You might also like

- Breaking Bad Habits and Improving Your LifeFrom EverandBreaking Bad Habits and Improving Your LifeRating: 4 out of 5 stars4/5 (3)

- Inscriptions 27 October2019Document37 pagesInscriptions 27 October2019Gopinath Radhakrishnan100% (3)

- Inscriptions 29 Apr 2020Document46 pagesInscriptions 29 Apr 2020Gopinath Radhakrishnan100% (4)

- Inscriptions 28 Jan 2020Document32 pagesInscriptions 28 Jan 2020Gopinath Radhakrishnan100% (6)

- Inscriptions 32 Jan2021Document35 pagesInscriptions 32 Jan2021Gopinath Radhakrishnan100% (2)

- Inscriptions 40 Jan2023Document42 pagesInscriptions 40 Jan2023Gopinath Radhakrishnan100% (1)

- Inscriptions 30 JULY2020Document41 pagesInscriptions 30 JULY2020Gopinath Radhakrishnan50% (4)

- Inscriptions 25Document41 pagesInscriptions 25Gopinath Radhakrishnan100% (12)

- Inscriptions 36 COVER PAGESDocument22 pagesInscriptions 36 COVER PAGESGopinath RadhakrishnanNo ratings yet

- Inscriptions 2Document22 pagesInscriptions 2Gopinath Radhakrishnan100% (1)

- Inscriptions 31 October 2020Document49 pagesInscriptions 31 October 2020Gopinath Radhakrishnan100% (8)

- Inscriptions 33rd Issue April2021Document47 pagesInscriptions 33rd Issue April2021Gopinath Radhakrishnan100% (4)

- Inscriptions 3Document24 pagesInscriptions 3Gopinath Radhakrishnan50% (2)

- Inscriptions 14Document45 pagesInscriptions 14Gopinath Radhakrishnan100% (1)

- Inscriptions 24th Issue JAN2019Document36 pagesInscriptions 24th Issue JAN2019Gopinath Radhakrishnan100% (3)

- Walmart PresentationDocument30 pagesWalmart PresentationPawan KumarNo ratings yet

- How To Manage Your Karmic AccountsDocument14 pagesHow To Manage Your Karmic AccountsBram100% (2)

- Changing Habits: Improve your Life by Changing your Habits. Stop Procrastinating, Create Healthy Behaviors, End Unhealthy Thinking and be More Successful: Invincible MindFrom EverandChanging Habits: Improve your Life by Changing your Habits. Stop Procrastinating, Create Healthy Behaviors, End Unhealthy Thinking and be More Successful: Invincible MindRating: 4 out of 5 stars4/5 (1)

- Master Your Habits: Strategies for Achieving Your Goals and Living Your Best LifeFrom EverandMaster Your Habits: Strategies for Achieving Your Goals and Living Your Best LifeNo ratings yet

- Inscriptions 35 October2021Document35 pagesInscriptions 35 October2021Gopinath Radhakrishnan100% (3)

- ResilientDocument12 pagesResilientmarina wezlyNo ratings yet

- Chap#3 Summary Applied EqDocument4 pagesChap#3 Summary Applied EqHina HussainNo ratings yet

- Bad Habits Makeover: Transform Your Life One Behavior at a TimeFrom EverandBad Habits Makeover: Transform Your Life One Behavior at a TimeNo ratings yet

- NeuroHabits: Master Your Life Through the Science of Habit ChangeFrom EverandNeuroHabits: Master Your Life Through the Science of Habit ChangeNo ratings yet

- Create and Modify HabitsDocument34 pagesCreate and Modify HabitsMykovosNo ratings yet

- James Tripp - Hypnosis Without TranceDocument12 pagesJames Tripp - Hypnosis Without TranceRon Herman89% (9)

- 8 Spiritual LawsDocument6 pages8 Spiritual LawsMark LangfordNo ratings yet

- Manifest With The Power of Thought and Attraction How To ManifestDocument8 pagesManifest With The Power of Thought and Attraction How To ManifestSteveNo ratings yet

- Habit Discussion GuideDocument13 pagesHabit Discussion GuidebarujseferNo ratings yet

- A Joosr Guide to... The Happiness Hypothesis by Jonathan Haidt: Finding Modern Truth in Ancient WisdomFrom EverandA Joosr Guide to... The Happiness Hypothesis by Jonathan Haidt: Finding Modern Truth in Ancient WisdomRating: 4.5 out of 5 stars4.5/5 (4)

- Atomic Habits Unleashed: Building Lasting Change, One Tiny Habit at a TimeFrom EverandAtomic Habits Unleashed: Building Lasting Change, One Tiny Habit at a TimeNo ratings yet

- 7 Powerful Secrets To Getting Stuff Done PDFDocument13 pages7 Powerful Secrets To Getting Stuff Done PDFAymane MourchidNo ratings yet

- Flow with the Go: Ways to Adapt to Unexpected Change, Everyday Situation and BeyondFrom EverandFlow with the Go: Ways to Adapt to Unexpected Change, Everyday Situation and BeyondNo ratings yet

- Metaphysics - The Heartbeat of The UniverseDocument7 pagesMetaphysics - The Heartbeat of The UniversehyanandNo ratings yet

- Article3 Video3Document8 pagesArticle3 Video3yulia boykooNo ratings yet

- Chitta ShuddhiDocument8 pagesChitta ShuddhiSwami Vedatitananda100% (8)

- CHANGE YOUR BRAIN: Unlock the Power of Neuroplasticity and Transform Your Mind for Optimal Living (2023 Guide for Beginners)From EverandCHANGE YOUR BRAIN: Unlock the Power of Neuroplasticity and Transform Your Mind for Optimal Living (2023 Guide for Beginners)No ratings yet

- Finally Happy: How to Easily Forge True and Enduring HappinessFrom EverandFinally Happy: How to Easily Forge True and Enduring HappinessNo ratings yet

- The Power of Routine: Elevate Your Life with Habits That StickFrom EverandThe Power of Routine: Elevate Your Life with Habits That StickNo ratings yet

- The Psychology of EmotionsDocument60 pagesThe Psychology of Emotionskunal arenNo ratings yet

- Psychological Issues 2 (An Integral Approach) - Abraham González Lara (2016)Document164 pagesPsychological Issues 2 (An Integral Approach) - Abraham González Lara (2016)abraham_akeraiosNo ratings yet

- STOP, TIP, Oppose, Sense, ImproveDocument9 pagesSTOP, TIP, Oppose, Sense, ImproveAndrew Davidson DwyerNo ratings yet

- Habits - Mark MansonDocument25 pagesHabits - Mark MansonKeerthivasanNo ratings yet

- Path To Weight LossDocument10 pagesPath To Weight LossLillith TRsNo ratings yet

- Habits - Mark MansonDocument25 pagesHabits - Mark MansonHarvest Walukow100% (1)

- The Power of Habit by Charles Duhigg: A Summary and AnalysisFrom EverandThe Power of Habit by Charles Duhigg: A Summary and AnalysisRating: 4 out of 5 stars4/5 (32)

- Habit Hacks : Simple & Effective Techniques for Positive ChangeFrom EverandHabit Hacks : Simple & Effective Techniques for Positive ChangeNo ratings yet

- Powerful Habits: Learn Good Habits to Live a Happy & Successful LifeFrom EverandPowerful Habits: Learn Good Habits to Live a Happy & Successful LifeNo ratings yet

- Homeroom Guidance Q4 - Module 15Document27 pagesHomeroom Guidance Q4 - Module 15Teacher Lii-Anne MagnoNo ratings yet

- Cue 1: Time: Bad Habits Are Replaced, Not EliminatedDocument6 pagesCue 1: Time: Bad Habits Are Replaced, Not Eliminatedbey luNo ratings yet

- Inscriptions 37 April 2022Document35 pagesInscriptions 37 April 2022Gopinath Radhakrishnan100% (9)

- Inscriptions 34 July2021Document51 pagesInscriptions 34 July2021Gopinath Radhakrishnan100% (1)

- Inscriptions 36 COVER PAGESDocument22 pagesInscriptions 36 COVER PAGESGopinath RadhakrishnanNo ratings yet

- Inscriptions 35 October2021Document35 pagesInscriptions 35 October2021Gopinath Radhakrishnan100% (3)

- Inscriptions 39 Oct2022Document38 pagesInscriptions 39 Oct2022Gopinath RadhakrishnanNo ratings yet

- Inscriptions 43 OCt2023Document37 pagesInscriptions 43 OCt2023Gopinath RadhakrishnanNo ratings yet

- Inscriptions 33rd Issue April2021Document47 pagesInscriptions 33rd Issue April2021Gopinath Radhakrishnan100% (4)

- Inscriptions 31 October 2020Document49 pagesInscriptions 31 October 2020Gopinath Radhakrishnan100% (8)

- Inscriptions 25Document41 pagesInscriptions 25Gopinath Radhakrishnan100% (12)

- Inscriptions 30 JULY2020Document41 pagesInscriptions 30 JULY2020Gopinath Radhakrishnan50% (4)

- Inscriptions 26 JULY 2019Document35 pagesInscriptions 26 JULY 2019Gopinath Radhakrishnan100% (8)

- Inscriptions 14Document45 pagesInscriptions 14Gopinath Radhakrishnan100% (1)

- Inscriptions 4Document27 pagesInscriptions 4Gopinath RadhakrishnanNo ratings yet

- Inscriptions 2Document22 pagesInscriptions 2Gopinath Radhakrishnan100% (1)

- Inscriptions 19 Oct2017Document24 pagesInscriptions 19 Oct2017Gopinath Radhakrishnan100% (7)

- Inscriptions 24th Issue JAN2019Document36 pagesInscriptions 24th Issue JAN2019Gopinath Radhakrishnan100% (3)

- Inscriptions 3Document24 pagesInscriptions 3Gopinath Radhakrishnan50% (2)

- Inscriptions Wall 1 Panel 1Document20 pagesInscriptions Wall 1 Panel 1Gopinath Radhakrishnan100% (3)

- Semester 6Document10 pagesSemester 6himalayabanNo ratings yet

- Chapter 8Document7 pagesChapter 8Yenelyn Apistar CambarijanNo ratings yet

- UST Case Study As of 1993: March 2016Document19 pagesUST Case Study As of 1993: March 2016KshitishNo ratings yet

- Income From Other SourcesDocument31 pagesIncome From Other SourcesNeeraj AgarwalNo ratings yet

- Takehome Quiz Ae 121Document3 pagesTakehome Quiz Ae 121Crissette RoslynNo ratings yet

- JAIIB-Accounts-Free Mock Test Jan 2022Document4 pagesJAIIB-Accounts-Free Mock Test Jan 2022kanarendranNo ratings yet

- Marketing Management 14th Edition Kotler Solutions ManualDocument38 pagesMarketing Management 14th Edition Kotler Solutions Manualdeliacerrutipro100% (12)

- Lectures On Financial Mathematics: Harald LangDocument85 pagesLectures On Financial Mathematics: Harald LangMiguel Angel BotinaNo ratings yet

- Pakistan Stock Exchange-1Document23 pagesPakistan Stock Exchange-1Umar Sajjad AwanNo ratings yet

- Appendix C: Time Value of MoneyDocument15 pagesAppendix C: Time Value of MoneyRabie HarounNo ratings yet

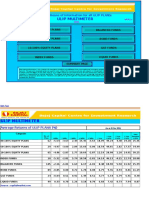

- Ulip MultimeterDocument17 pagesUlip MultimeterRaghu RaoNo ratings yet

- Common Factors Affecting Bond Returns PDFDocument2 pagesCommon Factors Affecting Bond Returns PDFRebecca50% (2)

- The Cost of Capital: Assets DebtDocument22 pagesThe Cost of Capital: Assets Debtaku kamuNo ratings yet

- Bond ValuationDocument42 pagesBond ValuationRahul KumarNo ratings yet

- Birth Certificate Bond To Treasury RedactedDocument1 pageBirth Certificate Bond To Treasury RedactedRicardo Vargas80% (5)

- Test Bank For Financial Accounting With International Financial Reporting Standards 4th Edition Jerry J Weygandt Paul D Kimmel Donald e KiesoDocument23 pagesTest Bank For Financial Accounting With International Financial Reporting Standards 4th Edition Jerry J Weygandt Paul D Kimmel Donald e Kiesoaudreycollinsnstjaxwkrd100% (42)

- Executive Summary: Industry SnapshotDocument105 pagesExecutive Summary: Industry SnapshotRajveer SinghNo ratings yet

- Howard Marks PresentationDocument11 pagesHoward Marks PresentationCanadianValueNo ratings yet

- Interest Rates An Introduction PDFDocument186 pagesInterest Rates An Introduction PDFHarshaNo ratings yet

- FICM ObsaaDocument105 pagesFICM Obsaasamuel kebede100% (1)

- Edmans 2015Document32 pagesEdmans 2015Maher KhasawnehNo ratings yet

- Relationship MarketingDocument241 pagesRelationship MarketingNishant Kumar100% (1)

- Requests For Admissions by CitiMortageDocument53 pagesRequests For Admissions by CitiMortageJylly JakesNo ratings yet

- All About BondsDocument103 pagesAll About BondsDrEwPabloNo ratings yet

- Risk Management With HDFC Securities by Ajay KhavaleDocument82 pagesRisk Management With HDFC Securities by Ajay Khavaleverma15No ratings yet

- Islamic-Finance-Book Volume 3 PDFDocument206 pagesIslamic-Finance-Book Volume 3 PDFnovi sekarNo ratings yet

- Governmental and Nonprofit Accounting 10Th Edition Smith Solutions Manual Full Chapter PDFDocument52 pagesGovernmental and Nonprofit Accounting 10Th Edition Smith Solutions Manual Full Chapter PDFJoanSmithrgqb100% (11)

- M12 Bade 9418 04 Ch10aDocument16 pagesM12 Bade 9418 04 Ch10aVanny Van Sneidjer100% (2)

- Denuncia de Leocenis García Contra Juan Guaidó y Nicolás MaduroDocument22 pagesDenuncia de Leocenis García Contra Juan Guaidó y Nicolás MaduroPresents 360No ratings yet