You might also like

- Demand - Exam Practice 7Document5 pagesDemand - Exam Practice 7Leah BrocklebankNo ratings yet

- Test Bank - Financial Accounting and Reporting Theory (Volume 1, 2 and 3)Document17 pagesTest Bank - Financial Accounting and Reporting Theory (Volume 1, 2 and 3)Kimberly Etulle Celona100% (1)

- Tax Treatment of GiftsDocument18 pagesTax Treatment of GiftsM H MullaNo ratings yet

- Tax Treatment of GiftsDocument17 pagesTax Treatment of Giftssreyans banthiaNo ratings yet

- Tax Treatment of GiftsDocument16 pagesTax Treatment of GiftsGokul NairNo ratings yet

- The Tax Treatment of Sum of Money Received As Gift Under Section 56Document4 pagesThe Tax Treatment of Sum of Money Received As Gift Under Section 56Anshu kumarNo ratings yet

- Tax Would Be Levied On Such Gifts. The Persons Who Constitute Relatives For ThisDocument2 pagesTax Would Be Levied On Such Gifts. The Persons Who Constitute Relatives For ThisSavoir PenNo ratings yet

- Taxability of GiftDocument9 pagesTaxability of GiftGaurav BeniwalNo ratings yet

- Understanding The Provisions of Section 56 (2) (X)Document5 pagesUnderstanding The Provisions of Section 56 (2) (X)kavi priyaNo ratings yet

- Gift - Def of RelativeDocument1 pageGift - Def of RelativeAshish JainNo ratings yet

- Receive A Gift From RelatiDocument2 pagesReceive A Gift From Relatinagaraj.winNo ratings yet

- Accept Gift and Pay TaxDocument2 pagesAccept Gift and Pay TaxSantosh ParasharNo ratings yet

- Assignment - Explain Income From Other SourcesDocument9 pagesAssignment - Explain Income From Other SourcesPraveen SNo ratings yet

- Vivos Based On Pure Act of Liberality Without Any or Less Than Adequate Consideration and Without AnyDocument5 pagesVivos Based On Pure Act of Liberality Without Any or Less Than Adequate Consideration and Without AnyJunivenReyUmadhayNo ratings yet

- TDS Stands For Tax Deducted at SourceDocument6 pagesTDS Stands For Tax Deducted at Sourcesaurabh dixitNo ratings yet

- Taxation: Wealth Tax and Gift TaxDocument10 pagesTaxation: Wealth Tax and Gift TaxharshitaNo ratings yet

- Taxability of Gift Tax - TLK - 2022Document10 pagesTaxability of Gift Tax - TLK - 2022varaxiy659No ratings yet

- Tax Free in Case of Other SourcesDocument4 pagesTax Free in Case of Other SourcesAnshul TyagiNo ratings yet

- Section 56 - Decoding Section 56 of The Income-Tax Act, 1961 (ITDocument5 pagesSection 56 - Decoding Section 56 of The Income-Tax Act, 1961 (ITNavyaNo ratings yet

- Module 2Document22 pagesModule 2Suryansh Kumar AroraNo ratings yet

- TaxationDocument31 pagesTaxationdaljeet singhNo ratings yet

- Corporate Taxation IntroductionDocument48 pagesCorporate Taxation IntroductionSatyajeet MohantyNo ratings yet

- Income Tax Unit 1Document44 pagesIncome Tax Unit 1Abhishek BhatiaNo ratings yet

- Unit 1Document35 pagesUnit 1Monika SaxenaNo ratings yet

- Income TaxDocument3 pagesIncome TaxGopika RaveendranNo ratings yet

- Income From Other SourcesDocument16 pagesIncome From Other SourcesSarvar PathanNo ratings yet

- Deemed Income Under Income Tax Act, 1961.: Extended Definition of IncomeDocument5 pagesDeemed Income Under Income Tax Act, 1961.: Extended Definition of IncomeVaibhav GuptaNo ratings yet

- Unit 1 ItlaDocument11 pagesUnit 1 ItlaAbdul basitNo ratings yet

- Tax Unit 2Document63 pagesTax Unit 2sunaina aliNo ratings yet

- Income TaxDocument12 pagesIncome TaxArvind RioNo ratings yet

- "Income From Other Sources": Faculty of Law Jamia Millia IslamiaDocument20 pages"Income From Other Sources": Faculty of Law Jamia Millia IslamiaABNo ratings yet

- Chapter 4 - Income From Other SourcesDocument23 pagesChapter 4 - Income From Other SourcesPuran GuptaNo ratings yet

- Income From Other Sources - NotesDocument4 pagesIncome From Other Sources - NotesAniket AgrawalNo ratings yet

- Name-Saif Ali Class - B.A LLB (6 Semester) Topic - Income From Other Persons Included in Assessee'S Total Income ROLL NO. - 43Document8 pagesName-Saif Ali Class - B.A LLB (6 Semester) Topic - Income From Other Persons Included in Assessee'S Total Income ROLL NO. - 43Saif AliNo ratings yet

- Name-Saif Ali Class - B.A LLB (6 Semester) Topic - Income From Other Persons Included in Assessee'S Total Income ROLL NO. - 43Document8 pagesName-Saif Ali Class - B.A LLB (6 Semester) Topic - Income From Other Persons Included in Assessee'S Total Income ROLL NO. - 43Saif AliNo ratings yet

- Assignmnt IIDocument6 pagesAssignmnt IIJeremy RemlalfakaNo ratings yet

- Income From Other SourcesDocument17 pagesIncome From Other Sourcesrakhee dewanNo ratings yet

- Module 1 Lesson 5Document6 pagesModule 1 Lesson 5Rich Ann Redondo VillanuevaNo ratings yet

- Clubbing of Income: Objective - Main Objectives Are As FollowsDocument8 pagesClubbing of Income: Objective - Main Objectives Are As FollowsVishnu VarthanNo ratings yet

- Topic:-Clubbing of Incomes and Aggregation of IncomesDocument31 pagesTopic:-Clubbing of Incomes and Aggregation of IncomesmaanikyanNo ratings yet

- GiftDocument8 pagesGiftsagar kukrejaNo ratings yet

- Incomes Which Do Not Form OF Total Income (Section 10) : Dr. P.Sree Sudha, Associate Professor, DsnluDocument48 pagesIncomes Which Do Not Form OF Total Income (Section 10) : Dr. P.Sree Sudha, Associate Professor, Dsnluleela naga janaki rajitha attiliNo ratings yet

- Module-1: Basic Concepts and DefinitionsDocument35 pagesModule-1: Basic Concepts and Definitions2VX20BA091No ratings yet

- cLUBBING OF iNCOMEDocument18 pagescLUBBING OF iNCOMEDipinderNo ratings yet

- Income From Other Sources - Ay0910Document41 pagesIncome From Other Sources - Ay0910ravibavaria5913No ratings yet

- Clubbing of Income 1Document15 pagesClubbing of Income 1Shyla PillaiNo ratings yet

- Section 56 - Decoding Section 56 of The Income-Tax Act, 1961 (ITDocument6 pagesSection 56 - Decoding Section 56 of The Income-Tax Act, 1961 (ITNavyaNo ratings yet

- Chapter 2 - Donor's Tax (Notes)Document8 pagesChapter 2 - Donor's Tax (Notes)Angela Denisse FranciscoNo ratings yet

- Condonation or Cancellation of IndebtednessDocument4 pagesCondonation or Cancellation of IndebtednessArceño, Advrelyn Frances C.No ratings yet

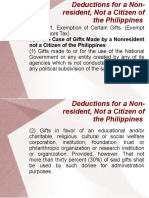

- B) in The Case of Gifts Made by A Nonresident Not A Citizen of The PhilippinesDocument23 pagesB) in The Case of Gifts Made by A Nonresident Not A Citizen of The PhilippinesNissi JonnaNo ratings yet

- Bba Income TaxDocument156 pagesBba Income TaxSalman Ansari100% (1)

- Donor's TaxDocument25 pagesDonor's TaxMark Erick Acojido RetonelNo ratings yet

- Income Tax Short Notes For C S C A C M A Exam 2014Document43 pagesIncome Tax Short Notes For C S C A C M A Exam 2014Jolly SinghalNo ratings yet

- Unit IDocument7 pagesUnit IMonuNo ratings yet

- It'S Matter of Law and WelfareDocument36 pagesIt'S Matter of Law and WelfareAwinash ChowdaryNo ratings yet

- Tax Law Final PDFDocument27 pagesTax Law Final PDFhalaNo ratings yet

- Govern The Imposition of The Donor's TaxDocument5 pagesGovern The Imposition of The Donor's TaxjuliNo ratings yet

- UNIT-1 Basic Concepts of Income TaxDocument38 pagesUNIT-1 Basic Concepts of Income TaxGarimaNo ratings yet

- Income Tax IntroductionDocument36 pagesIncome Tax IntroductionAnonymous yXJnZMt71% (7)

- Income TaxDocument51 pagesIncome TaxInternet 223No ratings yet

- Sponsorship: Who's Eligible & How to ApplyFrom EverandSponsorship: Who's Eligible & How to ApplyNo ratings yet

- TA Chapter 7 PDFDocument29 pagesTA Chapter 7 PDFMutia WardaniNo ratings yet

- Fa4 Prelim Exercises 1 Fa4 Current - LiabilitiesDocument6 pagesFa4 Prelim Exercises 1 Fa4 Current - LiabilitiesatashajaylevelasquezNo ratings yet

- Income Tax Law & Practice: Unit 1Document30 pagesIncome Tax Law & Practice: Unit 1jaspreet kaurNo ratings yet

- Answer Problem Non Vat 1Document14 pagesAnswer Problem Non Vat 1Angel Frolen B. RacinezNo ratings yet

- Multiple Choice Partnership and CorporationDocument14 pagesMultiple Choice Partnership and CorporationTrina Joy HomerezNo ratings yet

- 3tcpe Taaot: HRTRDRDocument1 page3tcpe Taaot: HRTRDRSuresh VadlamudiNo ratings yet

- Impact of New Housing Units On Existing Rents 090120Document57 pagesImpact of New Housing Units On Existing Rents 090120pkrysl2384No ratings yet

- Cockshutt & Cottrell - Towards A New SocialismDocument208 pagesCockshutt & Cottrell - Towards A New Socialismmichael4t100% (2)

- Declaration For 206AB 206CCA 4 1 1 2 1 2Document1 pageDeclaration For 206AB 206CCA 4 1 1 2 1 2Khalid ShaikhNo ratings yet

- Economics 1 Bridging Study Guide Part 3Document118 pagesEconomics 1 Bridging Study Guide Part 3Roger LinNo ratings yet

- Lesson 2 Sources of Family IncomeDocument22 pagesLesson 2 Sources of Family Incomeroel mabbayad83% (6)

- WRLODocument31 pagesWRLOshailendra369No ratings yet

- UnauditedDocument30 pagesUnauditedSanjay KumarNo ratings yet

- Economic ModelDocument2 pagesEconomic ModelAnand SinghNo ratings yet

- BOI Interim Report 2019 PDFDocument122 pagesBOI Interim Report 2019 PDFAditya MukherjeeNo ratings yet

- IND AS 20 - Bhavik Chokshi - FR ShieldDocument7 pagesIND AS 20 - Bhavik Chokshi - FR ShieldSoham Upadhyay100% (1)

- Project: Prepare A Worksheet, Financial Statements, and Adjusting and Closing Entries (15 Marks)Document5 pagesProject: Prepare A Worksheet, Financial Statements, and Adjusting and Closing Entries (15 Marks)jonialbadri1000No ratings yet

- LeasesDocument1 pageLeasesIm NayeonNo ratings yet

- 02 Profits, Cash Flows and Taxes - StudentsDocument25 pages02 Profits, Cash Flows and Taxes - StudentslmsmNo ratings yet

- Interpretation of StatueDocument4 pagesInterpretation of StatueYasir KhanNo ratings yet

- The Accounting Cycle: Accruals and DeferralsDocument52 pagesThe Accounting Cycle: Accruals and Deferralszahraa aabedNo ratings yet

- 1 Income From PGBPDocument20 pages1 Income From PGBPalex v.m.No ratings yet

- Module 4 - ConsumptionDocument21 pagesModule 4 - ConsumptionllanahbayugaoNo ratings yet

- 2421 Sports Equipment Manufacturing in China Industry ReportDocument37 pages2421 Sports Equipment Manufacturing in China Industry ReportIon NyegreNo ratings yet

- Receipt of House Rent Free Doc Format TemplateDocument6 pagesReceipt of House Rent Free Doc Format Templateparag0019No ratings yet

- OCTOBER 2021: PT. Shopee Internasional IndonesiaDocument1 pageOCTOBER 2021: PT. Shopee Internasional IndonesiaRifka FitrotuzzakiaNo ratings yet

- Practice Exam Chapters 1-5 (1) Solutions: Problem IDocument5 pagesPractice Exam Chapters 1-5 (1) Solutions: Problem IAtif RehmanNo ratings yet

- Cor Jesu College Sacred Heart Avenue Digos City: Business PlanDocument19 pagesCor Jesu College Sacred Heart Avenue Digos City: Business PlanFatima ChinNo ratings yet