You might also like

- Credit Derivatives: Techniques to Manage Credit Risk for Financial ProfessionalsFrom EverandCredit Derivatives: Techniques to Manage Credit Risk for Financial ProfessionalsNo ratings yet

- 01 07 08 NYC JMC UpdateDocument10 pages01 07 08 NYC JMC Updateapi-27426110No ratings yet

- MML WhitepaperDocument5 pagesMML WhitepaperKors van der WerfNo ratings yet

- Collateralized Loan ObligationDocument3 pagesCollateralized Loan Obligationjosh321No ratings yet

- Preparing For The Unknown: Private DebtDocument24 pagesPreparing For The Unknown: Private Debtmichael zNo ratings yet

- Building A Strong Syndicated Credit FacilityDocument5 pagesBuilding A Strong Syndicated Credit Facilitymajed.taheri100% (1)

- Market Turmoil Draft 8-3-07Document21 pagesMarket Turmoil Draft 8-3-07ctb001No ratings yet

- Home Assignment - JUNK BOND Subject: Corporate FinanceDocument3 pagesHome Assignment - JUNK BOND Subject: Corporate FinanceAsad Mazhar100% (1)

- The Deal Private Credit's '24 Tech ResolutionsDocument7 pagesThe Deal Private Credit's '24 Tech Resolutionsshelby.wintersNo ratings yet

- M&A in Financial Sector May Provide Boost After Slow StartDocument7 pagesM&A in Financial Sector May Provide Boost After Slow StartAnjalika SinghNo ratings yet

- The Future of Hedge Fund Investing: A Regulatory and Structural Solution for a Fallen IndustryFrom EverandThe Future of Hedge Fund Investing: A Regulatory and Structural Solution for a Fallen IndustryNo ratings yet

- Big Freeze IIDocument5 pagesBig Freeze IIKalyan Teja NimushakaviNo ratings yet

- Goldman Sachs Investment Banking AnalysisDocument10 pagesGoldman Sachs Investment Banking Analysiskenn benNo ratings yet

- Risk Management Failures During The Financial Crisis: November 2011Document27 pagesRisk Management Failures During The Financial Crisis: November 2011Khushi ShahNo ratings yet

- Will The Bubble in Private Markets Hiss or Pop - Financial TimesDocument3 pagesWill The Bubble in Private Markets Hiss or Pop - Financial TimesAleksandar SpasojevicNo ratings yet

- Marathon S 2023 2024 Global Credit Whitepaper 1678838357Document23 pagesMarathon S 2023 2024 Global Credit Whitepaper 1678838357SwaggyVBros MNo ratings yet

- Money Market Instability: Interconnected CrisisDocument20 pagesMoney Market Instability: Interconnected Crisisctb001No ratings yet

- Private Markets in Volatile Times - Neuberger Berman (2023)Document5 pagesPrivate Markets in Volatile Times - Neuberger Berman (2023)sherNo ratings yet

- Private EquityDocument26 pagesPrivate Equitycvf100% (3)

- TM Assignemt - AbhishekDocument16 pagesTM Assignemt - AbhishekKhushboo LakarNo ratings yet

- Can Broker Consolidation Work in LondonDocument6 pagesCan Broker Consolidation Work in Londonfelix.stockerNo ratings yet

- Investment Banking 2005doc669Document29 pagesInvestment Banking 2005doc669tiwariparveshNo ratings yet

- Madoff Fraud Afects Hedge Funds IndustryDocument2 pagesMadoff Fraud Afects Hedge Funds Industryfreebanker777741No ratings yet

- Thesis Credit Default SwapsDocument7 pagesThesis Credit Default Swapsjessicaoatisneworleans100% (2)

- ProjectDocument7 pagesProjectmalik waseemNo ratings yet

- A Journey To The Alt-A ZoneDocument14 pagesA Journey To The Alt-A ZonejasnshihNo ratings yet

- FinTech Rising: Navigating the maze of US & EU regulationsFrom EverandFinTech Rising: Navigating the maze of US & EU regulationsRating: 5 out of 5 stars5/5 (1)

- Ultimate Guide To Debt & Leveraged Finance - Wall Street PrepDocument18 pagesUltimate Guide To Debt & Leveraged Finance - Wall Street PrepPearson SunigaNo ratings yet

- Global Capital Partners Fund LLC Is Expanding Investment Options With Impeccable Financial LoansDocument4 pagesGlobal Capital Partners Fund LLC Is Expanding Investment Options With Impeccable Financial LoansPR.comNo ratings yet

- Financial RisksDocument3 pagesFinancial RisksViz PrezNo ratings yet

- Managing Corporate Liquidity CrisisDocument8 pagesManaging Corporate Liquidity CrisisRusdi RuslyNo ratings yet

- Money MakersDocument7 pagesMoney MakerslacosteNo ratings yet

- Private Equity: Access for All: Investing in Private Equity through the Stock MarketsFrom EverandPrivate Equity: Access for All: Investing in Private Equity through the Stock MarketsNo ratings yet

- The Economics of Banking ExplainedDocument4 pagesThe Economics of Banking ExplainedRajesh AnnamalaiNo ratings yet

- Structured Products OverviewDocument7 pagesStructured Products OverviewAnkit GoelNo ratings yet

- NYU Press Chapter Examines AIG's Reckless CDS Bets and DownfallDocument23 pagesNYU Press Chapter Examines AIG's Reckless CDS Bets and DownfallRaymond Behnke [STUDENT]No ratings yet

- Marathon's 2023-2024 Credit Cycle White PaperDocument23 pagesMarathon's 2023-2024 Credit Cycle White PaperVincentNo ratings yet

- Hedge Funds in Trade FinanceDocument3 pagesHedge Funds in Trade FinancecoomccannNo ratings yet

- Spinning Around: The Craze For Private Assets Has Reached Fever Pitch. Can The Party Continue?Document14 pagesSpinning Around: The Craze For Private Assets Has Reached Fever Pitch. Can The Party Continue?Nguyễn Hương GiangNo ratings yet

- Q: - "Why Is British Banking in Crisis?" Provide Reasons and Suggest Possible Solutions?Document6 pagesQ: - "Why Is British Banking in Crisis?" Provide Reasons and Suggest Possible Solutions?scorpio786No ratings yet

- How To Save CashDocument3 pagesHow To Save CashSubramanian S (IN)No ratings yet

- The Alpha Masters: Unlocking the Genius of the World's Top Hedge FundsFrom EverandThe Alpha Masters: Unlocking the Genius of the World's Top Hedge FundsRating: 4 out of 5 stars4/5 (15)

- G11 - Short-term financing opportunities for small businessesDocument3 pagesG11 - Short-term financing opportunities for small businessesMULU TEMESGENNo ratings yet

- FT Citi To Slash Lending To Buyout Funds As New Capital Rules Bite Sept22Document10 pagesFT Citi To Slash Lending To Buyout Funds As New Capital Rules Bite Sept22tracy.jiang0908No ratings yet

- Rise of The CDSDocument20 pagesRise of The CDSza_gabyNo ratings yet

- Nuveen - A Good Time For Private DebtDocument3 pagesNuveen - A Good Time For Private Debtramachandra rao sambangiNo ratings yet

- Our Team Agenda Securitization CDS CDO LiquidityDocument81 pagesOur Team Agenda Securitization CDS CDO Liquidityshwetata986No ratings yet

- 2007 Subprime Mortgage Financial CrisisDocument12 pages2007 Subprime Mortgage Financial CrisisMuhammad Arief Billah100% (8)

- Performance of Private Credit Funds A First LookDocument37 pagesPerformance of Private Credit Funds A First LookIván WdiNo ratings yet

- Cma 051812Document16 pagesCma 051812Beer0% (1)

- February 2nd - February 15th, 2013: Rising Demand Propels Warehouse Market To Strong 2012 FinishDocument4 pagesFebruary 2nd - February 15th, 2013: Rising Demand Propels Warehouse Market To Strong 2012 FinishAnonymous Feglbx5No ratings yet

- Creditflux 1 June 2006 OCRDocument32 pagesCreditflux 1 June 2006 OCRfodriscollNo ratings yet

- Disbursement (CASH) VoucherDocument18 pagesDisbursement (CASH) VoucherReymart BorresNo ratings yet

- Account Transfer Form (ACAT)Document6 pagesAccount Transfer Form (ACAT)MichelleNo ratings yet

- RON Transfer ConfirmationDocument1 pageRON Transfer ConfirmationIordan FlorinNo ratings yet

- Salary Statement (Sbi) 10-08-2023Document7 pagesSalary Statement (Sbi) 10-08-2023finetech softwareNo ratings yet

- Oct PayslipDocument3 pagesOct PayslipRajanala Vignesh NaiduNo ratings yet

- Sample Diminishing BalnceDocument1 pageSample Diminishing BalnceAbie OniaNo ratings yet

- How To File A 1096 and 1099 and 1099oid To Pay Utility BillsDocument10 pagesHow To File A 1096 and 1099 and 1099oid To Pay Utility BillsTitle IV-D Man with a plan99% (86)

- Libra To Vashu TradingDocument1 pageLibra To Vashu TradingLL Lawwise Consultech India Pvt LtdNo ratings yet

- On January 2Document2 pagesOn January 2Chris Tian FlorendoNo ratings yet

- Tentative Agreement Overview 2021.12.01Document7 pagesTentative Agreement Overview 2021.12.01WWMTNo ratings yet

- Bank Statement PDFDocument188 pagesBank Statement PDFragaveyndhar maniNo ratings yet

- Differences Between Commercial and Central BankDocument12 pagesDifferences Between Commercial and Central BankTrifan_DumitruNo ratings yet

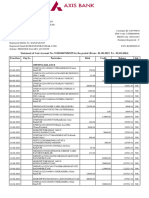

- Statement of Axis Account No:911010047456925 For The Period (From: 01-08-2023 To: 02-02-2024)Document12 pagesStatement of Axis Account No:911010047456925 For The Period (From: 01-08-2023 To: 02-02-2024)shekhar17042012No ratings yet

- Topic 3: Bankruptcy 1) Second or Subsequent BankruptcyDocument6 pagesTopic 3: Bankruptcy 1) Second or Subsequent BankruptcySyahirah ArifNo ratings yet

- Rebate: Due DateDocument2 pagesRebate: Due Datebhuban020383No ratings yet

- SimpleandCompoundInterest 2ndsessionDocument58 pagesSimpleandCompoundInterest 2ndsessionprachiNo ratings yet

- Loan CalculatorDocument7 pagesLoan Calculatordattatray bhanuseNo ratings yet

- Basic Finance Final Q2Document13 pagesBasic Finance Final Q2Michelle EsperalNo ratings yet

- Myvi SST July22Document1 pageMyvi SST July22suhayl azlanNo ratings yet

- A Study On Financial Literacy of Malaysian Degree Students PDFDocument9 pagesA Study On Financial Literacy of Malaysian Degree Students PDFbilalrafiqgaganNo ratings yet

- Detailstatement - 19 7 2023@15 21 27Document2 pagesDetailstatement - 19 7 2023@15 21 27aarti RwtNo ratings yet

- Finance in IndiaDocument6 pagesFinance in IndiamanojNo ratings yet

- 4 Partnership LiquidationDocument6 pages4 Partnership LiquidationArmhel FangonNo ratings yet

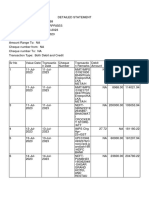

- Detailed StatementDocument2 pagesDetailed StatementtestNo ratings yet

- Pension Book NEW 2Document14 pagesPension Book NEW 2Principal ghss no 1No ratings yet

- SMJK Shan Tao (29th April 23) PDFDocument4 pagesSMJK Shan Tao (29th April 23) PDFBao YiNo ratings yet

- Credit AppDocument1 pageCredit Appautoheim59No ratings yet

- 2020 IvyZelman Fairway PresentationDocument41 pages2020 IvyZelman Fairway PresentationpharssNo ratings yet

- InventarioProcesosActivos 18-12-2020Document691 pagesInventarioProcesosActivos 18-12-2020Luz Angela Barrero ChavesNo ratings yet

- View bank statement online for Mr Juan RamosDocument2 pagesView bank statement online for Mr Juan RamosLong Home ProductsNo ratings yet