You might also like

- Learning Activity 3 - Inc TaxDocument3 pagesLearning Activity 3 - Inc TaxErica FlorentinoNo ratings yet

- Tax On Individuals Quiz - ProblemsDocument3 pagesTax On Individuals Quiz - ProblemsJP Mirafuentes100% (1)

- Rodel's 2020 Income Tax Computation with Itemized DeductionsTITLE Mulry's 2020 Taxable Income and Tax Payable TITLE Sharon's Various 2020 Tax Computations as Resident, Non-Resident ETB and NETBDocument5 pagesRodel's 2020 Income Tax Computation with Itemized DeductionsTITLE Mulry's 2020 Taxable Income and Tax Payable TITLE Sharon's Various 2020 Tax Computations as Resident, Non-Resident ETB and NETByezaquera100% (1)

- Tax Quiz SolutionsDocument3 pagesTax Quiz SolutionsLora Mae JuanitoNo ratings yet

- Income TaxationDocument5 pagesIncome Taxationangellachavezlabalan.cpalawyerNo ratings yet

- Illustration 5Document2 pagesIllustration 5Bea Nicole BaltazarNo ratings yet

- Solution: A. Gross Business Income, PhilippinesDocument9 pagesSolution: A. Gross Business Income, Philippineslena cpa78% (9)

- Take Home Seatwork 11.25.2023Document2 pagesTake Home Seatwork 11.25.2023rhenzadrian.11No ratings yet

- Tax Calculation for CJR's 2018 IncomeDocument1 pageTax Calculation for CJR's 2018 IncomeEdnel LoterteNo ratings yet

- He Is Not Subject To Basic Income Tax. However, His 13th Month Pay Exceeds 90,000. ThereforeDocument15 pagesHe Is Not Subject To Basic Income Tax. However, His 13th Month Pay Exceeds 90,000. ThereforeEarl Daniel RemorozaNo ratings yet

- Tax Final TaxDocument19 pagesTax Final TaxSittie Aisah AmpatuaNo ratings yet

- 8.2 Assignment - Regular Income Tax For Individuals (For Discussion)Document8 pages8.2 Assignment - Regular Income Tax For Individuals (For Discussion)Roselyn LumbaoNo ratings yet

- TAX Final-PreboardDocument14 pagesTAX Final-PreboardMarjorie BernasNo ratings yet

- Individual Taxation Problem SolvingDocument7 pagesIndividual Taxation Problem SolvingSecret-uploader50% (2)

- Regular vs Final Tax Guide for Individual Filipino TaxpayersDocument8 pagesRegular vs Final Tax Guide for Individual Filipino TaxpayersElla Marie Lopez0% (1)

- Answers, Solutions and Clarifications FileDocument3 pagesAnswers, Solutions and Clarifications FileAnnie LindNo ratings yet

- ANSWERS Post Test Regular Income Taxation For PartnershipsDocument8 pagesANSWERS Post Test Regular Income Taxation For Partnershipslena cpa100% (1)

- INCOME TAXATION Drills With AnswersDocument5 pagesINCOME TAXATION Drills With AnswersViky Rose EballeNo ratings yet

- Taxation Quiz - Passive Income, Residency, and MoreDocument7 pagesTaxation Quiz - Passive Income, Residency, and MoreIsaiah John Domenic M. CantaneroNo ratings yet

- Taxation 109Document2 pagesTaxation 109Bisag AsaNo ratings yet

- Seatwork 1 - Final Tax and Compensation Income 2.0Document2 pagesSeatwork 1 - Final Tax and Compensation Income 2.0Magical LunaNo ratings yet

- Problem 1Document3 pagesProblem 1Shiene MedrianoNo ratings yet

- Income Tax Quiz AnswerDocument4 pagesIncome Tax Quiz AnswerMarco Alejandro Ibay100% (1)

- Cases On Taxation For Individualss AnswersDocument11 pagesCases On Taxation For Individualss AnswersMitchie Faustino100% (2)

- Quiz 3 - CabigonDocument4 pagesQuiz 3 - CabigonRie CabigonNo ratings yet

- Tax Pre TestDocument4 pagesTax Pre TestSebastian GarciaNo ratings yet

- Solutions For Problem 1Document4 pagesSolutions For Problem 1spongebob SquarepantsNo ratings yet

- Income in Foreign Country: Two WaysDocument3 pagesIncome in Foreign Country: Two WaysPaul Anthony AspuriaNo ratings yet

- Basic Principles of TaxationDocument18 pagesBasic Principles of TaxationAlexandra Nicole IsaacNo ratings yet

- Ea - TaxDocument8 pagesEa - TaxKc SevillaNo ratings yet

- Post Test Regular Income Taxation For PartnershipsDocument6 pagesPost Test Regular Income Taxation For Partnershipslena cpaNo ratings yet

- ASSIGNMENT NO. 3 Chapter 7 Regular Income TaxationDocument4 pagesASSIGNMENT NO. 3 Chapter 7 Regular Income TaxationElaiza Jayne PongaseNo ratings yet

- Che Che H. Datingaling OMGT-2102: Answer: Taxable Income Is P700,000Document4 pagesChe Che H. Datingaling OMGT-2102: Answer: Taxable Income Is P700,000cheche datingalingNo ratings yet

- Ama Aia - Tax01-Final Exam-Casilla 2nd Sem Ay 2021-2022Document9 pagesAma Aia - Tax01-Final Exam-Casilla 2nd Sem Ay 2021-2022Meg CruzNo ratings yet

- Quiz 1 - StrataxDocument3 pagesQuiz 1 - Strataxspongebob SquarepantsNo ratings yet

- Assignment 1 Taxes On IndividualsDocument7 pagesAssignment 1 Taxes On IndividualsMarynissa CatibogNo ratings yet

- 8.2 Assignment - Regular Income Tax For IndividualsDocument8 pages8.2 Assignment - Regular Income Tax For Individualssam imperialNo ratings yet

- 8.6 Assignment - Regular Income Tax On CorporationsDocument3 pages8.6 Assignment - Regular Income Tax On CorporationsRoselyn LumbaoNo ratings yet

- 09tp TaxationDocument3 pages09tp TaxationKatelyn Mae SungcangNo ratings yet

- SW05Document7 pagesSW05Nadi HoodNo ratings yet

- Taaaaax PDFDocument40 pagesTaaaaax PDFAnne Marieline BuenaventuraNo ratings yet

- FUNDALES BTAX MidtermsDocument4 pagesFUNDALES BTAX MidtermsE. RobertNo ratings yet

- Final and Capital Gains TaxDocument7 pagesFinal and Capital Gains TaxElla Marie LopezNo ratings yet

- 21 Comprehensive Tax Cases: Multiple Choice: Choose The Best Possible AnswerDocument21 pages21 Comprehensive Tax Cases: Multiple Choice: Choose The Best Possible AnswerMessi Andal0% (1)

- Exercises in Corporation SolutionsDocument6 pagesExercises in Corporation Solutionsdiane camansagNo ratings yet

- Prv-Tax 1Document4 pagesPrv-Tax 1Kathylene GomezNo ratings yet

- TAX 1201 Answers Deductions From Gross IncomeDocument6 pagesTAX 1201 Answers Deductions From Gross IncomeCarlo Agravante100% (1)

- Individual Illustration and Activity No. 2Document22 pagesIndividual Illustration and Activity No. 2Angela CanayaNo ratings yet

- Individual Illustration and Activity No. 2Document19 pagesIndividual Illustration and Activity No. 2김유나100% (1)

- TAX.03 Exercises On Corporate Income TaxationDocument7 pagesTAX.03 Exercises On Corporate Income Taxationleon gumbocNo ratings yet

- Prefinal Exam Phil TaxDocument4 pagesPrefinal Exam Phil TaxDarren GreNo ratings yet

- Taxation Material 3Document11 pagesTaxation Material 3Shaira BugayongNo ratings yet

- Preparation of Income Tax Return IndividualDocument2 pagesPreparation of Income Tax Return IndividualFRAULIEN GLINKA FANUGAONo ratings yet

- P6 3Document5 pagesP6 3Neil RyanNo ratings yet

- Non-Resident Foreign CorporationDocument4 pagesNon-Resident Foreign CorporationRosemarie CruzNo ratings yet

- The Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeFrom EverandThe Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Wealth Management Planning: The UK Tax PrinciplesFrom EverandWealth Management Planning: The UK Tax PrinciplesRating: 4.5 out of 5 stars4.5/5 (2)

- J.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineNo ratings yet

- NikolsddDocument1 pageNikolsddMaissyNo ratings yet

- Ijbel24.isu 6 929Document6 pagesIjbel24.isu 6 929MaissyNo ratings yet

- 306 "Truth in Lending Act" Disclosure Requirement: - PersonDocument3 pages306 "Truth in Lending Act" Disclosure Requirement: - PersonJennifer MoscareNo ratings yet

- ACCO 30033 ExercisesDocument16 pagesACCO 30033 ExercisesGenevieve Arpon100% (1)

- Project Global Fast FoodsDocument5 pagesProject Global Fast FoodsandreeaNo ratings yet

- Career Opportunities in EventsDocument5 pagesCareer Opportunities in EventsTruc TThanhNo ratings yet

- Kadvani Forge Limitennnd3Document133 pagesKadvani Forge Limitennnd3Kristen RollinsNo ratings yet

- Consumer News Namibia Feb 2013Document28 pagesConsumer News Namibia Feb 2013Milton LouwNo ratings yet

- Life Board Game Rules - The Game of LifeDocument6 pagesLife Board Game Rules - The Game of LifeNinzin ConreyNo ratings yet

- Managerial Accounting 16th Ed Textbook Solutions Manual Chapter 01Document92 pagesManagerial Accounting 16th Ed Textbook Solutions Manual Chapter 01Tiến AnhNo ratings yet

- New Microsoft Word DocumentDocument28 pagesNew Microsoft Word DocumentHori LalNo ratings yet

- Winter Training Project ReportDocument42 pagesWinter Training Project ReportTamanna Rana100% (1)

- Lecture 18Document32 pagesLecture 18Mohammad Tariqul IslamNo ratings yet

- Labor Law Digest 3Document15 pagesLabor Law Digest 3LouFloresNo ratings yet

- F6 (VNM) - FXVN Ltd Foreign Exchange Gains and LossesDocument12 pagesF6 (VNM) - FXVN Ltd Foreign Exchange Gains and LossesHuyền NguyễnNo ratings yet

- Grade Matrix ProjectDocument10 pagesGrade Matrix ProjectRajesh InsbNo ratings yet

- Case Assignment 1 - Invent A Fraud Khadine PriceDocument8 pagesCase Assignment 1 - Invent A Fraud Khadine Pricekhadine PriceNo ratings yet

- Letter To Mayor de BlasioDocument5 pagesLetter To Mayor de BlasioNew York Daily NewsNo ratings yet

- Compensation Management SystemDocument12 pagesCompensation Management Systemswarnaprava.ss1999No ratings yet

- Avc-Ii-B (HRM) Week-1 Functions of Human Resource ManagementDocument12 pagesAvc-Ii-B (HRM) Week-1 Functions of Human Resource ManagementcecilNo ratings yet

- Cad - AutocadDocument15 pagesCad - AutocadJohn DareNo ratings yet

- Document 13Document3 pagesDocument 13Naman AgrawalNo ratings yet

- R&E Transport, Inc. v. LatagDocument2 pagesR&E Transport, Inc. v. LatagrubdrNo ratings yet

- YdryDocument2 pagesYdryVinodhkumar Shanmugam100% (1)

- Volume 1 Conditions of ServiceDocument129 pagesVolume 1 Conditions of ServiceDefimediagroup LdmgNo ratings yet

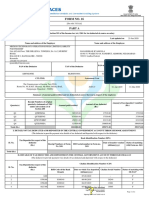

- Form No. 16: Part ADocument10 pagesForm No. 16: Part ARAJASHEKAR KYAROLLANo ratings yet

- Grant in Aid CodeDocument29 pagesGrant in Aid CodeAbdullah Basha OnjeeNo ratings yet

- Private Law in CompaniesDocument5 pagesPrivate Law in CompaniesLara CampinhoNo ratings yet

- The Project Work Has Been Undertaken With A View To Study The Quality ofDocument5 pagesThe Project Work Has Been Undertaken With A View To Study The Quality ofDelsy KrishnanNo ratings yet

- Oam MidtermDocument50 pagesOam MidtermSantos Kim0% (1)

- Queries Related To ITR FilingDocument3 pagesQueries Related To ITR FilingRajesh KashyapNo ratings yet

- Practical Exercises SpredsheetsDocument23 pagesPractical Exercises SpredsheetsDaVid Silence Kawlni89% (9)

- Data TypesDocument2 pagesData Typeskvigneshk2001No ratings yet

- ACI Employee Benefits Package AnalysisDocument35 pagesACI Employee Benefits Package AnalysisMonzurul Kadir ShakeelNo ratings yet