You might also like

- SOV E05169BCOM PBD Answer SchemeDocument7 pagesSOV E05169BCOM PBD Answer SchemeNeeraj KrishnaNo ratings yet

- International Economics 9Th Edition Appleyard Solutions Manual Full Chapter PDFDocument34 pagesInternational Economics 9Th Edition Appleyard Solutions Manual Full Chapter PDFedward.archer149100% (13)

- International Economics 9th Edition Appleyard Solutions Manual DownloadDocument13 pagesInternational Economics 9th Edition Appleyard Solutions Manual DownloadElna Todd100% (22)

- SYDE 262 Assignment 3 Sample SolutionDocument15 pagesSYDE 262 Assignment 3 Sample SolutionRachelNo ratings yet

- Lect 3 Part 1. The Econ of Prodn Cost and Profit MaximizationDocument17 pagesLect 3 Part 1. The Econ of Prodn Cost and Profit MaximizationkonchojNo ratings yet

- Econ SG Chap08Document20 pagesEcon SG Chap08CLNo ratings yet

- Practical Lesson 1.2 "Optimization of Costs For Marketing MarketDocument9 pagesPractical Lesson 1.2 "Optimization of Costs For Marketing MarketMax TimoshenkoNo ratings yet

- 1 56183 566 8 - 27Document26 pages1 56183 566 8 - 27sabza0590% (1)

- UD Econ Comps Study GuideDocument23 pagesUD Econ Comps Study GuideUDeconNo ratings yet

- Break Even AnalysisDocument4 pagesBreak Even Analysissatavahan_yNo ratings yet

- Gra 65161 - 201820 - 14.12.2018 - EgDocument9 pagesGra 65161 - 201820 - 14.12.2018 - EgHien NgoNo ratings yet

- CH 06Document12 pagesCH 06LinNo ratings yet

- Theory of PricingDocument48 pagesTheory of PricingDedipyaNo ratings yet

- DAY 3 Cost AcctgDocument7 pagesDAY 3 Cost AcctgLovenia MagpatocNo ratings yet

- Chapter 13 and 14Document73 pagesChapter 13 and 14Maj Icalina CulatonNo ratings yet

- 1 ++Marginal+CostingDocument71 pages1 ++Marginal+CostingB GANAPATHYNo ratings yet

- Econ203 Lab 081Document36 pagesEcon203 Lab 081api-235832666No ratings yet

- Microeconomics Principles and Applications 6th Edition Hall Solutions ManualDocument17 pagesMicroeconomics Principles and Applications 6th Edition Hall Solutions ManualGeorgePalmerkqgd100% (39)

- Managerial EconomicsDocument10 pagesManagerial EconomicsMansi SharmaNo ratings yet

- EC3099 - Industrial Economics - 2007 Exam - Zone-ADocument4 pagesEC3099 - Industrial Economics - 2007 Exam - Zone-AAishwarya PotdarNo ratings yet

- Inferior Good. 1 (Positive), It Is A Luxury Good or A Superior GoodDocument14 pagesInferior Good. 1 (Positive), It Is A Luxury Good or A Superior GoodSakshi AgarwalNo ratings yet

- Perfect CompetitionDocument15 pagesPerfect CompetitionFabian MtiroNo ratings yet

- Break-Even AnalysisDocument37 pagesBreak-Even Analysismablekos13No ratings yet

- Midterm - Basic Micro Economics - Lesson 1Document11 pagesMidterm - Basic Micro Economics - Lesson 1Nhiel Bryan BersaminaNo ratings yet

- Economic IDocument24 pagesEconomic ICarlo Widjaja100% (1)

- Group 7 HandoutsDocument10 pagesGroup 7 HandoutsCoke Aidenry SaludoNo ratings yet

- ECO402 FinalTerm QuestionsandAnswersPreparationbyVirtualiansSocialNetworkDocument20 pagesECO402 FinalTerm QuestionsandAnswersPreparationbyVirtualiansSocialNetworkranashair9919No ratings yet

- Break Even PointDocument11 pagesBreak Even PointAseel JameelNo ratings yet

- Market Structure in EconomicsDocument11 pagesMarket Structure in EconomicsOh ok SodryNo ratings yet

- Aggregate Supply & Business Cycles: Unit HighlightsDocument14 pagesAggregate Supply & Business Cycles: Unit HighlightsprabodhNo ratings yet

- Lesson 1: Theory of Costs Module Title:: Polytechnic College of BotolanDocument14 pagesLesson 1: Theory of Costs Module Title:: Polytechnic College of BotolanRodrick RamosNo ratings yet

- Evaluating PCDocument12 pagesEvaluating PCNigel YeoNo ratings yet

- Cost Volume Profit AnalysisDocument64 pagesCost Volume Profit AnalysisGUDATA ABARANo ratings yet

- Managerial Decisions For Firms With Market Power: Essential ConceptsDocument8 pagesManagerial Decisions For Firms With Market Power: Essential ConceptsRohit SinhaNo ratings yet

- General Instructions:: Hence, The Correct Answer Is Option A'Document22 pagesGeneral Instructions:: Hence, The Correct Answer Is Option A'Ashish GangwalNo ratings yet

- Economics For Today 5th Edition Layton Solutions ManualDocument10 pagesEconomics For Today 5th Edition Layton Solutions Manualcassandracruzpkteqnymcf100% (33)

- Workbook Answers: AQA A2 Economics Unit 3Document25 pagesWorkbook Answers: AQA A2 Economics Unit 3New IdNo ratings yet

- Business Economics: Q F (K, L, La)Document5 pagesBusiness Economics: Q F (K, L, La)Deep BhutaNo ratings yet

- Cost Volume Profit (CVP) AnalysisDocument60 pagesCost Volume Profit (CVP) AnalysisEtsub SamuelNo ratings yet

- Perfect Competition Lecture NotesDocument7 pagesPerfect Competition Lecture NotesVlad Guzunov100% (1)

- Text 2Document4 pagesText 2Leesan Ul NabiNo ratings yet

- 10e 12 Chap Student WorkbookDocument23 pages10e 12 Chap Student WorkbookkartikartikaaNo ratings yet

- Ebook Economics For Today 5Th Edition Layton Solutions Manual Full Chapter PDFDocument31 pagesEbook Economics For Today 5Th Edition Layton Solutions Manual Full Chapter PDFenstatequatrain1jahl100% (9)

- Unit IV (Cost & Revenue Analysis)Document26 pagesUnit IV (Cost & Revenue Analysis)Helik SoniNo ratings yet

- Economics For Managers: Wwu MünsterDocument100 pagesEconomics For Managers: Wwu MünsterAditya SrivastavaNo ratings yet

- Key Diagrams A2 Business EconomicsDocument16 pagesKey Diagrams A2 Business EconomicsEl Niño SajidNo ratings yet

- Cost II Chapter1Document9 pagesCost II Chapter1Dureti NiguseNo ratings yet

- Profit MaximisationDocument6 pagesProfit MaximisationAlexcorbinNo ratings yet

- Pricing Decisions: How Have The Syllabus Learning Outcomes Been Examined?Document14 pagesPricing Decisions: How Have The Syllabus Learning Outcomes Been Examined?Oana AvramNo ratings yet

- Perfect Competition: Market PowerDocument13 pagesPerfect Competition: Market Powerdenny_sitorusNo ratings yet

- Management Accounting AssignmentDocument21 pagesManagement Accounting AssignmentAadi KaushikNo ratings yet

- Management Accounting AssignmentDocument21 pagesManagement Accounting AssignmentAadi KaushikNo ratings yet

- Management Accounting AssignmentDocument21 pagesManagement Accounting AssignmentAadi KaushikNo ratings yet

- Mas 04 - CVP AnalysisDocument7 pagesMas 04 - CVP AnalysisCarl Angelo LopezNo ratings yet

- Chapter Nine Pure CompetitionDocument14 pagesChapter Nine Pure CompetitionCharmaine CruzNo ratings yet

- Micro Notes Chapter 6Document5 pagesMicro Notes Chapter 6D HoNo ratings yet

- MGMT Science Notes 03 CVP AnalysisDocument8 pagesMGMT Science Notes 03 CVP AnalysismichelleNo ratings yet

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageFrom EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- Finance for Non-Financiers 2: Professional FinancesFrom EverandFinance for Non-Financiers 2: Professional FinancesNo ratings yet

- Syllabus Ap-Microeconomics-Sample 1 1058788v1Document4 pagesSyllabus Ap-Microeconomics-Sample 1 1058788v1api-359133069No ratings yet

- Concept Screening-PostedDocument16 pagesConcept Screening-PostedCintia NurliyanaNo ratings yet

- Read Me Advertise Better FaDocument40 pagesRead Me Advertise Better FaDali Ben GouissemNo ratings yet

- A Market Research ON: "Chocolates"Document26 pagesA Market Research ON: "Chocolates"mohitfrequentNo ratings yet

- PR and Communications Organization Structure: Public RelationsDocument2 pagesPR and Communications Organization Structure: Public RelationsYahia Mustafa AlfazaziNo ratings yet

- Tesco Returns To The Corner Shops of England's Past: Hult International Business SchoolDocument9 pagesTesco Returns To The Corner Shops of England's Past: Hult International Business SchoolLakshmi VenugopalNo ratings yet

- Quiz - Midterm ExaminationDocument21 pagesQuiz - Midterm Examinationangel caoNo ratings yet

- KrazyBee Services Private LimitedDocument9 pagesKrazyBee Services Private LimitedBalakrishnan IyerNo ratings yet

- Tutorial Chapter 6 - Sol.Document6 pagesTutorial Chapter 6 - Sol.Madina SuleimenovaNo ratings yet

- MBA Material ManagementDocument3 pagesMBA Material ManagementJNU100% (1)

- SM AklDocument318 pagesSM AklUsadhi33% (3)

- Mini Research SibusisiweDocument46 pagesMini Research SibusisiweKelvin ChikoweNo ratings yet

- ACCG 200 Week 8 Homework QuestionsDocument3 pagesACCG 200 Week 8 Homework QuestionsAlexander TrovatoNo ratings yet

- Place M M S MarcomDocument39 pagesPlace M M S MarcomThanhHoàiNguyễnNo ratings yet

- 2020 FA L4 To L10 StudentsDocument40 pages2020 FA L4 To L10 Students徐恺民No ratings yet

- Patanjali Vs BaidyanathDocument6 pagesPatanjali Vs BaidyanathHarsh Vardhan BajpaiNo ratings yet

- 304.C TS4FI 2021-New PDFDocument10 pages304.C TS4FI 2021-New PDFMayowa Adeniyi100% (2)

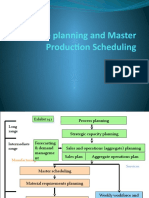

- Aggregate Planning and Master Production SchedulingDocument17 pagesAggregate Planning and Master Production SchedulingAshwani Singh100% (1)

- Significance of Amazing Selling Machine (ASM12)Document3 pagesSignificance of Amazing Selling Machine (ASM12)Tariqul Islam AyanNo ratings yet

- Media ClassificationDocument12 pagesMedia ClassificationRocky SyalNo ratings yet

- HafsaDocument11 pagesHafsaاحلام سعيدNo ratings yet

- Costing 57189426Document10 pagesCosting 57189426Zeeshan RahmanNo ratings yet

- Mayer Brown Net Asset Value Credit FacilitiesDocument5 pagesMayer Brown Net Asset Value Credit FacilitiesJose GoncalvesNo ratings yet

- Abercrombie & Fitch Co.: Investment ThesisDocument17 pagesAbercrombie & Fitch Co.: Investment ThesisFan SijingNo ratings yet

- Jepretan Layar 2023-09-27 Pada 10.49.00Document3 pagesJepretan Layar 2023-09-27 Pada 10.49.00Ardyannur DewaNo ratings yet

- IDX Annually 2016 Revisi PDFDocument158 pagesIDX Annually 2016 Revisi PDFFriedrick VecchioNo ratings yet

- quiz thầyDocument44 pagesquiz thầyThanh UyênNo ratings yet

- Marketing Plan - SiantechDocument47 pagesMarketing Plan - SiantechAhmed NasrNo ratings yet

- The Effect of Digital Marketing Strategy On Customer and Organizational OutcomesDocument11 pagesThe Effect of Digital Marketing Strategy On Customer and Organizational OutcomesOurpanNo ratings yet

- Chapter 1-5 Book 1Document42 pagesChapter 1-5 Book 1Krizel Dixie ParraNo ratings yet