You might also like

- Textbook of Urgent Care Management: Chapter 9, Insurance Requirements for the Urgent Care CenterFrom EverandTextbook of Urgent Care Management: Chapter 9, Insurance Requirements for the Urgent Care CenterNo ratings yet

- TÀI LIỆU -F8Document33 pagesTÀI LIỆU -F8Đoàn HoaNo ratings yet

- Assurance engagements and auditing standardsDocument16 pagesAssurance engagements and auditing standardsnerissa belloNo ratings yet

- Au Dit TinhDocument75 pagesAu Dit TinhTRINH DUC DIEPNo ratings yet

- The Five Rules for Successful Stock Investing: Morningstar's Guide to Building Wealth and Winning in the MarketFrom EverandThe Five Rules for Successful Stock Investing: Morningstar's Guide to Building Wealth and Winning in the MarketRating: 4 out of 5 stars4/5 (1)

- Assurance engagement elementsDocument17 pagesAssurance engagement elementsMandeep BashisthaNo ratings yet

- Audit Risk Alert: General Accounting and Auditing Developments, 2017/18From EverandAudit Risk Alert: General Accounting and Auditing Developments, 2017/18No ratings yet

- Audit and AssuranceDocument34 pagesAudit and AssuranceRidwan AhmedNo ratings yet

- Textbook of Urgent Care Management: Chapter 7, Exit Transactions: The Process of Selling an Urgent Care CenterFrom EverandTextbook of Urgent Care Management: Chapter 7, Exit Transactions: The Process of Selling an Urgent Care CenterNo ratings yet

- Baudprix SW1Document5 pagesBaudprix SW1KNo ratings yet

- Seatwork 1 AudtheoDocument6 pagesSeatwork 1 AudtheoHera Aster LudwigNo ratings yet

- Understanding Named, Automatic and Additional Insureds in the CGL PolicyFrom EverandUnderstanding Named, Automatic and Additional Insureds in the CGL PolicyNo ratings yet

- Operations Auditing Quiz 1Document6 pagesOperations Auditing Quiz 1cheni magsaelNo ratings yet

- TRẮC NGHIỆMDocument43 pagesTRẮC NGHIỆMNgọc Anh Nguyễn ThịNo ratings yet

- ACCA-Advance Audit & Assurance (AAA/P7) - MCQ's - Questions: A Passive Duty An Active DutyDocument8 pagesACCA-Advance Audit & Assurance (AAA/P7) - MCQ's - Questions: A Passive Duty An Active Dutybuls eyeNo ratings yet

- AtDocument14 pagesAtInny AginNo ratings yet

- Assurance Chapter-1 (28-06-2018)Document8 pagesAssurance Chapter-1 (28-06-2018)Shahid MahmudNo ratings yet

- The Financial Statement Audit ProcessDocument8 pagesThe Financial Statement Audit ProcessAngelica Mae MarquezNo ratings yet

- Assurance EngagementDocument19 pagesAssurance EngagementAbdulkarim Hamisi KufakunogaNo ratings yet

- ExerciseDocument30 pagesExerciseJosua PagcaliwaganNo ratings yet

- At Without AnswersDocument52 pagesAt Without AnswersJohn Rashid HebainaNo ratings yet

- Internal Auditing Assurance PrinciplesDocument5 pagesInternal Auditing Assurance PrinciplesJohn CPANo ratings yet

- Understanding Assurance EngagementsDocument3 pagesUnderstanding Assurance EngagementsRaven ChelseaNo ratings yet

- Aaa Topic 1Document8 pagesAaa Topic 1Cindy ClollyNo ratings yet

- Auditing Theory Fundamentals of Assurance Engagements (Multiple Choice Questions)Document15 pagesAuditing Theory Fundamentals of Assurance Engagements (Multiple Choice Questions)random17341No ratings yet

- Chapter - 01, Concept and Need For AssuranceDocument5 pagesChapter - 01, Concept and Need For Assurancemahbub khanNo ratings yet

- Business AssuranceDocument38 pagesBusiness AssuranceRAQIB 2025No ratings yet

- Acc12 - PrelimsDocument5 pagesAcc12 - PrelimsLuise MauieNo ratings yet

- 01 JournalDocument5 pages01 Journalits me keiNo ratings yet

- Topic 1 AaaDocument5 pagesTopic 1 AaaIsaac OsoroNo ratings yet

- Fundamentals of Auditing and Assurance ServicesDocument37 pagesFundamentals of Auditing and Assurance Servicesnicolebrixx100% (1)

- Auditing Contingent Liabilities and Subsequent EventsDocument13 pagesAuditing Contingent Liabilities and Subsequent Eventsh3swg6inl8wkNo ratings yet

- Fundamentals of Auditing and Assurance ServicesDocument34 pagesFundamentals of Auditing and Assurance ServicesPeter BanjaoNo ratings yet

- Introduction and Overview of Audit and Assurance: Chapter Learning ObjectivesDocument30 pagesIntroduction and Overview of Audit and Assurance: Chapter Learning ObjectivesTarro NguyenNo ratings yet

- Assurance Sample Paper 2017Document30 pagesAssurance Sample Paper 2017Lingeshwaren ChandramorganNo ratings yet

- Tareq Ahmed (Faisal) M.J.Abedin & CoDocument49 pagesTareq Ahmed (Faisal) M.J.Abedin & Cotusher pepolNo ratings yet

- Quiz AuditingDocument16 pagesQuiz AuditingCharlotte Canabang AmmadangNo ratings yet

- Principles of Auditing - Test No AnswerDocument40 pagesPrinciples of Auditing - Test No AnswerKatrina ChuaNo ratings yet

- Assurance Sample Paper 2016Document23 pagesAssurance Sample Paper 2016Lingeshwaren ChandramorganNo ratings yet

- AssuranceDocument39 pagesAssuranceLinh MaiNo ratings yet

- assuranceDocument12 pagesassuranceNga Nguyễn ThanhNo ratings yet

- AuditingDocument5 pagesAuditingZubaida AshrafNo ratings yet

- Test Bank - Assurance Principles (Cpar) LDocument56 pagesTest Bank - Assurance Principles (Cpar) Ljsus22100% (8)

- (UK) External AuditDocument6 pages(UK) External AuditDiana TuckerNo ratings yet

- Review of Philippine Standards on Quality Control, Auditing, Assurance and Related ServicesDocument56 pagesReview of Philippine Standards on Quality Control, Auditing, Assurance and Related Servicescherry padreNo ratings yet

- Chapter 6 AuditingDocument24 pagesChapter 6 AuditingMisshtaCNo ratings yet

- 4 JawapanDocument5 pages4 JawapanNad Adenan100% (1)

- Activity 1 - Fundamentals To Auditing and Assurance ServicesDocument14 pagesActivity 1 - Fundamentals To Auditing and Assurance ServicesRen100% (1)

- Module #01 - Fundamentals of Assurance ServicesDocument7 pagesModule #01 - Fundamentals of Assurance ServicesRhesus UrbanoNo ratings yet

- Activity Worksheet 001Document4 pagesActivity Worksheet 001Pearl Isabelle SudarioNo ratings yet

- MCQ - Assurance ServicesDocument13 pagesMCQ - Assurance Servicesemc2_mcv67% (30)

- Philippine Framework For Assurance EngagementsDocument12 pagesPhilippine Framework For Assurance Engagementsjamaira haridNo ratings yet

- MCQ-for lecture-QUIZ REVISED-QUESTIONS For StudentsDocument6 pagesMCQ-for lecture-QUIZ REVISED-QUESTIONS For Studentstinesa ambikapathyNo ratings yet

- CH 01Document16 pagesCH 01rajeshaisdu009No ratings yet

- Auditing ReviewerDocument3 pagesAuditing ReviewerDave ManaloNo ratings yet

- Auditing Theory - Overview of The Audit Process With AnswersDocument44 pagesAuditing Theory - Overview of The Audit Process With AnswersShielle Azon90% (30)

- Chapter 1 Introduction To Assurance Engagements - PPT 1704069091Document70 pagesChapter 1 Introduction To Assurance Engagements - PPT 1704069091Clar Aaron Bautista100% (1)

- AUDITINGDocument11 pagesAUDITINGMaud Julie May FagyanNo ratings yet

- READING REPORT in Auditing and Assurance Concepts and ApplicationDocument3 pagesREADING REPORT in Auditing and Assurance Concepts and Applicationhazel alvarezNo ratings yet

- Auditing S1 - Chapter 1Document12 pagesAuditing S1 - Chapter 1p aloaNo ratings yet

- Auditing Ethics Full Test 1 May 2024 Test Paper 1703329935Document22 pagesAuditing Ethics Full Test 1 May 2024 Test Paper 1703329935hersheyys4No ratings yet

- Psa 600Document9 pagesPsa 600Bhebi Dela CruzNo ratings yet

- Adoption Status of BFRS, BAS, BSADocument7 pagesAdoption Status of BFRS, BAS, BSAAl RajeeNo ratings yet

- CaplinPoint Q3FY22Document45 pagesCaplinPoint Q3FY22Ranjan PrakashNo ratings yet

- UntitledDocument48 pagesUntitledKausar FirdousNo ratings yet

- Final PPT Compliance Audit P K Jain 20210415102658Document67 pagesFinal PPT Compliance Audit P K Jain 20210415102658Pratik Sharma100% (1)

- Financials-Bank Asia 2017Document134 pagesFinancials-Bank Asia 2017SA023No ratings yet

- Standard Unmodified Auditor ReportDocument3 pagesStandard Unmodified Auditor ReportRiz WanNo ratings yet

- Forming Auditor Opinion and Reporting RequirementsDocument8 pagesForming Auditor Opinion and Reporting RequirementsAdzNo ratings yet

- 2 Philippine - Standards - On - AuditingDocument12 pages2 Philippine - Standards - On - AuditingyuliNo ratings yet

- Does the CAG exceed its legal powers in auditing government companiesDocument4 pagesDoes the CAG exceed its legal powers in auditing government companiesNisha ChanchlaniNo ratings yet

- ISO 9001:2015 CS 9 Raising NC - 2017Document5 pagesISO 9001:2015 CS 9 Raising NC - 2017YasirdzNo ratings yet

- Effects of Corporate Governance Characteristics On Audit Report LagsDocument6 pagesEffects of Corporate Governance Characteristics On Audit Report LagsBayu SayNo ratings yet

- Mao Caro by Prafful BhaleraoDocument9 pagesMao Caro by Prafful BhaleraoSonu BhaleraoNo ratings yet

- Chapter 1 SlidesDocument19 pagesChapter 1 Slidesazade azamiNo ratings yet

- Auditing Desktop Itud1j8Document59 pagesAuditing Desktop Itud1j8Cici homeNo ratings yet

- IPCC Audit MCQs by Vinit Mishra Sir PDFDocument125 pagesIPCC Audit MCQs by Vinit Mishra Sir PDFPrakash Gaurav100% (3)

- Assurance Question Bank 2019Document193 pagesAssurance Question Bank 2019Md. Shafiqul Islam0% (1)

- 5 Published Company AccountsDocument27 pages5 Published Company Accountsking brothersNo ratings yet

- S Chand and Company LimitedDocument21 pagesS Chand and Company LimitedNishit GolchhaNo ratings yet

- Chapter 5Document56 pagesChapter 5lyj1017100% (1)

- Project On Audit of BankDocument71 pagesProject On Audit of BankSimran Sachdev0% (2)

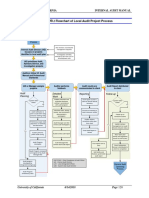

- 6000 Appendix 6000.: 2 Flowchart of Local Audit Project ProcessDocument1 page6000 Appendix 6000.: 2 Flowchart of Local Audit Project ProcessNiken RindasariNo ratings yet

- Final Foreign CaseDocument24 pagesFinal Foreign CaseBoaz SorianoNo ratings yet

- ACCA P7 Workbook Q&A InsightsDocument80 pagesACCA P7 Workbook Q&A InsightsLorena BallaNo ratings yet

- Internal Audit Manual - v4.1 - 27 Nov 2012 PDFDocument57 pagesInternal Audit Manual - v4.1 - 27 Nov 2012 PDFJi YuNo ratings yet

- Audit Working Papers and Programs GuideDocument45 pagesAudit Working Papers and Programs Guidelj gazzinganNo ratings yet

- The First Minute: How to start conversations that get resultsFrom EverandThe First Minute: How to start conversations that get resultsRating: 4.5 out of 5 stars4.5/5 (57)

- The Coaching Habit: Say Less, Ask More & Change the Way You Lead ForeverFrom EverandThe Coaching Habit: Say Less, Ask More & Change the Way You Lead ForeverRating: 4.5 out of 5 stars4.5/5 (186)

- Spark: How to Lead Yourself and Others to Greater SuccessFrom EverandSpark: How to Lead Yourself and Others to Greater SuccessRating: 4.5 out of 5 stars4.5/5 (131)

- How to Lead: Wisdom from the World's Greatest CEOs, Founders, and Game ChangersFrom EverandHow to Lead: Wisdom from the World's Greatest CEOs, Founders, and Game ChangersRating: 4.5 out of 5 stars4.5/5 (95)

- Work the System: The Simple Mechanics of Making More and Working Less (4th Edition)From EverandWork the System: The Simple Mechanics of Making More and Working Less (4th Edition)Rating: 4.5 out of 5 stars4.5/5 (23)

- Transformed: Moving to the Product Operating ModelFrom EverandTransformed: Moving to the Product Operating ModelRating: 4 out of 5 stars4/5 (1)

- How to Talk to Anyone at Work: 72 Little Tricks for Big Success Communicating on the JobFrom EverandHow to Talk to Anyone at Work: 72 Little Tricks for Big Success Communicating on the JobRating: 4.5 out of 5 stars4.5/5 (36)

- Billion Dollar Lessons: What You Can Learn from the Most Inexcusable Business Failures of the Last Twenty-five YearsFrom EverandBillion Dollar Lessons: What You Can Learn from the Most Inexcusable Business Failures of the Last Twenty-five YearsRating: 4.5 out of 5 stars4.5/5 (52)

- Transformed: Moving to the Product Operating ModelFrom EverandTransformed: Moving to the Product Operating ModelRating: 4 out of 5 stars4/5 (1)

- The 12 Week Year: Get More Done in 12 Weeks than Others Do in 12 MonthsFrom EverandThe 12 Week Year: Get More Done in 12 Weeks than Others Do in 12 MonthsRating: 4.5 out of 5 stars4.5/5 (411)

- Scaling Up: How a Few Companies Make It...and Why the Rest Don't, Rockefeller Habits 2.0From EverandScaling Up: How a Few Companies Make It...and Why the Rest Don't, Rockefeller Habits 2.0Rating: 5 out of 5 stars5/5 (1)

- The 7 Habits of Highly Effective PeopleFrom EverandThe 7 Habits of Highly Effective PeopleRating: 4 out of 5 stars4/5 (2564)

- The E-Myth Revisited: Why Most Small Businesses Don't Work andFrom EverandThe E-Myth Revisited: Why Most Small Businesses Don't Work andRating: 4.5 out of 5 stars4.5/5 (709)

- Unlocking Potential: 7 Coaching Skills That Transform Individuals, Teams, & OrganizationsFrom EverandUnlocking Potential: 7 Coaching Skills That Transform Individuals, Teams, & OrganizationsRating: 4.5 out of 5 stars4.5/5 (28)

- The Friction Project: How Smart Leaders Make the Right Things Easier and the Wrong Things HarderFrom EverandThe Friction Project: How Smart Leaders Make the Right Things Easier and the Wrong Things HarderNo ratings yet

- How the World Sees You: Discover Your Highest Value Through the Science of FascinationFrom EverandHow the World Sees You: Discover Your Highest Value Through the Science of FascinationRating: 4 out of 5 stars4/5 (7)

- Work Stronger: Habits for More Energy, Less Stress, and Higher Performance at WorkFrom EverandWork Stronger: Habits for More Energy, Less Stress, and Higher Performance at WorkRating: 4.5 out of 5 stars4.5/5 (12)

- Elevate: The Three Disciplines of Advanced Strategic ThinkingFrom EverandElevate: The Three Disciplines of Advanced Strategic ThinkingRating: 4.5 out of 5 stars4.5/5 (3)

- The 4 Disciplines of Execution: Revised and Updated: Achieving Your Wildly Important GoalsFrom EverandThe 4 Disciplines of Execution: Revised and Updated: Achieving Your Wildly Important GoalsRating: 4.5 out of 5 stars4.5/5 (48)

- 300+ PMP Practice Questions Aligned with PMBOK 7, Agile Methods, and Key Process Groups - 2024: First EditionFrom Everand300+ PMP Practice Questions Aligned with PMBOK 7, Agile Methods, and Key Process Groups - 2024: First EditionNo ratings yet

- 7 Principles of Transformational Leadership: Create a Mindset of Passion, Innovation, and GrowthFrom Everand7 Principles of Transformational Leadership: Create a Mindset of Passion, Innovation, and GrowthRating: 5 out of 5 stars5/5 (51)

- Radical Candor by Kim Scott - Book Summary: Be A Kickass Boss Without Losing Your HumanityFrom EverandRadical Candor by Kim Scott - Book Summary: Be A Kickass Boss Without Losing Your HumanityRating: 4.5 out of 5 stars4.5/5 (40)

- The 12 Week Year: Get More Done in 12 Weeks than Others Do in 12 MonthsFrom EverandThe 12 Week Year: Get More Done in 12 Weeks than Others Do in 12 MonthsRating: 4.5 out of 5 stars4.5/5 (90)

- Agile: The Insights You Need from Harvard Business ReviewFrom EverandAgile: The Insights You Need from Harvard Business ReviewRating: 4.5 out of 5 stars4.5/5 (34)

- The Lean Product Playbook: How to Innovate with Minimum Viable Products and Rapid Customer FeedbackFrom EverandThe Lean Product Playbook: How to Innovate with Minimum Viable Products and Rapid Customer FeedbackRating: 4.5 out of 5 stars4.5/5 (81)

- Difficult Conversations: Craft a Clear Message, Manage Emotions and Focus on a SolutionFrom EverandDifficult Conversations: Craft a Clear Message, Manage Emotions and Focus on a SolutionRating: 4 out of 5 stars4/5 (3)