserverZerohedgeNo ratings yet

- The General Theory of Employment, Interest and Money. IllustratedFrom EverandThe General Theory of Employment, Interest and Money. IllustratedRating: 3.5 out of 5 stars3.5/5 (18)

- Banking FinalsDocument15 pagesBanking FinalsApril CastilloNo ratings yet

- Whelan Lecture NotesDocument361 pagesWhelan Lecture NotesAahaanaNo ratings yet

- Pathfinders Traders TrainingsDocument58 pagesPathfinders Traders TrainingsSameer ShindeNo ratings yet

- Economics for the Rest of Us: Debunking the Science that Makes Life DismalFrom EverandEconomics for the Rest of Us: Debunking the Science that Makes Life DismalRating: 4 out of 5 stars4/5 (12)

- Long Quiz Overview Pas23 ReviewerDocument15 pagesLong Quiz Overview Pas23 ReviewerHassanhor Guro Bacolod100% (1)

- Where Keynes Went Wrong Hunter LewisDocument513 pagesWhere Keynes Went Wrong Hunter LewisChris Campbell100% (1)

- Mark Carney's False IdeologyDocument5 pagesMark Carney's False IdeologySimone MenciassiNo ratings yet

- Macroeconomic Crisis and The Social OrderDocument14 pagesMacroeconomic Crisis and The Social OrderflipperNo ratings yet

- InterviewDocument5 pagesInterviewAdminAliNo ratings yet

- Blogs / Cosmic Variance: Where We Are On The Laffer CurveDocument27 pagesBlogs / Cosmic Variance: Where We Are On The Laffer CurvetskokoNo ratings yet

- Antenarrating Economy1Document3 pagesAntenarrating Economy1Wilfred BerendsenNo ratings yet

- Principle 10 - FINALDocument6 pagesPrinciple 10 - FINALJapaninaNo ratings yet

- Fundamental Driven Liquidity Traps: A Unified Theory of The Great Depression and The Great RecessionDocument97 pagesFundamental Driven Liquidity Traps: A Unified Theory of The Great Depression and The Great RecessionBidyut Bhusan PandaNo ratings yet

- 2022-09-08 - Hward Marks Memo - Illusion-of-KnowledgeDocument14 pages2022-09-08 - Hward Marks Memo - Illusion-of-KnowledgeappujisNo ratings yet

- MA For PADMDocument100 pagesMA For PADMLelisa MergaNo ratings yet

- Mauldin April 26Document16 pagesMauldin April 26richardck61No ratings yet

- Lucas - in Defense of The Dismal ScienceDocument3 pagesLucas - in Defense of The Dismal ScienceLucianaNo ratings yet

- Aea 206 Macroeconomics PDFDocument187 pagesAea 206 Macroeconomics PDFmarikiannawNo ratings yet

- Keynesian Economics: The Beginning of The End Steven Kates RMIT University Melbourne AustraliaDocument10 pagesKeynesian Economics: The Beginning of The End Steven Kates RMIT University Melbourne AustraliaLei Kuok KinNo ratings yet

- 806 1Document23 pages806 1Muhammad NomanNo ratings yet

- Information and The Change in The ParadiDocument69 pagesInformation and The Change in The ParadiNikita MazurenkoNo ratings yet

- Kenneth Boulding's ReconstructionDocument20 pagesKenneth Boulding's ReconstructionDCS Noé Hernández CortezNo ratings yet

- AlasdaircLeod GibsonsParadoxDocument17 pagesAlasdaircLeod GibsonsParadoxron9123No ratings yet

- CrisisInEconTheory AKirman2009Document22 pagesCrisisInEconTheory AKirman2009RanulfoNo ratings yet

- First Lecture MDocument9 pagesFirst Lecture MalyNo ratings yet

- Some Thoughts On DeflationDocument9 pagesSome Thoughts On Deflationrichardck30No ratings yet

- David Harvey, Rate and Mass, NLR 130, July August 2021Document26 pagesDavid Harvey, Rate and Mass, NLR 130, July August 2021Patrick MaddenNo ratings yet

- An Agenda For Reforming Economic Theory: Paradigm in Monetary Economics, Cambridge University Press, 2003Document15 pagesAn Agenda For Reforming Economic Theory: Paradigm in Monetary Economics, Cambridge University Press, 2003api-26091012No ratings yet

- Fix Stagflation Cause 20230126Document15 pagesFix Stagflation Cause 20230126pipel sedeesNo ratings yet

- The Shaky Art of Economic BubblesDocument12 pagesThe Shaky Art of Economic BubblesHassanAhmed73No ratings yet

- Macroec IDocument109 pagesMacroec IProveedor Iptv España100% (1)

- Introducing Economic Actualism: Making the Science of Rational Behavior More RationalFrom EverandIntroducing Economic Actualism: Making the Science of Rational Behavior More RationalNo ratings yet

- An Introduction To Economic Analysis: After Reading This Chapter, You Will Be Conversant WithDocument6 pagesAn Introduction To Economic Analysis: After Reading This Chapter, You Will Be Conversant WithVignesh MohanrajNo ratings yet

- Case Stud ConcluDocument1 pageCase Stud ConcluJhesebel LimbuanNo ratings yet

- Lessons From The 1930sDocument19 pagesLessons From The 1930sGeorge_G92No ratings yet

- NullDocument7 pagesNullapi-26172897No ratings yet

- Paul Romer The Trouble With Macroeconomics PDFDocument26 pagesPaul Romer The Trouble With Macroeconomics PDFWellington MigliariNo ratings yet

- Lesson 1 Economics and MicroeconomicsDocument4 pagesLesson 1 Economics and Microeconomicskellycolette3488No ratings yet

- Tom's Outlook 2nd Quarter 2009Document7 pagesTom's Outlook 2nd Quarter 2009Keynes2009No ratings yet

- Knowledge SessionDocument8 pagesKnowledge Sessionsnehapawar02No ratings yet

- Mauldin March 29Document18 pagesMauldin March 29richardck61No ratings yet

- Half A Bubble Off Dead CenterDocument14 pagesHalf A Bubble Off Dead Centerrichardck61No ratings yet

- The Cyclicity of Debt: Time Value of MoneyDocument18 pagesThe Cyclicity of Debt: Time Value of MoneyPrachi GargNo ratings yet

- Smith 2016 International FinanceDocument11 pagesSmith 2016 International Financedebnathsuman49No ratings yet

- Nouriel Roubini John MakinDocument15 pagesNouriel Roubini John MakinSamy SudanNo ratings yet

- Pure Exchange Equilibrium of Dynamic Economic ModelsDocument25 pagesPure Exchange Equilibrium of Dynamic Economic Modelsmmarko1No ratings yet

- Leijonhufvud, A. Information and Coordination Cap. 9 y 10Document63 pagesLeijonhufvud, A. Information and Coordination Cap. 9 y 10Biblioteca U de San AndrésNo ratings yet

- Teaching Economics Skidelsky PDFDocument4 pagesTeaching Economics Skidelsky PDFMallu MunizNo ratings yet

- Chapter OneDocument33 pagesChapter OneTesfahun GetachewNo ratings yet

- Eco Iia U1Document13 pagesEco Iia U1Yunior CenNo ratings yet

- Mauldin October 12Document5 pagesMauldin October 12richardck61No ratings yet

- Reading 1.1Document6 pagesReading 1.122eco2088No ratings yet

- Tbs Macro Homework 2 Due On Last TutorialDocument4 pagesTbs Macro Homework 2 Due On Last TutorialOussemaNo ratings yet

- Sample Lecture: Giving You All The Answers Up FrontDocument3 pagesSample Lecture: Giving You All The Answers Up FrontMipsNo ratings yet

- Is Government Spending Too Easy An AnswerDocument11 pagesIs Government Spending Too Easy An Answerfarik007No ratings yet

- System Failure: The Falling Rate of Profit and The Economic CrisisDocument7 pagesSystem Failure: The Falling Rate of Profit and The Economic CrisiszizekNo ratings yet

- A Joosr Guide to... Capital in the Twenty-First Century by Thomas PikettyFrom EverandA Joosr Guide to... Capital in the Twenty-First Century by Thomas PikettyNo ratings yet

- LinkedIn ProxyDocument220 pagesLinkedIn ProxyinafriedNo ratings yet

- Chapter 2 Introduction To Behavioral AnalysisDocument7 pagesChapter 2 Introduction To Behavioral AnalysisSwee Yi LeeNo ratings yet

- Significance of Risk Management and TakafulDocument6 pagesSignificance of Risk Management and TakafulAli MunavvaruNo ratings yet

- Financial System in PakistanDocument13 pagesFinancial System in PakistanMuhammad IrfanNo ratings yet

- Bank of Maldives: Head Office, Boduthakurufaanu Magu MaleDocument22 pagesBank of Maldives: Head Office, Boduthakurufaanu Magu MalemikeNo ratings yet

- Sample ContractDocument3 pagesSample ContractBonaventure NzeyimanaNo ratings yet

- Module A Stage1Document11 pagesModule A Stage1ejoghenetaNo ratings yet

- Recovered File 1Document27 pagesRecovered File 1RoxySyazlyna0% (1)

- NIT No. e - 02/EE (E) /vadodara /2021-22/recall-2Document35 pagesNIT No. e - 02/EE (E) /vadodara /2021-22/recall-2ruchita vishnoiNo ratings yet

- Objectives and Research Methodology: ObjectiveDocument82 pagesObjectives and Research Methodology: ObjectiveRahul RanjanNo ratings yet

- Digital Entrepreneurship in Kenya 2014 PDFDocument86 pagesDigital Entrepreneurship in Kenya 2014 PDFSutarjo9No ratings yet

- MOW Marketing PlanDocument29 pagesMOW Marketing Plandanlor1991100% (1)

- Impairment of AssetsDocument21 pagesImpairment of AssetsDeryl GalveNo ratings yet

- FIN 360 Mock ExamDocument1 pageFIN 360 Mock ExamSkrybeNo ratings yet

- Irc Wash Water Kabarole, UgandaDocument13 pagesIrc Wash Water Kabarole, UgandajadwongscribdNo ratings yet

- Ey The Insolvency and Bankruptcy Code 2016 An Overview PDFDocument6 pagesEy The Insolvency and Bankruptcy Code 2016 An Overview PDFRaghav DhootNo ratings yet

- Process Costing-WIPDocument3 pagesProcess Costing-WIPSigei LeonardNo ratings yet

- Grade 7 EMS Exam November 2018 WatermarkDocument11 pagesGrade 7 EMS Exam November 2018 WatermarkGomolemo MolapongNo ratings yet

- YÖKDİL Sosyal Phrasal Verb Soru Tipi PDFDocument6 pagesYÖKDİL Sosyal Phrasal Verb Soru Tipi PDFTunahan KüçükerNo ratings yet

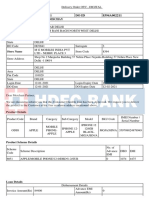

- Application ID 8394A00221 Do Id 8394A002211: Customer Name Nischay NischayDocument2 pagesApplication ID 8394A00221 Do Id 8394A002211: Customer Name Nischay NischayAnonymous tOgAKZ8No ratings yet

- List of Branches of Brokerage Firms 09.04.2019Document87 pagesList of Branches of Brokerage Firms 09.04.2019Muhammad AtharNo ratings yet

- Indore-Hfl Certificate For The Financial Year 2021-22Document79 pagesIndore-Hfl Certificate For The Financial Year 2021-22seema wahaneNo ratings yet

- Capital MarketDocument41 pagesCapital MarketAhmed Jan DahriNo ratings yet

- Blue and Grey Minimalist CV Finance Manager Resume - 20231214 - 201814 - 0000Document2 pagesBlue and Grey Minimalist CV Finance Manager Resume - 20231214 - 201814 - 0000walid.chiiloubNo ratings yet

- Chipotle Shareholders LawsuitDocument24 pagesChipotle Shareholders LawsuitEaterNo ratings yet

- Time Value of Money NEW FINALDocument38 pagesTime Value of Money NEW FINALAwais A.No ratings yet