You might also like

- Sandy Gill ProjectDocument67 pagesSandy Gill ProjectSandy Gill GillNo ratings yet

- Comparison of Ind As and IFRSDocument10 pagesComparison of Ind As and IFRSAman SinghNo ratings yet

- Technical ReleaseDocument35 pagesTechnical ReleasezilchhourNo ratings yet

- The Language of Business Is Changing: Do You Understand/speak IFRS?Document22 pagesThe Language of Business Is Changing: Do You Understand/speak IFRS?vinit.ambat13510No ratings yet

- Ke Quoc TeDocument1 pageKe Quoc TeAn TrịnhNo ratings yet

- Benefits Associated With Implementation of IFRSDocument8 pagesBenefits Associated With Implementation of IFRSchinkijsrNo ratings yet

- Accounting StandardsDocument22 pagesAccounting Standardsdodiyavijay25691No ratings yet

- IFRS in IndiaDocument6 pagesIFRS in IndiaAnil ChauhanNo ratings yet

- Ifrs 170120102142Document10 pagesIfrs 170120102142ajayNo ratings yet

- Merits of IFRSDocument3 pagesMerits of IFRSashish.nairNo ratings yet

- ACC 430 Exam 2 Answer KeyDocument2 pagesACC 430 Exam 2 Answer KeyShannonNo ratings yet

- Final Assignment 505Document36 pagesFinal Assignment 505PRINCESS PlayZNo ratings yet

- Ifrs in IndiaDocument6 pagesIfrs in IndiaPuneesh SachdevaNo ratings yet

- Ias MergedDocument157 pagesIas MergedAnalou LopezNo ratings yet

- IFRS BasicsDocument8 pagesIFRS BasicsgeorgebabycNo ratings yet

- IFRS Conversion ServicesDocument2 pagesIFRS Conversion ServicesParas MittalNo ratings yet

- Assignment - Ankit Singh BBA (P) 2Document19 pagesAssignment - Ankit Singh BBA (P) 2Rahul SinghNo ratings yet

- Advantages and Disadvantages of IFRSDocument2 pagesAdvantages and Disadvantages of IFRSraylan02300No ratings yet

- 1478-8225-Aftermaths of IFRS CCCDocument25 pages1478-8225-Aftermaths of IFRS CCCsincereboy5No ratings yet

- The Chartered Institute of Taxation of Nigeria (CITN)Document48 pagesThe Chartered Institute of Taxation of Nigeria (CITN)Fred OnyemenamNo ratings yet

- Accounting Standards in PakistanDocument17 pagesAccounting Standards in PakistanMuneeb AliNo ratings yet

- Chapter 1Document79 pagesChapter 1alemu desta100% (1)

- ch6 IFRSDocument56 pagesch6 IFRSAnonymous 6aW7sZWdILNo ratings yet

- International Financial Reporting Standards (IFRS)Document74 pagesInternational Financial Reporting Standards (IFRS)Ashutosh GuptaNo ratings yet

- Contemporary Issues - IFRS, HR, CSR EtcDocument38 pagesContemporary Issues - IFRS, HR, CSR Etckaltim.iu.m.ma.h78No ratings yet

- IFRS-Basic Principles, Assumptions, Importance, Advantages and DisadvantagesDocument32 pagesIFRS-Basic Principles, Assumptions, Importance, Advantages and DisadvantagesPRINCESS PlayZNo ratings yet

- IFRS1Document33 pagesIFRS1Ejiemen OkunegaNo ratings yet

- Financial Reporting Case 3Document3 pagesFinancial Reporting Case 3HUPGUIDAN, GAUDENCIANo ratings yet

- The Iasb at A CrossroadDocument8 pagesThe Iasb at A Crossroadyahya zafarNo ratings yet

- 1 CAPE The Nature and Scope of Financial Accounting 2018 SDocument6 pages1 CAPE The Nature and Scope of Financial Accounting 2018 SNIS TTNo ratings yet

- Conceptual Framework of AccountingDocument32 pagesConceptual Framework of AccountingGiaNo ratings yet

- Assignment Intermediate Accounting CH 123Document5 pagesAssignment Intermediate Accounting CH 123NELVA QABLINANo ratings yet

- 5 SEM BCOM - International Financial Reporting StandardsDocument49 pages5 SEM BCOM - International Financial Reporting StandardsMadhu kumarNo ratings yet

- International Financial Reporting Standards (Ifrs) : Presented By, Siva Priyanka Vamshidhar Reddy Manasa ReddyDocument16 pagesInternational Financial Reporting Standards (Ifrs) : Presented By, Siva Priyanka Vamshidhar Reddy Manasa ReddyVamshidhar ReddyNo ratings yet

- Introduction To IFRSDocument13 pagesIntroduction To IFRSgovindsekharNo ratings yet

- IfrsDocument20 pagesIfrsarchana_anuragi100% (3)

- IFRSDocument14 pagesIFRSNishchay Dhingra100% (1)

- Adv. Accountancy Paper-1Document5 pagesAdv. Accountancy Paper-1Avadhut PaymalleNo ratings yet

- Business FinanceDocument13 pagesBusiness FinanceMichael MendozaNo ratings yet

- IFRS BhamineeDocument4 pagesIFRS BhamineeBhaminee patelNo ratings yet

- IFRS - Road To ConversionDocument29 pagesIFRS - Road To ConversionAnggiMarpaungNo ratings yet

- Ifrs Indian ContextDocument7 pagesIfrs Indian ContextKumar Sachin DeoNo ratings yet

- Unit 01 (8553)Document30 pagesUnit 01 (8553)naseer ahmedNo ratings yet

- AfmDocument15 pagesAfmabcd dcbaNo ratings yet

- International Financial Reporting StandardsDocument12 pagesInternational Financial Reporting StandardsViraja GuruNo ratings yet

- Presentation-Financial Reporting-I: Master of Commerce Semister 4, Fr-I Presentation, Presenting On September 13, 2019Document12 pagesPresentation-Financial Reporting-I: Master of Commerce Semister 4, Fr-I Presentation, Presenting On September 13, 2019gohar sheraziNo ratings yet

- Covergence of Ifrs With Indian GaapDocument15 pagesCovergence of Ifrs With Indian GaappripandeyNo ratings yet

- Ifrs Research Paper TopicsDocument5 pagesIfrs Research Paper Topicscam1hesa100% (1)

- Accounting Standards (Satyanath Mohapatra)Document39 pagesAccounting Standards (Satyanath Mohapatra)smrutiranjan swain100% (1)

- What Is IFRSDocument8 pagesWhat Is IFRSRagvi BaluNo ratings yet

- Accounting Under IFRS RegulationDocument4 pagesAccounting Under IFRS Regulationlukas.zmatlikNo ratings yet

- IFRSDocument20 pagesIFRSShilpi Jain0% (1)

- Accounting Standard-1 and Its Legal Implications in The Corporate WorldDocument32 pagesAccounting Standard-1 and Its Legal Implications in The Corporate Worldlove_djNo ratings yet

- Scrip Midterm AccountingDocument8 pagesScrip Midterm AccountingThanh MaiNo ratings yet

- Us Assurance International Financial Reporting STD 030108Document4 pagesUs Assurance International Financial Reporting STD 030108Pallavi PalluNo ratings yet

- Ifrs As A Tool For Cross Border Reporting ImzakariDocument27 pagesIfrs As A Tool For Cross Border Reporting ImzakariBayodele7No ratings yet

- The Convergence To IFRS - Reasons, Implications, Applicability, and ConcernsDocument10 pagesThe Convergence To IFRS - Reasons, Implications, Applicability, and ConcernsRajipah OsmanNo ratings yet

- International Financial Statement AnalysisFrom EverandInternational Financial Statement AnalysisRating: 1 out of 5 stars1/5 (1)

- IFRS Simplified: A fast and easy-to-understand overview of the new International Financial Reporting StandardsFrom EverandIFRS Simplified: A fast and easy-to-understand overview of the new International Financial Reporting StandardsRating: 4 out of 5 stars4/5 (11)

- True or FalseDocument1 pageTrue or FalseStela Marie CarandangNo ratings yet

- Soalan AccaDocument4 pagesSoalan AccaBhutan ChayNo ratings yet

- CFI Holdings H1 2013 Results PDFDocument2 pagesCFI Holdings H1 2013 Results PDFKristi DuranNo ratings yet

- Ifrs 3 Business CombinationsDocument11 pagesIfrs 3 Business CombinationsEshetieNo ratings yet

- ACCO 20063 - Conceptual Framework and Accounting StandardsDocument21 pagesACCO 20063 - Conceptual Framework and Accounting StandardsSarmiento Rona A.No ratings yet

- CPA Compilation ReportDocument2 pagesCPA Compilation ReportMike YaunaNo ratings yet

- Novartis Annual Report 2018 enDocument337 pagesNovartis Annual Report 2018 enNyah Graze G. HuevosNo ratings yet

- Ahenkye Pasco Accounting 1 and 2 Notes and Solved Past QuestionsDocument208 pagesAhenkye Pasco Accounting 1 and 2 Notes and Solved Past QuestionspeterokotettehNo ratings yet

- Globe Reflection aCyFaR1 AWItDocument9 pagesGlobe Reflection aCyFaR1 AWIt123r12f1No ratings yet

- Forensic Accounting and Fraud Investigation A Language of The Court of Law To Resolve Anticipated DisputesDocument6 pagesForensic Accounting and Fraud Investigation A Language of The Court of Law To Resolve Anticipated DisputesInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Deferred TaxationDocument20 pagesDeferred TaxationayyazmNo ratings yet

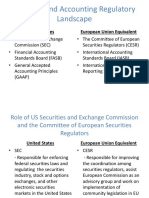

- Financial and Accounting Regulatory LandscapeDocument7 pagesFinancial and Accounting Regulatory LandscapeDiana Mindru StrenerNo ratings yet

- Accounting ConventionsDocument16 pagesAccounting ConventionsDishank Baid100% (1)

- Tabassum Butt - ACCADocument4 pagesTabassum Butt - ACCAcdeekyNo ratings yet

- Standards B: Forming An Opinion and Reporting On Financial StatementsDocument35 pagesStandards B: Forming An Opinion and Reporting On Financial StatementsnikNo ratings yet

- Investor Presentation: March 2017Document32 pagesInvestor Presentation: March 2017Jenny QuachNo ratings yet

- Conceptual Framework - Discussion Exercises For PrintDocument17 pagesConceptual Framework - Discussion Exercises For PrintFrancine Thea M. LantayaNo ratings yet

- Bachelor of Science (Honours) : Accounting Accounting and FinanceDocument12 pagesBachelor of Science (Honours) : Accounting Accounting and FinanceBryan SingNo ratings yet

- AFAR1 Main Exam Q (Feb 2022)Document5 pagesAFAR1 Main Exam Q (Feb 2022)Alice LowNo ratings yet

- Fielmann Report 2013Document132 pagesFielmann Report 2013Alexandru GheorgheNo ratings yet

- Baf Sem 5Document8 pagesBaf Sem 5api-292680897No ratings yet

- 20190831041657SLCHIA005FR1 Intro To FRDocument113 pages20190831041657SLCHIA005FR1 Intro To FRNadiaIssabellaNo ratings yet

- MCB - Standlaone Accounts 2007Document83 pagesMCB - Standlaone Accounts 2007usmankhan9No ratings yet

- Mcom Cbcs LatestDocument45 pagesMcom Cbcs Latestanoopsingh19992010No ratings yet

- Akpri - Impact of Hierarchy InformationDocument18 pagesAkpri - Impact of Hierarchy InformationGungis PramanaNo ratings yet

- Applying IFRS 3 in Accounting For Business Acquisitions: - A Case StudyDocument70 pagesApplying IFRS 3 in Accounting For Business Acquisitions: - A Case Studysalehin1969No ratings yet

- University of Lagos: Akoka Yaba School of Postgraduate Studies PART TIME 2017/2018 SESSIONDocument5 pagesUniversity of Lagos: Akoka Yaba School of Postgraduate Studies PART TIME 2017/2018 SESSIONDavid OparindeNo ratings yet

- Certifr Questions BankDocument86 pagesCertifr Questions BankysalamonyNo ratings yet

- Online Learning Module ACCT 1026 (Financial Accounting and Reporting)Document7 pagesOnline Learning Module ACCT 1026 (Financial Accounting and Reporting)Annie RapanutNo ratings yet

- Master Thesis PP88092Document70 pagesMaster Thesis PP88092Aeson Dela CruzNo ratings yet